Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Limited Liability Companies (LLCs) are known for their blend of personal asset protection and flexible taxation, while Partnerships emphasize a more straightforward approach to shared ownership and profit distribution. This analysis explores how each type - LLC and Partnership - fundamentally differs in business structure, liability protection, taxation, and management practices, offering a detailed comparison of their distinctive features.

Understanding LLCs and Partnerships

Limited Liability Companies (LLCs) and Partnerships are two popular business structures, each offering distinct advantages and challenges. Let’s dive deeper into their key differences in this part below.

What is a Limited Liability Company (LLC)?

A Limited Liability Company (LLC) is a hybrid business entity that combines the liability protection of a corporation with the tax efficiencies and operational flexibility of a partnership. LLCs are established through state registration and must comply with specific regulatory requirements.

Key characteristics of an LLC:

- Liability protection: Members (owners) are not personally liable for the company’s debts or legal obligations.

- Tax treatment: Generally, LLCs benefit from pass-through taxation, meaning profits and losses flow through to members' personal tax returns, avoiding double taxation.

- Management flexibility: An LLC can be member-managed (owners handle operations) or manager-managed (owners appoint managers to run the business).

- Formation requirements: LLCs must file Articles of Organization with the state and often require an Operating Agreement outlining ownership and management structures.

- Compliance obligations: Annual filings, reports, and fees vary by state.

What is a Partnership?

A Partnership is a business arrangement where two or more individuals share ownership. There are multiple types of partnerships, each with different levels of liability and management control:

Types of partnerships:

- General Partnership (GP):

- Each partner shares equal responsibility for business operations.

- Partners have unlimited personal liability for business debts.

- Formation is informal and often does not require state registration.

- Limited Partnership (LP):

- Comprises general partners (who manage the business and assume liability) and limited partners (who invest but have no management role and limited liability).

- Requires a formal agreement and state registration.

- Limited Liability Partnership (LLP):

- Provides liability protection for all partners against business debts and malpractice claims.

- Often used by professional services firms (law firms, accounting firms, etc.).

- Requires state registration and compliance with additional regulations.

Key legal and structural differences between LLCs and Partnerships

| Factor | LLC | General Partnership | Limited Partnership (LP) | Limited Liability Partnership (LLP) |

|---|---|---|---|---|

| Liability protection | Members are protected from personal liability | Partners have unlimited liability | General partners have unlimited liability; limited partners are protected | Partners have limited liability |

| Taxation | Pass-through taxation (unless elected as a corporation) | Pass-through taxation | Pass-through taxation | Pass-through taxation |

| Management | Flexible: member-managed or manager-managed | Partners equally manage | General partners manage; limited partners do not participate | Partners share management responsibilities |

| Formation requirements | Requires state registration | No formal registration needed | Requires formal agreement and state registration | Requires state registration and compliance obligations |

| Ownership transferability | More complex but possible | Difficult unless all partners agree | Limited partners can transfer ownership; general partners cannot | Ownership transfer depends on partnership agreement |

Liability protection: Which offers better protection?

Liability exposure directly affects business owners’ financial security, making it one of the most crucial factors in selecting a business structure. This section provides an in-depth analysis of personal liability risks in different business entities.

Personal liability in an LLC

A Limited Liability Company (LLC) offers one of the strongest liability shields among small business structures. Owners, referred to as members, are not personally liable for business debts and lawsuits under most circumstances. This means:

- Creditors cannot pursue members' personal assets (homes, cars, savings) to settle business debts.

- Liability is limited to the amount of capital a member has invested in the LLC.

- If the LLC is sued, the lawsuit generally targets only business assets, not the personal wealth of the owners.

However, piercing the corporate veil is a key legal doctrine that can override an LLC’s liability shield. Courts may hold members personally responsible if:

- The LLC is not properly maintained (e.g., no separate bank account, mixing personal and business finances).

- Members commit fraud or illegal acts.

- The LLC does not follow state-mandated compliance requirements.

Personal liability in a General Partnership

A General Partnership (GP) exposes partners to unlimited personal liability. This means:

- Each partner is personally responsible for all business debts.

- If one partner takes on debt or signs a contract, all partners share the legal responsibility.

- Personal assets (homes, investments, bank accounts) can be used to satisfy business obligations.

- If one partner is sued, the plaintiff can pursue any or all partners for the full debt amount.

This structure works well for low-risk businesses but poses a significant financial risk for partnerships operating in industries with potential lawsuits, such as professional services or product-based businesses.

How LLPs & LPs provide partial protection

Some partnerships offer limited liability through variations such as Limited Partnerships (LPs) and Limited Liability Partnerships (LLPs):

- Limited Partnerships (LPs):

- Have both general partners (GPs) and limited partners (LPs).

- General partners retain full liability, while limited partners’ liability is capped at their investment.

- Limited partners must avoid active management to maintain liability protection.

- Limited Liability Partnerships (LLPs):

- Protect partners from personal liability for business debts.

- Shield partners from negligence claims made against their co-partners.

- Typically favored by professional firms (law firms, accounting firms, medical practices).

While LLPs provide better protection than general partnerships, liability coverage varies by state, and some jurisdictions restrict their formation to specific professions.

Legal implications of business debts

Different business structures dictate how creditors recover debts and the extent of an owner’s liability:

| Business structure | Personal liability for business debts | Protection level |

|---|---|---|

| LLC | No, unless personal guarantee or fraud | High |

| General Partnership (GP) | Yes, partners are fully liable | None |

| Limited Partnership (LP) | Only general partners liable | Partial |

| Limited Liability Partnership (LLP) | No personal liability for business debts | Moderate to High |

For entrepreneurs prioritizing personal asset protection, forming an LLC is typically the safer option. Partnerships, especially GPs, carry substantial risk due to unlimited liability, making them less desirable for businesses with potential legal exposure. However, LLPs and LPs can provide a middle ground, offering limited liability while maintaining the flexibility of a partnership structure.

When selecting a business entity, consulting with a business attorney or financial advisor is crucial to ensure the chosen structure aligns with liability concerns, state regulations, and long-term business goals.

Taxation differences: How are LLCs and Partnerships taxed?

While both entities benefit from pass-through taxation, they have distinct rules regarding self-employment taxes, tax deductions, and the option for LLCs to elect S Corporation status.

Pass-through taxation in both structures

Both LLCs and Partnerships are classified as pass-through entities by default. This means that profits and losses are reported directly on the owners' personal tax returns, avoiding the double taxation faced by C corporations.

- LLCs: Unless an LLC elects to be taxed as a corporation, it is treated as a disregarded entity (if single-member) or as a partnership (if multi-member). In either case, business income “passes through” to the owners' individual tax returns, where it is taxed at personal income tax rates.

- Partnerships: The IRS requires partnerships to file Form 1065 (U.S. Return of Partnership Income), but the business itself does not pay income taxes. Instead, each partner reports their share of profits and losses on Schedule K-1, which flows through to their individual Form 1040 tax return.

Self-employment taxes for LLC vs. Partnership

While both structures avoid corporate-level taxation, self-employment tax treatment can differ significantly:

- LLC members: By default, LLC members are considered self-employed and must pay self-employment taxes (Social Security and Medicare) on their entire share of business income.

- General Partners: Similar to LLC members, general partners in a partnership are subject to self-employment taxes on their distributive share of business income. However, unlike LLCs, general partners cannot take a salary; instead, they may receive guaranteed payments, which are also subject to self-employment tax.

- Limited Partners: Limited partners in a Limited Partnership (LP) are typically not subject to self-employment tax on their share of profits unless they actively participate in management. This distinction can make LPs an attractive option for passive investors.

| Entity type | Self-employment tax requirement |

|---|---|

| LLC (default) | Yes, on all business income |

| General Partnership | Yes, on all distributive share |

| Limited Partnership | No, unless actively managing |

| LLC (S Corp election) | Yes, but only on salaries (not distributions) |

Tax deductions and benefits for each

Both LLCs and partnerships can take advantage of various tax deductions, but their eligibility depends on their specific structure:

Common deductions for both LLCs and Partnerships:

- Business expenses: Rent, utilities, marketing costs, employee salaries, and office supplies.

- Home office deduction: If operating from a home office, a portion of rent and utilities may be deductible.

- Qualified Business Income (QBI) deduction: Under the Tax Cuts and Jobs Act (TCJA), LLC members and partners may deduct up to 20% of qualified business income (QBI), subject to income thresholds.

- Retirement contributions: Contributions to SEP IRAs, SIMPLE IRAs, and solo 401(k)s can provide substantial tax benefits.

- Health insurance premiums: Self-employed business owners can deduct health insurance premiums for themselves and their families.

Unique tax advantages:

- LLCs: Can elect to be taxed as an S Corporation, which reduces self-employment tax liabilities.

- Partnerships: Offer flexibility in allocating profits and losses among partners, even if not proportional to ownership percentage (as long as the allocation follows a legitimate substantial economic effect).

Electing S corporation status for an LLC

LLCs have an advantage over partnerships because they can elect S Corporation (S Corp) status for tax purposes. This election can reduce the self-employment tax burden.

- If an LLC elects to be taxed as an S Corporation, the owner can classify income into two categories:

- Salary (subject to payroll taxes): The owner must take a “reasonable salary” for work performed in the business, paying FICA taxes (Social Security and Medicare).

- Distributions (not subject to self-employment tax): The remaining business profits can be distributed as dividends, avoiding self-employment taxes.

| Tax treatment factor | LLC (Default) | LLC (S Corp election) | Partnership |

|---|---|---|---|

| Self-employment tax | Yes (on all income) | Only on salary | Yes (except for LPs) |

| Profit distribution flexibility | Moderate | Limited | High (customizable) |

| Corporate tax election | Optional (S Corp or C Corp) | S Corp | Not applicable |

While both LLCs and partnerships provide pass-through taxation, key differences in self-employment taxes, profit distribution, and tax flexibility can significantly impact overall tax liability. LLCs offer more options for tax optimization through S Corporation election, while partnerships provide greater customization in profit allocation. Choosing the right structure depends on the business model, ownership goals, and long-term tax planning strategy.

Formation and legal requirements

An LLC or a partnership comes with distinct registration requirements, compliance steps, and regulatory considerations that impact long-term operations.

An LLC and a partnership have different registration requirements

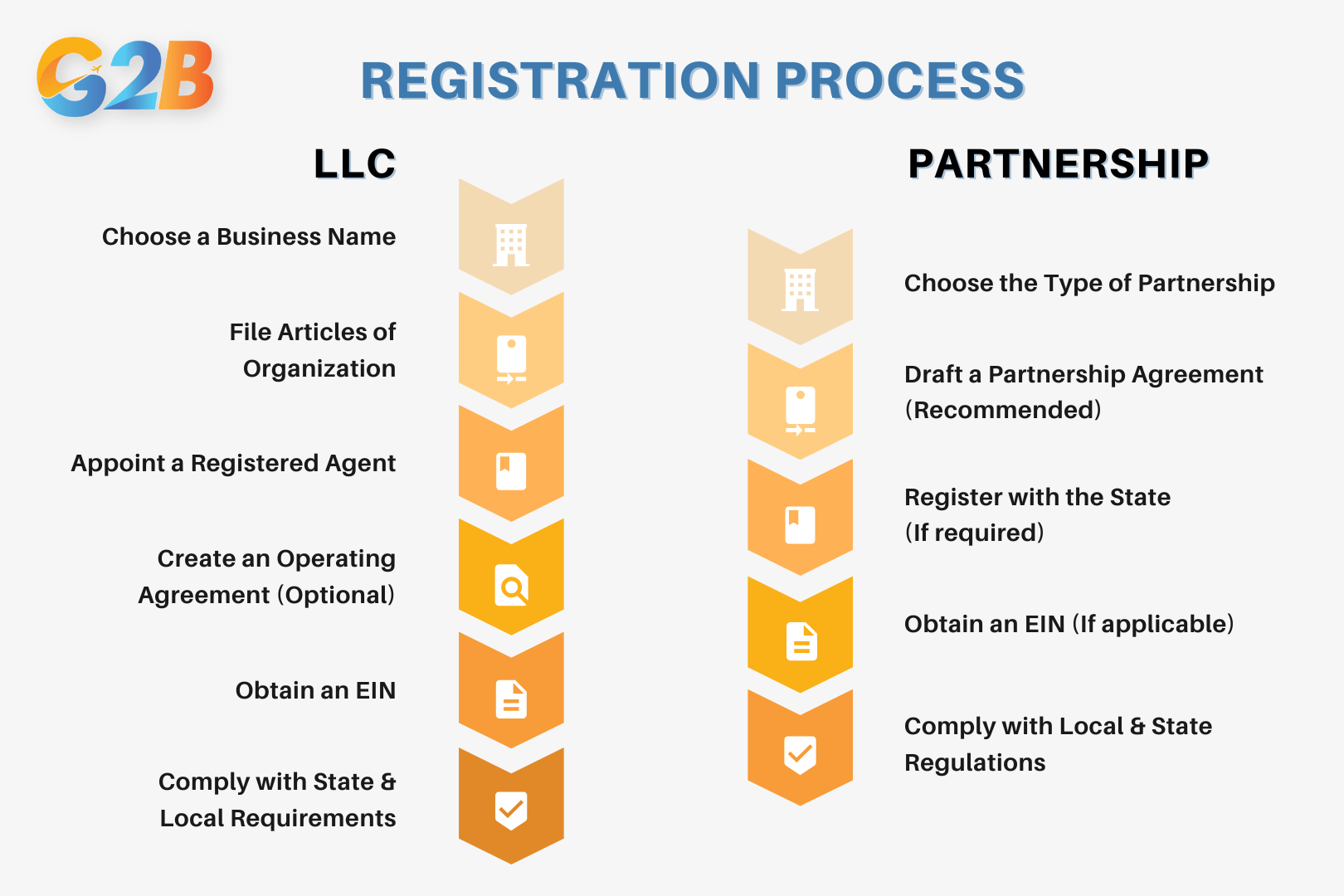

How to register an LLC (state filings & fees)

Forming a Limited Liability Company (LLC) involves several key steps that vary by state but generally follow a standardized legal process:

- Choose a business name

- Must be unique and compliant with state naming rules.

- Often required to include "LLC" or "Limited Liability Company".

- Some states prohibit specific terms that imply governmental affiliation.

- File articles of organization

- Officially registers the LLC with the state.

- Includes business name, registered agent details, and management structure.

- Filing fees range from $50 to $500, depending on the state.

- Appoint a registered agent

- Required in all states to accept legal documents on behalf of the LLC.

- Can be an individual or a professional service.

- Create an operating agreement (Optional but recommended)

- Outlines ownership structure, management roles, and operational rules.

- Helps prevent disputes among members.

- Obtain an Employer Identification Number (EIN)

- Issued by the IRS for tax purposes.

- Necessary for hiring employees, opening business bank accounts, and filing taxes.

- Comply with state and local requirements

- May include business licenses, permits, and annual reporting obligations.

- Some states impose franchise taxes or publication requirements (e.g., New York requires LLCs to publish notices in local newspapers).

Forming a Partnership: Agreements & legal steps

Partnerships have fewer formalities compared to LLCs, but legal agreements play a crucial role in defining the structure and responsibilities of partners. The formation process varies based on the type of partnership:

- Choose the type of partnership

- General Partnership (GP): No formal registration required in most states; partners share equal liability.

- Limited Partnership (LP): Requires state registration; includes general and limited partners with different liability levels.

- Limited Liability Partnership (LLP): Requires registration; provides liability protection for all partners, typically used by professional services firms.

- Draft a partnership agreement (highly recommended)

- Defines ownership percentage, profit-sharing structure, and management roles.

- Outlines procedures for partner exits, disputes, and dissolution.

- Not legally required but crucial for avoiding conflicts.

- Register with the state (If required)

- General partnerships often do not need formal registration.

- LPs and LLPs must file a Certificate of Limited Partnership or LLP registration.

- Obtain an EIN (If applicable)

- Required for tax purposes if the partnership has employees.

- Helps in opening business bank accounts.

- Comply with local and state regulations

- Certain industries require professional licenses.

- Some states impose annual reporting or franchise tax obligations.

Management structure: Who controls the business?

The management structure of an LLC differs significantly from partnerships, and understanding these distinctions is crucial for business owners aiming for efficient operations.

Member-managed vs. Manager-managed LLCs

Unlike partnerships, LLCs offer a flexible management structure, allowing owners (known as members) to choose between a member-managed or manager-managed model.

Member-managed LLCs

- In this structure, all members actively participate in the daily operations and decision-making processes.

- Suitable for small businesses or closely held LLCs where all members want equal control.

- Decisions are often made by majority vote, although the operating agreement can specify other arrangements.

- More cost-effective, as hiring external managers isn't necessary.

Manager-managed LLCs

- Members appoint one or more managers (can be members or external professionals) to handle business operations.

- Best for larger LLCs or businesses with passive investors who don’t want direct involvement.

- Members retain ownership rights but delegate operational control.

- More structured and often preferred in industries requiring specialized expertise.

Decision-making in General Partnerships

A general partnership (GP) operates on the principle of shared authority and responsibility. Unless otherwise stated in a partnership agreement:

- Each partner has equal decision-making power, regardless of capital contributions.

- Major decisions, such as taking on debt or entering contracts, typically require unanimous consent.

- Routine operational decisions may be made by any partner acting on behalf of the partnership.

- Conflicts can arise when partners disagree, emphasizing the need for a detailed partnership agreement.

Role of Limited Partners in LPs

A Limited Partnership (LP) consists of general partners (GPs) who control the business and limited partners (LPs) who invest but do not manage daily operations.

- General partners make all key business decisions and bear unlimited liability.

- Limited partners contribute capital but have no management authority and limited liability.

- Limited partners can lose their liability protection if they engage in management activities.

How LLPs distribute management responsibilities

A Limited Liability Partnership (LLP) combines elements of a general partnership and an LLC, offering flexibility while protecting partners from personal liability.

- Unlike LPs, all partners in an LLP can participate in management.

- Partners typically have equal control, but management duties can be allocated differently in the partnership agreement.

- Common in professional service firms (e.g., law firms, accounting firms) where partners have expertise in different areas.

Comparison of management structures

| Business structure | Who manages the business? | Decision-making process |

|---|---|---|

| Member-managed LLC | All members equally | Majority vote or unanimous consent |

| Manager-managed LLC | Designated manager(s) | Managers control daily operations |

| General Partnership | All partners equally | Unanimous consent for major decisions |

| Limited Partnership | General partners | General partners control, limited partners invest |

| Limited Liability Partnership | All partners can participate | Management structure depends on agreement |

The right management structure depends on factors such as business size, industry, level of involvement desired by owners, and long-term goals. LLCs offer flexibility, GPs emphasize shared control, LPs separate management from investment, and LLPs balance liability protection with management participation. Understanding these distinctions ensures that business owners select a structure that aligns with their strategic vision and operational needs.

Profit distribution and financial management

Understanding how each structure allocates profits, manages capital, and resolves financial disputes is essential for business owners looking to make informed decisions.

How LLCs allocate profits and losses

Limited Liability Companies (LLCs) offer flexibility in how profits and losses are distributed among members. Unlike partnerships, where profit distribution typically follows ownership percentage, LLCs can allocate profits based on an operating agreement. Here’s how LLCs handle profit allocation:

- Default allocation (pro-rata basis): In the absence of a specific agreement, profits and losses are typically allocated based on the percentage of ownership interest in the LLC.

- Custom allocation (operating agreement): LLCs allow members to agree on non-proportional profit distribution. This can be structured based on capital contributions, involvement in management, or other factors.

- Pass-through taxation: Profits and losses pass through to members' personal tax returns, reducing double taxation. However, LLCs can elect to be taxed as an S corporation or C corporation, impacting profit distribution.

- Capital accounts: Each member has a capital account tracking their contributions, withdrawals, and allocated profits. These accounts ensure equitable financial tracking and taxation compliance.

How Partnerships distribute income among partners

Partnerships, including general, limited, and limited liability partnerships, follow structured rules for profit distribution:

- Default distribution (equal sharing): In general partnerships, profits are typically split equally unless a partnership agreement states otherwise.

- Capital contribution-based allocation: Limited partnerships often allocate profits based on the percentage of total investment made by each partner.

- Guaranteed payments: Some partners, especially in professional partnerships (e.g., law firms, accounting firms), receive guaranteed payments before profit distribution.

- Pass-through taxation: Just like LLCs, partnerships do not pay federal income tax; instead, profits pass through to partners’ individual tax returns, where they pay taxes based on their share of income.

- Loss allocation: Losses are distributed in the same manner as profits, unless otherwise stated in the agreement. Limited partners in an LP may have restrictions on loss deductions based on at-risk rules.

Key difference from LLCs: Partnerships typically follow strict pro-rata profit-sharing rules unless an agreement modifies them, whereas LLCs allow greater customization.

Managing business finances and capital contributions

Sound financial management ensures the stability and longevity of a business. LLCs and partnerships approach capital contributions and financial management differently:

| Factor | LLC | Partnership |

|---|---|---|

| Initial capital | Members contribute per agreement | Partners contribute per agreement |

| Additional capital contributions | Can require unanimous approval or per agreement | Often required based on need, not always equal |

| Debt liability | Limited liability for members | General partners have unlimited liability, limited partners are protected |

| Cash flow management | Can distribute funds as per agreement | Often structured around working capital needs |

| Financial records | Formal bookkeeping recommended | Bookkeeping required, but often less structured |

- Capital contributions in LLCs: Members can contribute cash, property, or services, and additional contributions may be required based on financial needs.

- Capital contributions in Partnerships: Contributions are often more flexible, with each partner contributing based on agreement terms, but general partners are personally liable for debts.

Industry-specific considerations: Which is better for your business?

Different business sectors have distinct operational, legal, and financial needs, making one structure more advantageous than the other. Below, let’s explore how LLCs and partnerships compare in key industries.

LLC vs. Partnership for startups and small businesses

Startups and small businesses often prioritize flexibility, ease of formation, and access to funding. Here’s how each structure performs in this context:

LLC advantages:

- Limited Liability Protection: Founders aren’t personally liable for debts, which is crucial if the business takes on loans or external investments.

- Credibility with investors: LLCs appear more structured and reliable, often a prerequisite for securing venture capital or bank loans.

- Tax flexibility: Startups can elect to be taxed as a corporation if they plan to reinvest profits rather than distribute them.

Partnership advantages:

- Ease of formation: General partnerships require minimal paperwork, allowing entrepreneurs to start quickly.

- Pass-through taxation simplicity: Profits are taxed only at the individual level, avoiding corporate tax obligations.

- Less regulatory compliance: No need for annual reports or complex corporate governance structures.

If a startup intends to seek investors and scale, an LLC is the superior choice. For small businesses with a simple operational model, a partnership may be more efficient.

Best choice for professional services (law firms, accounting, etc.)

Professional service businesses - including law firms, consulting firms, and medical practices - should consider liability protection, taxation, and licensing regulations.

LLC advantages:

- Limited Liability Protection: Professionals are shielded from personal liability related to business debts and obligations.

- Structured management: LLCs allow members to define clear management roles and decision-making processes.

- Flexible profit distribution: Income can be allocated based on contributions or predefined agreements rather than equal splits.

Partnership advantages:

- Better for professional groups: Many states require law firms and accounting firms to operate as limited liability partnerships (LLPs) rather than LLCs.

- Pass-through taxation: Partnerships allow firms to avoid double taxation while distributing profits more efficiently.

- Shared management: Ideal for businesses where partners have equal expertise and decision-making power.

Professional service businesses should check state regulations. If LLPs are permitted, they offer an optimal mix of liability protection and tax advantages. If not, an LLC is the safer option.

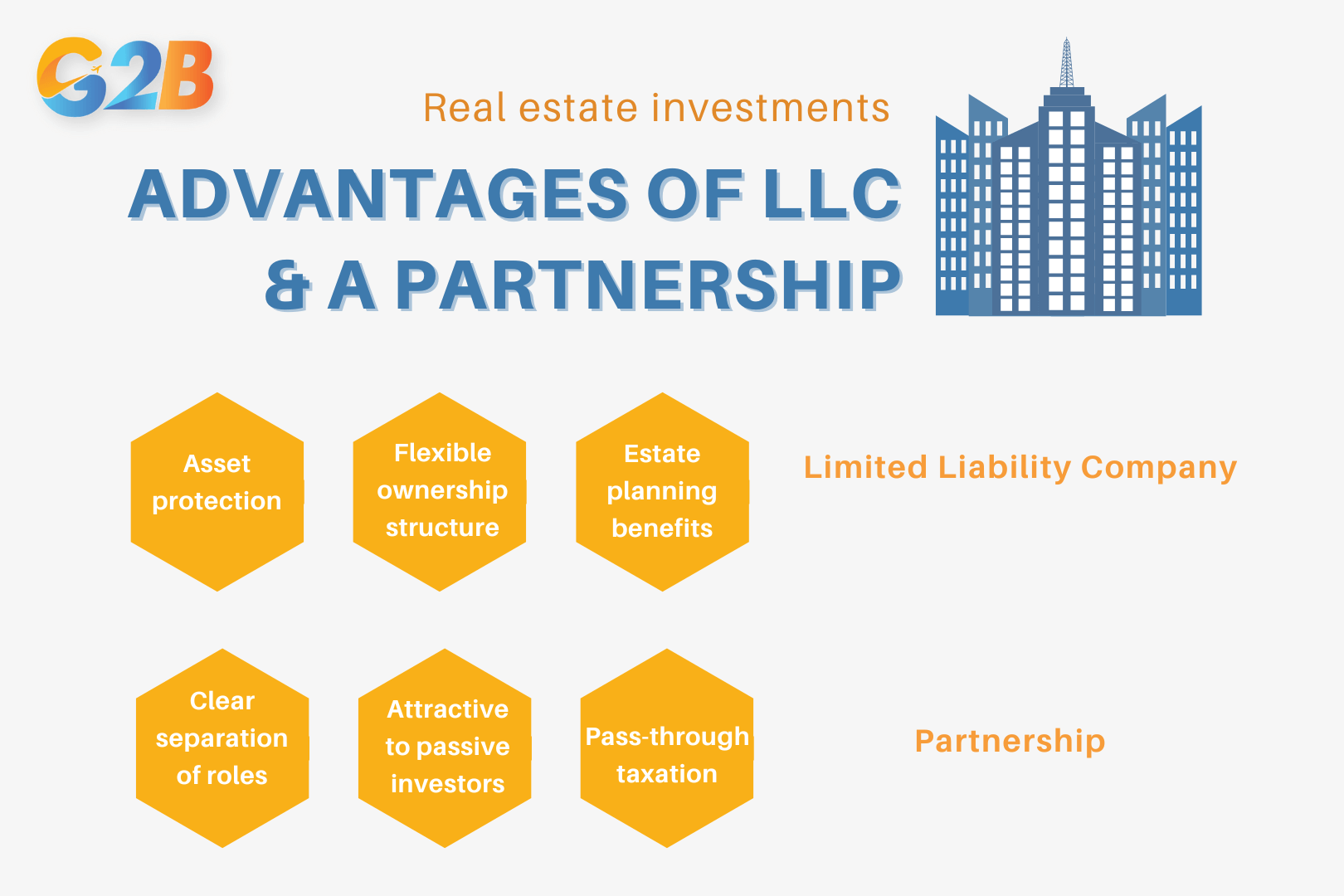

Real estate investments: LLC vs. Limited Partnerships

Real estate investors and developers need to balance liability protection, asset ownership structures, and tax efficiency.

Advantages of LLC and a partnership for real estate investments

LLC advantages:

- Asset protection: Each property can be placed under a separate LLC to shield owners from liabilities.

- Flexible ownership structure: Investors can join as passive members without management obligations.

- Estate planning benefits: Ownership interests in an LLC can be transferred more easily than partnership shares.

Limited Partnership (LP) advantages:

- Clear separation of roles: General partners handle management, while limited partners provide capital without taking on liability.

- Attractive to passive investors: LPs are commonly used in large real estate syndications and private equity deals.

- Pass-through taxation: Profits and losses are passed directly to investors, reducing tax burdens.

LLCs work best for individual property investors or those managing multiple properties. Limited partnerships are preferable for large real estate developments involving multiple passive investors.

Pros and cons: Making the right choice

Choosing between a Limited Liability Company (LLC) and a General Partnership is an important decision with each structure having distinct advantages and drawbacks.

Pros and cons of an LLC

An LLC offers strong liability protection, flexible taxation options, and operational versatility, making it a popular choice for entrepreneurs. However, it also comes with potential drawbacks, such as state-specific regulations, higher administrative costs, and possible self-employment taxes.

Pros:

- Limited Liability Protection

- Members are generally not personally responsible for business debts and liabilities.

- Protects personal assets from lawsuits or creditor claims.

- Flexible taxation options

- By default, LLCs have pass-through taxation, meaning profits and losses flow through to members' personal tax returns, avoiding double taxation.

- Can elect to be taxed as an S Corporation or C Corporation for additional tax advantages.

- Operational flexibility

- No strict ownership restrictions; can be owned by individuals, corporations, or other LLCs.

- Can choose member-managed or manager-managed structures for decision-making.

- Credibility and investor appeal

- LLCs are seen as more legitimate and stable compared to partnerships, making it easier to attract investors and secure funding.

- Banks and lenders may prefer lending to LLCs due to their formal structure.

- Ease of ownership transfer

- Ownership stakes can be transferred through an Operating Agreement without dissolving the LLC.

Cons:

- Higher costs and compliance requirements

- LLCs require state registration, annual reports, and compliance fees, which can be costly compared to partnerships.

- Some states impose franchise taxes or other fees.

- Self-employment taxes

- Members must pay self-employment taxes (Social Security and Medicare) on their share of profits, which can be higher than the tax obligations of a general partnership.

- Complexity in formation and maintenance

- Requires formal documentation like an Operating Agreement, Articles of Organization, and EIN registration.

- More administrative overhead than a general partnership.

Pros and cons of a General Partnership

A General Partnership is easy to establish, offers pass-through taxation, and allows for flexible management, making it an attractive option for small businesses. However, it also comes with significant drawbacks, including unlimited personal liability for business debts, potential conflicts between partners, and difficulty in securing external funding.

Pros:

- Simple and low-cost formation

- No formal state registration required; can be formed through a verbal or written agreement.

- Fewer compliance obligations and lower maintenance costs.

- Pass-through taxation

- Business income is not taxed at the entity level, avoiding corporate taxation.

- Profits and losses pass directly to partners’ personal tax returns, which may lead to tax benefits.

- Flexible profit distribution

- Partnerships can allocate profits and losses as agreed upon, rather than based on ownership percentages.

- This can be useful for structuring compensation and reinvestment strategies.

- Shared decision-making

- Each partner typically has an equal say in business decisions, fostering collaboration and shared responsibility.

- Less paperwork and compliance

- No requirement for annual reports or complex legal filings (depending on state laws).

Cons:

- Unlimited personal liability

- Partners are personally liable for business debts and legal actions.

- Each partner is also liable for the actions of the other partners (joint and several liability).

- Difficulty in raising capital

- Investors and banks are often hesitant to fund partnerships due to their informal structure.

- Cannot issue stocks or membership units like an LLC or corporation.

- Potential for disputes

- Equal decision-making can lead to conflicts if partners disagree on business direction.

- Without a partnership agreement, resolving disputes or dissolving the partnership can be legally complex.

- Complicated succession planning

- If a partner leaves or passes away, the partnership may be automatically dissolved unless otherwise specified in a written agreement.

When to choose an LLC over a Partnership

- If liability protection is a priority - LLC members are shielded from personal liability, while partners in a general partnership are fully exposed.

- If long-term growth and funding are essential - An LLC’s structure provides credibility and investment potential.

- If operational flexibility is needed - LLCs allow customized management structures and ownership arrangements.

- If planning for ownership transfer - LLC ownership can be reassigned without dissolving the entity, unlike partnerships.

When a Partnership might be the better choice

- If simplicity and low costs are the main concern - General partnerships have fewer legal and financial burdens.

- If partners are comfortable with liability risks - In small or low-risk businesses, partners may not be concerned about liability.

- If taxation flexibility is a priority - Pass-through taxation and flexible profit distribution can be more beneficial than LLC taxation in certain cases.

- If the business is based on professional services - Many law firms, accounting firms, and consultancies operate as partnerships for tax and liability reasons.

Choosing between an LLC and a partnership depends on factors such as risk tolerance, taxation preferences, funding needs, and business goals. By weighing the pros and cons of each structure, business owners can make an informed decision that aligns with their strategic vision.

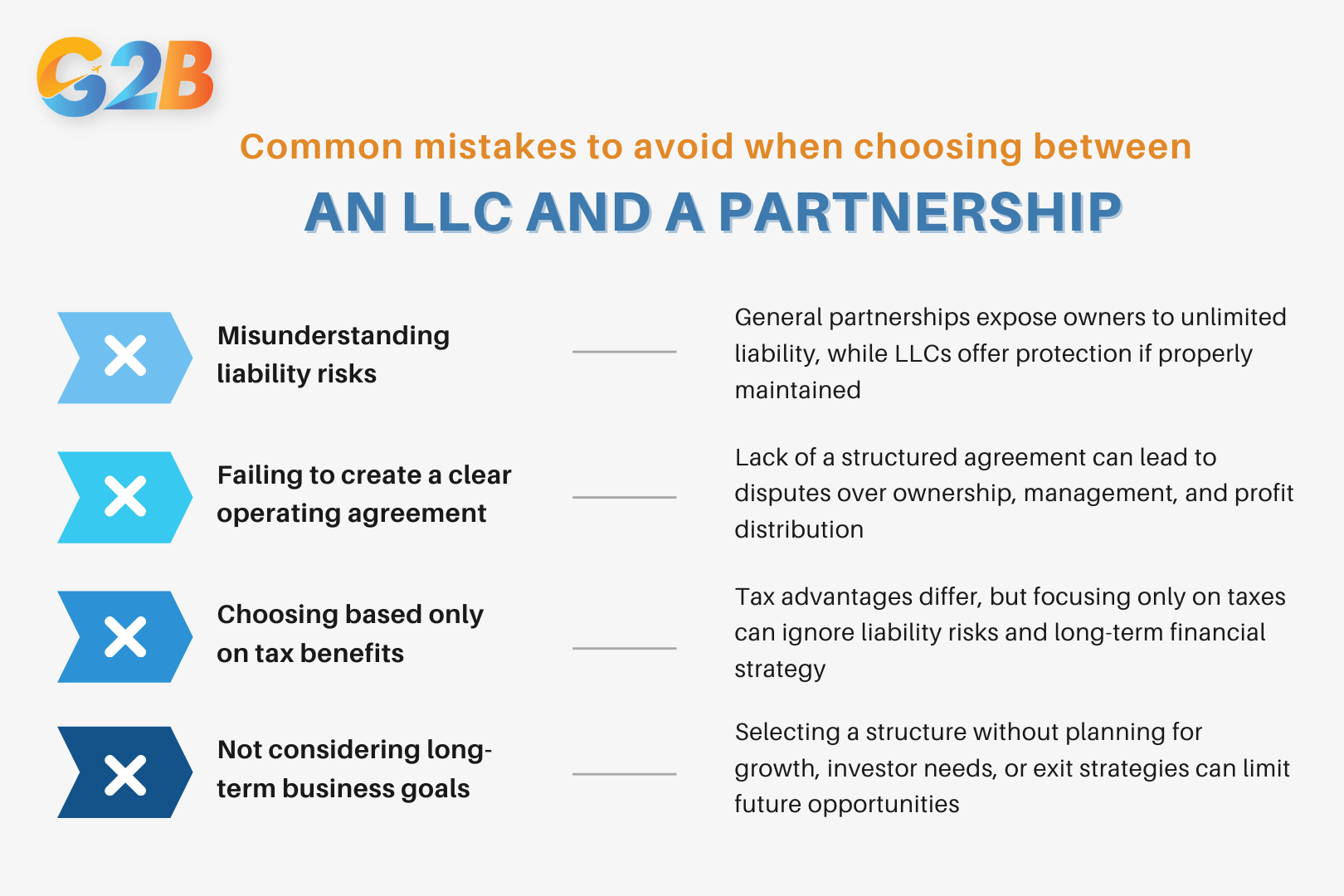

Common mistakes to avoid when choosing between an LLC and a Partnership

Missteps can lead to financial losses, legal disputes, and strategic limitations. Below, let’s investigate the most common mistakes and how to avoid them.

Common mistakes to avoid when choosing between an LLC and a Partnership

1. Misunderstanding liability risks

One of the biggest mistake is underestimating the liability risks associated with different business structures.

- General Partnerships expose owners to unlimited liability, meaning each partner is personally responsible for business debts and legal claims. If one partner makes a bad business decision or incurs debt, all partners are liable.

- LLCs offer limited liability protection, shielding personal assets from business debts and lawsuits. However, liability protection can be lost if an LLC is not properly maintained (e.g., failing to separate business and personal finances).

- Limited Partnerships (LPs) and Limited Liability Partnerships (LLPs) have hybrid liability protections, but general partners in an LP still carry unlimited liability.

How to avoid this mistake:

- Evaluate industry-specific liability risks before choosing a structure.

- Ensure that the LLC follows compliance rules to maintain limited liability protection.

- Consider obtaining business insurance for additional risk mitigation.

2. Failing to create a clear operating agreement

A defined operating agreement (LLC) or partnership agreement can cause serious conflicts among business owners.

- Many General Partnerships operate on verbal agreements, which can lead to disputes over profit distribution, management responsibilities, and partner exit strategies.

- LLCs also require a well-structured Operating Agreement to establish ownership percentages, voting rights, decision-making processes, and buyout provisions.

- Without a proper agreement, state default laws may apply, which may not align with the owners’ intentions.

How to avoid this mistake:

- Draft a formal agreement outlining roles, responsibilities, dispute resolution mechanisms, and exit strategies.

- Consult a business attorney to ensure the agreement is legally binding and comprehensive.

- Regularly update agreements as the business evolves.

3. Choosing based only on tax benefits

Taxation is a key factor, but it should not be the sole reason for selecting a business structure. Many business owners mistakenly assume:

- Partnerships are always more tax-efficient due to pass-through taxation, ignoring liability risks and management complexities.

- LLCs always offer better tax advantages, without considering self-employment taxes and potential double taxation (if electing corporate taxation).

- Short-term tax savings matter more than long-term financial strategy.

Comparing tax considerations:

| Factor | LLC | Partnership |

|---|---|---|

| Default taxation | Pass-through taxation | Pass-through taxation |

| Self-employment taxes | LLC members may pay higher self-employment taxes | Partners also pay self-employment taxes |

| Corporate tax option | Can elect S-Corp or C-Corp taxation | Not available in General Partnerships |

| Profit allocation flexibility | Can allocate profits in any agreed manner | Profit and losses are typically divided based on ownership percentage |

How to avoid this mistake:

- Consult a tax professional to analyze the long-term impact of different structures.

- Consider liability protection, ownership flexibility, and management needs alongside tax implications.

- Reassess tax strategies as business revenue grows.

4. Not considering long-term business goals

Many entrepreneurs choose an entity based on immediate convenience rather than long-term business scalability and exit strategies.

- Partnerships may seem easier at first due to minimal paperwork, but they lack growth-friendly features like issuing shares to investors.

- LLCs provide more flexibility, but they may not be ideal for businesses planning to go public or attract venture capital.

- Failing to consider succession planning can lead to legal complications if a partner or member decides to leave the business.

How to avoid this mistake:

- Consider future business growth, funding needs, and exit strategies before choosing a structure.

- If planning for external investors or public offering, explore options like C-Corp conversion.

- Include succession planning in the operating or partnership agreement.

Avoiding these common mistakes requires careful planning and professional guidance. Entrepreneurs should weigh liability risks, tax implications, management preferences, and long-term goals before choosing between an LLC and a Partnership. Consulting with a business attorney and tax advisor can help prevent costly mistakes and ensure the selected structure aligns with both current and future business needs.

Frequently asked questions (FAQs) about LLCs and Partnerships

This FAQ section answers common questions to provide clarity on LLCs and Partnerships’s key features, benefits, and potential challenges.

What are the key differences between an LLC and a Partnership?

While LLCs and partnerships both serve as business structures allowing multiple owners, they differ significantly in liability protection, taxation, and management structure:

| Aspect | LLC | Partnership |

|---|---|---|

| Liability protection | Members are not personally liable for business debts. | Partners have unlimited liability unless in an LLP or LP. |

| Taxation | Pass-through taxation by default, with the option to elect corporate taxation. | Pass-through taxation; profits and losses are reported on partners’ tax returns. |

| Management | Flexible; can be managed by members or managers. | General partners have equal management rights. |

| Formation | Requires state registration and compliance obligations. | Can be formed informally but may require state registration for LPs and LLPs. |

| Profit distribution | Profits are distributed as per the operating agreement. | Typically shared equally unless specified in a partnership agreement. |

LLCs provide liability protection and greater flexibility, while partnerships often require less paperwork but expose partners to personal liability.

Which is better for tax purposes: LLC or Partnership?

It depends on the business structure and tax objectives:

- LLCs are taxed as pass-through entities by default, meaning profits and losses flow through to members' tax returns. However, they can elect to be taxed as S corporations or C corporations, which may offer tax benefits depending on business income.

- Partnerships follow pass-through taxation rules, where partners report business income on their individual tax returns.

Key tax considerations:

- Self-employment taxes: LLC members pay self-employment taxes on the entire net income, while an S-corp election may reduce self-employment tax obligations.

- Deductions: Both LLCs and partnerships can deduct business expenses, but LLCs taxed as S-corps may allow members to classify some income as distributions instead of salary.

- Flexibility: LLCs have greater flexibility in tax classification, making them more adaptable for tax planning.

For businesses expecting significant income, consulting a tax advisor can help determine the best structure for minimizing tax liabilities.

How do I convert a Partnership into an LLC?

Converting a partnership into an LLC involves several steps:

- Check state laws: Each state has different regulations regarding conversions.

- Draft an operating agreement: Outline ownership structure, management, and profit-sharing rules.

- File articles of organization: Submit formation documents with the state’s business registration office.

- Obtain an EIN (Employer Identification Number): If the partnership had an EIN, a new one is required for the LLC.

- Transfer assets and contracts: Move business assets, liabilities, and contracts to the LLC.

- Update business licenses and bank accounts: Ensure all necessary permits and accounts reflect the new structure.

Some states allow a statutory conversion, making the transition smoother. Consulting an attorney or CPA can help ensure compliance.

What factors should I consider when choosing between these structures?

Selecting between an LLC and a partnership depends on multiple factors:

- Liability protection: If shielding personal assets is a priority, an LLC is the better choice.

- Tax considerations: Partnerships and LLCs offer pass-through taxation, but LLCs have more flexibility to elect corporate taxation.

- Formation & maintenance costs: LLCs require state filings and annual fees, whereas partnerships may have lower initial costs.

- Management flexibility: Partnerships operate under equal management rights unless otherwise stated in an agreement, while LLCs allow customized structures.

- Long-term business goals: If planning to raise funds or sell ownership shares in the future, an LLC may provide better opportunities.

Deciding between an LLC and a Partnership requires a careful evaluation of business objectives, liability concerns, and operational preferences. An LLC offers strong legal protection and flexibility, making it well-suited for those prioritizing asset security and long-term growth. In contrast, a Partnership provides a simpler, cost-effective structure but comes with unlimited personal liability. The right choice depends on the balance between protection, control, and administrative complexity.

Looking for more insights? Explore our in-depth guide on company formation or connect with G2B for expert consultation tailored to your unique needs. With a commitment to reliability and precision, G2B offers professional business support services in Delaware, guiding entrepreneurs through every stage of business registration with confidence.