Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom A general partnership (definition) is a straightforward business structure where two or more individuals agree to be co-owners of a for-profit business. Often the default entity for businesses with multiple owners, it stands out for its simplicity and minimal setup requirements. For those looking to register a company in Vietnam, a general partnership offers a practical and flexible option. In this comprehensive guide, we will break down everything you need to know about its formation, the critical role of a partnership agreement, its tax implications, and the significant liability risks involved.

What is a general partnership?

A general partnership is a business structure where two or more individuals jointly own and operate a business. In Vietnam, a general partnership is a specific legal entity registered under the Enterprise Law (Article 177, Law on Enterprises 2020). Unlike a default status, it requires formal registration. It is a legal entity separate from its partners, but the general partners have unlimited and joint liability for the partnership’s obligations with all their assets. General partners share profits, responsibilities, and liabilities. They must be individuals (not corporations) and are actively involved in the day-to-day management of the enterprise.

Key characteristics of a general partnership

Several fundamental traits define a general partnership, setting it apart from other business structures like the sole proprietorship. Understanding these is crucial for anyone considering this form of business.

- Shared management: In a general partnership, all partners typically have equal rights to participate in the management and control of the business. Major decisions usually require a consensus among the partners. Unless specified otherwise in a partnership agreement, each partner has the authority to act on behalf of the business and make decisions that bind the entire partnership.

- Pass-through taxation: General partnerships benefit from what is known as flow-through entities taxation. The business itself does not pay income tax. Instead, profits and losses are "passed through" to the individual partners, who then report this information on their personal tax returns. This avoids the issue of double taxation that can occur with corporations, where the company's profits are taxed at the corporate level and again when distributed to shareholders as dividends.

The partnership agreement

A comprehensive partnership agreement is essential to prevent future disputes over finances and management. This legally binding document acts as a roadmap for the business, clearly outlining the expectations and responsibilities of each partner. Drafting a thorough agreement is a foundational step for success and conflict prevention.

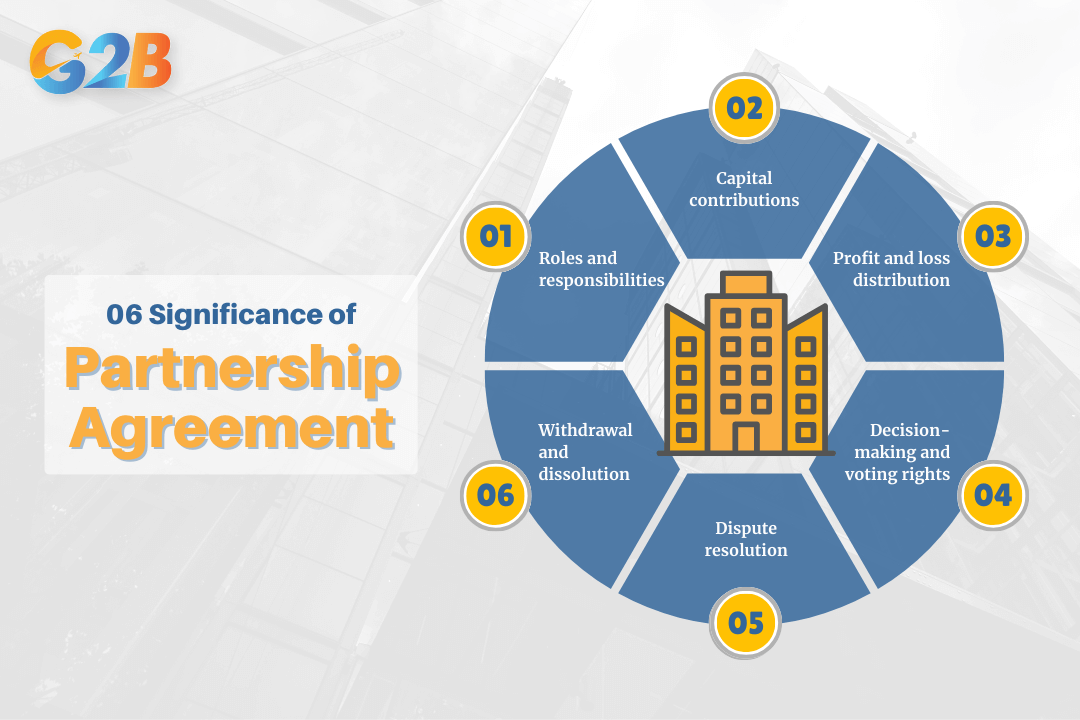

6 Critical components that every partnership agreement should include

Here are the critical components that every partnership agreement should include:

- Roles and responsibilities: The agreement should clearly define the specific duties and authority of each partner. This helps prevent overlap and ensures that all essential business activities, such as accounting, marketing, and operations, are covered.

- Capital contributions: This section details what each partner contributes to the business at the outset. The agreement should list each partner's initial contributions, such as cash, property, or specialized services, and establish their respective ownership percentages. This forms the initial capital structure of the partnership.

- Profit and loss distribution: The agreement must specify how profits and losses will be allocated among the partners. While profits are often split equally, partners can agree to a different distribution based on their contributions or other factors.

- Decision-making and voting rights: To avoid deadlocks, the agreement should outline the process for making key business decisions. It should clarify whether decisions require a unanimous vote or a simple majority and how voting power is allocated among partners.

- Dispute resolution: It's wise to plan for disagreements before they arise. The agreement should include a clause detailing the procedures for resolving disputes, which might involve mediation, arbitration, or another agreed-upon method.

- Withdrawal and dissolution: The agreement should define the process for a partner leaving the business, whether voluntarily, due to death, or other circumstances. This 'exit strategy' is critical for a smooth transition and avoids potential legal disputes down the line.

Liability in a general partnership

This is the most critical aspect to understand before forming a general partnership. The structure offers no liability protection, which carries significant personal financial risk for the partners. This is a key difference when comparing sole proprietorship vs partnership.

- Unlimited personal liability: In a general partnership, while the business is a separate legal entity, the general partners have unlimited personal liability for the business's debts and obligations. This means that if the business cannot pay its debts, creditors can go after the partners' personal assets, such as their homes, cars, and bank accounts.

- Joint and several liability: General partnerships are subject to joint and several liability. This means that each partner is not only responsible for their own actions but also for the actions of their partners when acting on behalf of the business. A creditor can choose to sue all partners together or any individual partner for the full amount of a business debt. For instance, if one partner signs a contract that the business cannot fulfill, a creditor could pursue any of the other partners to recover the entire debt.

Advantages and disadvantages of a general partnership

Choosing a business structure requires a balanced view of its pros and cons. A general partnership offers simplicity but at the cost of personal protection. This trade-off is often debated when considering sole proprietorship vs general partnership.

A general partnership offers many pros and cons

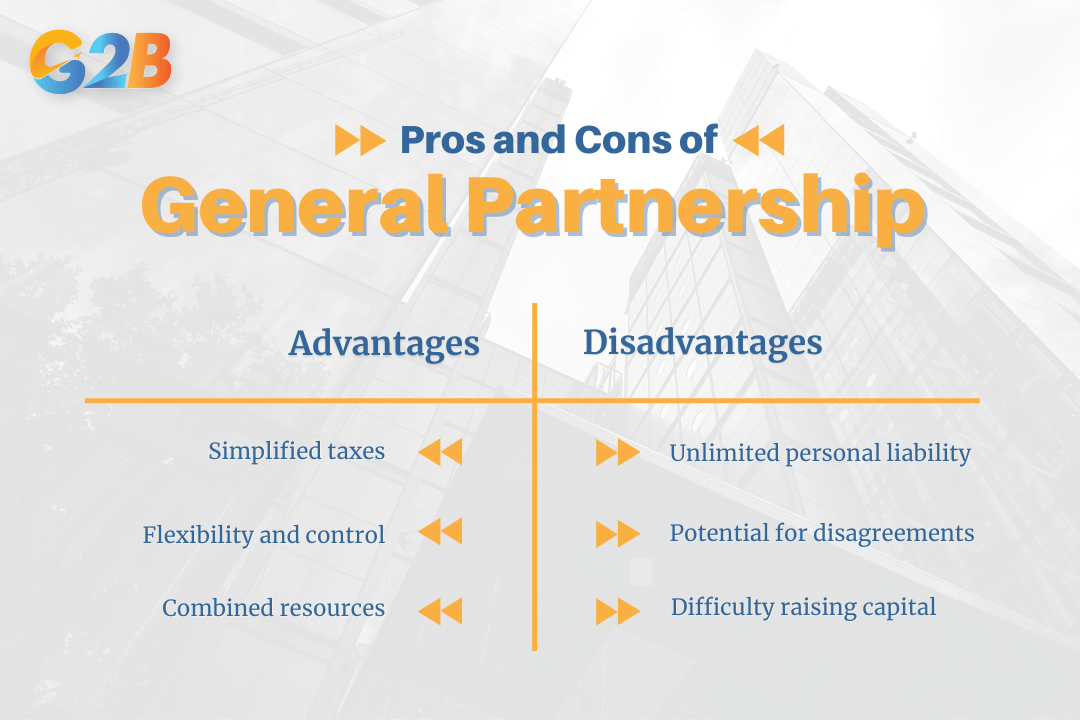

Advantages:

- Simplified taxes: The pass-through tax structure is a major benefit, as it avoids double taxation and simplifies the tax filing process. Profits and losses are reported on personal tax returns.

- Flexibility and control: Partners have a high degree of flexibility in managing the business without the rigid formalities and regulations that govern corporations.

- Combined resources: With multiple owners, the business can benefit from a larger pool of capital, skills, and expertise than a sole proprietorship.

Disadvantages:

- Unlimited personal liability: The most significant drawback is unlimited personal liability, as your personal assets are not protected from business debts. Due to this risk, partners should strongly consider implementing asset protection strategies.

- Joint liability for partners' actions: Each partner is legally responsible for the business-related actions of all other partners, which requires a high level of trust.

- Potential for disagreements: Without a detailed partnership agreement, disagreements over management, finances, and business direction can easily arise and escalate.

- Difficulty raising capital: General partnerships can find it challenging to attract outside investors, who may be hesitant due to the unlimited liability and lack of a formal ownership structure.

How to form a general partnership

In Vietnam, forming a general partnership (a partnership company) requires formal registration and approval by the business registration office.

- Choose a business name: Choose an official company name following Vietnamese regulations, which must include the company type “Cong ty Hop Danh” followed by the unique name.

- Draft a comprehensive partnership agreement: Draft a comprehensive partnership agreement, known as the company's Charter, which is mandatory to submit for official registration.

- Obtain business licenses and permits: Depending on your industry and location, your partnership will need to secure the necessary federal, state, and local licenses and permits to operate legally.

- Get an EIN or TIN: If you plan to hire employees or open a business bank account, you must obtain an EIN from the IRS (or a TIN in Vietnam). This number serves as your business's federal tax ID.

Taxation of a general partnership

Understanding the tax obligations of a general partnership is vital for maintaining compliance and managing finances effectively. Unlike pass-through entities in the U.S., a general partnership in Vietnam is subject to corporate income tax at a rate of 20% (CIT) under the Law on Corporate Income Tax 2025 (Law No. 67/2025/QH15). The partnership itself pays corporate income tax before distributing profits to partners, who then pay personal income tax on their shares.

Dissolving a general partnership

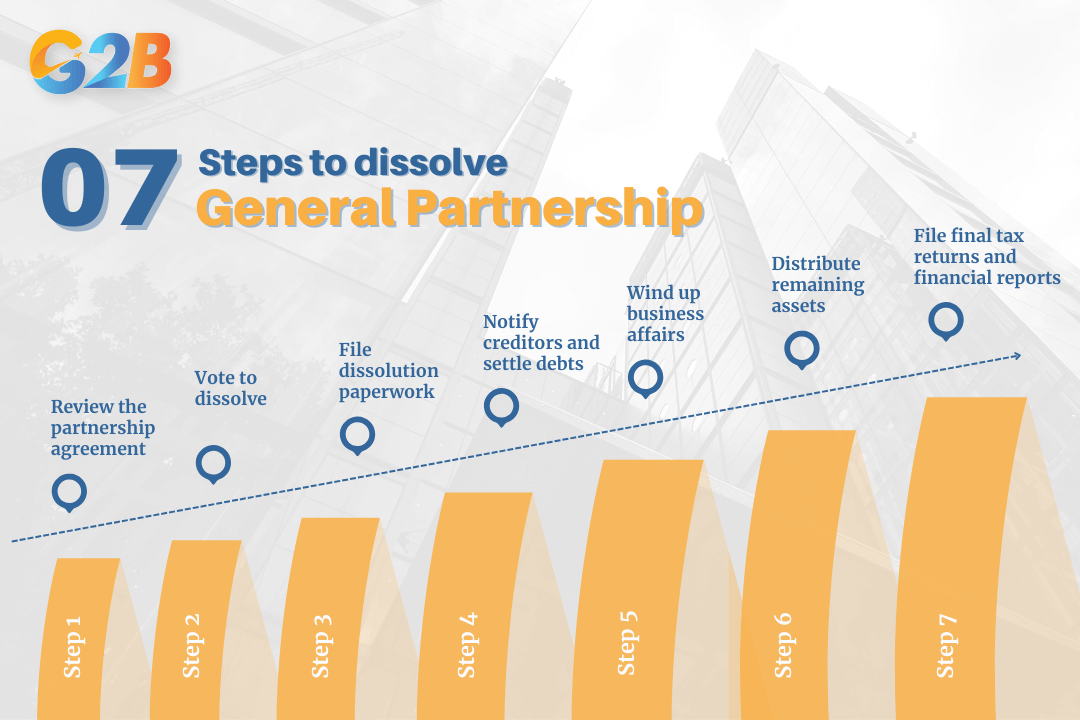

The process of ending a general partnership, known as dissolution and "winding up," requires careful attention to legal and financial details to avoid future liabilities.

- Review the partnership agreement: The first step is to consult the partnership agreement, which should outline the procedures for dissolution agreed upon by the partners.

- Vote to dissolve: If the agreement requires it, the partners must formally vote to dissolve the partnership. If there is no agreement, state laws will govern the process.

- File dissolution paperwork: In Vietnam, the company must file a dissolution registration dossier with the Business Registration Office within 07 days after the dissolution decision, including notifying the tax authorities and publishing the decision on the National Business Registration Portal.

- Notify creditors and settle debts: It is crucial to notify all creditors, suppliers, and customers that the partnership is ending. All business debts must be paid off using partnership assets.

- Wind up business affairs: This includes closing business bank accounts, canceling licenses and permits, and finalizing any outstanding contracts.

- Distribute remaining assets: After all debts are settled, any remaining assets are distributed among the partners according to the terms of the partnership agreement.

- File final tax returns and financial reports as required by Vietnamese law before completing the dissolution process.

How to dissolve a general partnership

General partnership vs. other business structures

Choosing the right business entity depends on your specific needs regarding liability, management, and taxation. Here’s how a general partnership compares to other common structures.

- General partnership vs. Limited partnership (LP): The main difference lies in liability and management. A general partnership in Vietnam consists of general partners who have unlimited liability and, optionally, capital contributing partners with limited liability. The key distinction from a limited partnership is that general partners manage the business and assume unlimited liability, while capital contributing partners have liability limited to their capital contribution and do not manage the company.

- General partnership vs. Limited liability partnership (LLP): An LLP provides liability protection for all partners, shielding them from the debts of the business and the malpractice of other partners. This structure is common among professionals like lawyers and accountants. In a general partnership, no such liability protection exists. This distinction is often highlighted in LLC vs LLP comparisons. However, Vietnam does not formally provide for Limited Liability Partnerships (LLPs) as in some other countries.

- General partnership vs. LLC: A Limited Liability Company (LLC) offers its owners (called members) personal liability protection, similar to a corporation, while still providing the pass-through taxation benefits of a partnership. An LLC in Vietnam provides personal liability protection for its members, who are responsible only up to the amount of their capital contribution, unlike a general partnership, where general partners have unlimited liability. This is a primary reason why many entrepreneurs weigh LLC vs Partnership carefully before incorporating.

Choosing a business structure in Vietnam

Choosing between a general partnership, a Limited Liability Company (LLC), or a joint stock company is a crucial decision in the business registration process in Vietnam. According to Vietnam's Law on Enterprises, each of these structures offers distinct advantages and disadvantages that directly impact liability, capital mobilization, and management.

A partnership is often selected for its straightforward structure. However, similar to its international counterparts, it involves unlimited liability for general partners, meaning they are responsible for the company's obligations with all of their personal assets. In contrast, a limited liability company stands out as the most popular choice for small to medium-sized enterprises and foreign investors. This preference is largely because it limits the owners' liability to the amount of their capital contribution to the business.

A general partnership offers an easy and flexible way for two or more people to go into business together. Its simplicity and pass-through taxation make it an attractive option for new ventures. However, this ease comes with the profound risk of unlimited personal liability, which exposes partners' personal assets to business debts. The single most important takeaway is the absolute necessity of a comprehensive, well-drafted partnership agreement.