Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom In recent years, Limited Liability Companies (LLCs) and Limited Liability Partnerships (LLPs) have emerged as prominent choices for entrepreneurs seeking flexibility and protection. Notably, the fiscal year 2023-2024 witnessed a record high in incorporations, with 185,314 companies and 58,990 LLPs registered, reflecting a substantial increase from the previous year. Understanding the distinctions between LLC vs. LLP is vital for aligning these structures with specific business goals and operational preferences.

Understanding the basics of LLC and LLP

LLC and LLP have distinct legal and operational characteristics, making them suitable for different types of businesses and professional groups.

What is an LLC? Definition and key features

A limited liability company (LLC) is a business entity that combines elements of corporations and partnerships. It provides limited liability protection to its owners, meaning their personal assets are generally protected from business debts and lawsuits.

Key characteristics of an LLC:

- Liability protection: Members' personal assets (e.g., homes, savings) are protected from business debts and lawsuits.

- Tax flexibility: An LLC can be taxed as a sole proprietorship, partnership, S corporation, or C corporation, depending on the owner's election.

- Management options: An LLC can be member-managed (owners run the business) or manager-managed (owners appoint managers).

- Formation requirements: Requires filing Articles of Organization with the state and may need an operating agreement to define ownership and management rules.

What is an LLP? Definition and key features

A limited liability partnership (LLP) is a business structure designed primarily for professional service providers, such as law firms, accounting firms, and medical practices. Unlike LLCs, which can be formed by any business, LLPs are often restricted to licensed professionals in many states.

Key characteristics of an LLP:

- Liability protection: Partners are not personally liable for the negligence or misconduct of other partners but may still be liable for their own actions. The liability protection in an LLP varies by state. For example, some states provide full protection to all partners, while others only shield against malpractice claims.

- Taxation: LLPs are pass-through entities, meaning profits and losses are reported on partners' personal tax returns, avoiding corporate-level taxation.

- Management structure: Generally, all partners share management responsibilities unless otherwise specified in a partnership agreement.

- Formation requirements: Requires filing LLP registration documents with the state, along with a partnership agreement outlining roles, responsibilities, and profit-sharing.

Key differences between LLC and LLP at a glance

| Feature | Limited Liability Company (LLC) | Limited Liability Partnership (LLP) |

|---|---|---|

| Liability Protection | Protects personal assets from business debts and lawsuits | Shields partners from each other's negligence, but personal liability varies by state |

| Taxation | Can choose to be taxed as a sole proprietorship, partnership, S corp, or C corp | Always a pass-through entity (profits/losses go to personal tax returns) |

| Management | Member-managed or manager-managed | Typically partner-managed, with shared decision-making |

| Formation Requirements | File Articles of Organization, create an Operating Agreement | Register as an LLP, draft a Partnership Agreement |

| Best for | Startups, small businesses, real estate investors, online businesses | Professional services (law firms, accountants, architects) |

Both LLCs and LLPs offer limited liability, but their applications differ significantly. LLCs are ideal for entrepreneurs seeking tax flexibility and operational freedom, while LLPs cater to professionals who require liability protection from their partners' actions. Understanding these differences ensures business owners make the right choice based on their industry, liability concerns, and growth objectives.

Liability protection: Which structure offers more security?

Each structure protects personal assets from business liabilities differently. While both provide a layer of protection, the scope and effectiveness of that protection vary significantly based on state laws, business operations, and ownership structure.

How LLCs protect personal assets

One of the primary advantages of forming an LLC is its strong liability shield, which separates personal assets from business debts and legal claims:

- Limited personal liability: Members (owners) are not personally responsible for the LLC's debts or legal obligations unless they personally guarantee a loan or engage in fraudulent or negligent activities.

- Protection from lawsuits: If the business faces a lawsuit, the claimant can typically only go after the company's assets, not the members' personal savings, homes, or vehicles.

- Charging order protection: In many states, an LLC's structure helps protect an owner's interest from personal creditors, meaning that even if a member has personal debts, creditors may not have direct access to company assets.

- Piercing the corporate veil: While LLCs provide strong liability protection, courts may “pierce the veil” if owners fail to maintain proper corporate formalities, mix personal and business finances, or commit fraud.

Liability shield in LLPs: What partners need to know?

LLPs offer a different form of liability protection, primarily designed for professional service firms (e.g., law firms, accounting firms, and medical practices). The key aspects of LLP liability protection include:

- Protection from partner negligence: A major advantage of an LLP is that partners are not personally liable for the misconduct or negligence of other partners. For example, if one partner commits malpractice, the other partners are shielded from liability.

- Business debts and obligations: LLP partners remain personally liable for business debts unless explicitly shielded by state laws or partnership agreements.

- Personal risk exposure: Unlike an LLC, an LLP does not always provide full protection against general business liabilities, meaning partners may still face some financial exposure.

- State variations: The degree of liability protection for LLPs varies by state. Some states, like Texas and New York, provide stronger protection, while others limit LLPs to specific professions.

State-specific variations in liability protection

Both LLCs and LLPs operate under state-specific regulations, which can significantly impact liability protection. Here are key variations to consider:

| Factor | LLC | LLP |

|---|---|---|

| State recognition | Available in all 50 states | Recognized in most states, but some restrict LLPs to certain professions |

| Liability for business debts | Generally protected | Varies by state; some states hold partners personally liable |

| Protection from partner misconduct | N/A (members are not personally liable for co-owners) | Yes, partners are shielded from others' professional malpractice |

| Charging order protection | Strong in some states (e.g., Delaware, Nevada) | Typically not applicable |

| Best suited for | Small businesses, real estate investors, and startups | Professional service firms (law, accounting, medicine) |

When comparing LLCs and LLPs, an LLC generally offers stronger personal asset protection from business debts and lawsuits, making it a better option for most entrepreneurs and business owners. On the other hand, LLPs are tailored for professionals who want to shield themselves from partner negligence while maintaining flexibility in management.

Taxation: How LLCs and LLPs are taxed

Choosing the right business structure is necessary for tax efficiency. Both Limited Liability Companies (LLCs) and Limited Liability Partnerships (LLPs) benefit from pass-through taxation, but they differ in tax flexibility and obligations.

Pass-through taxation: How it works for both structures

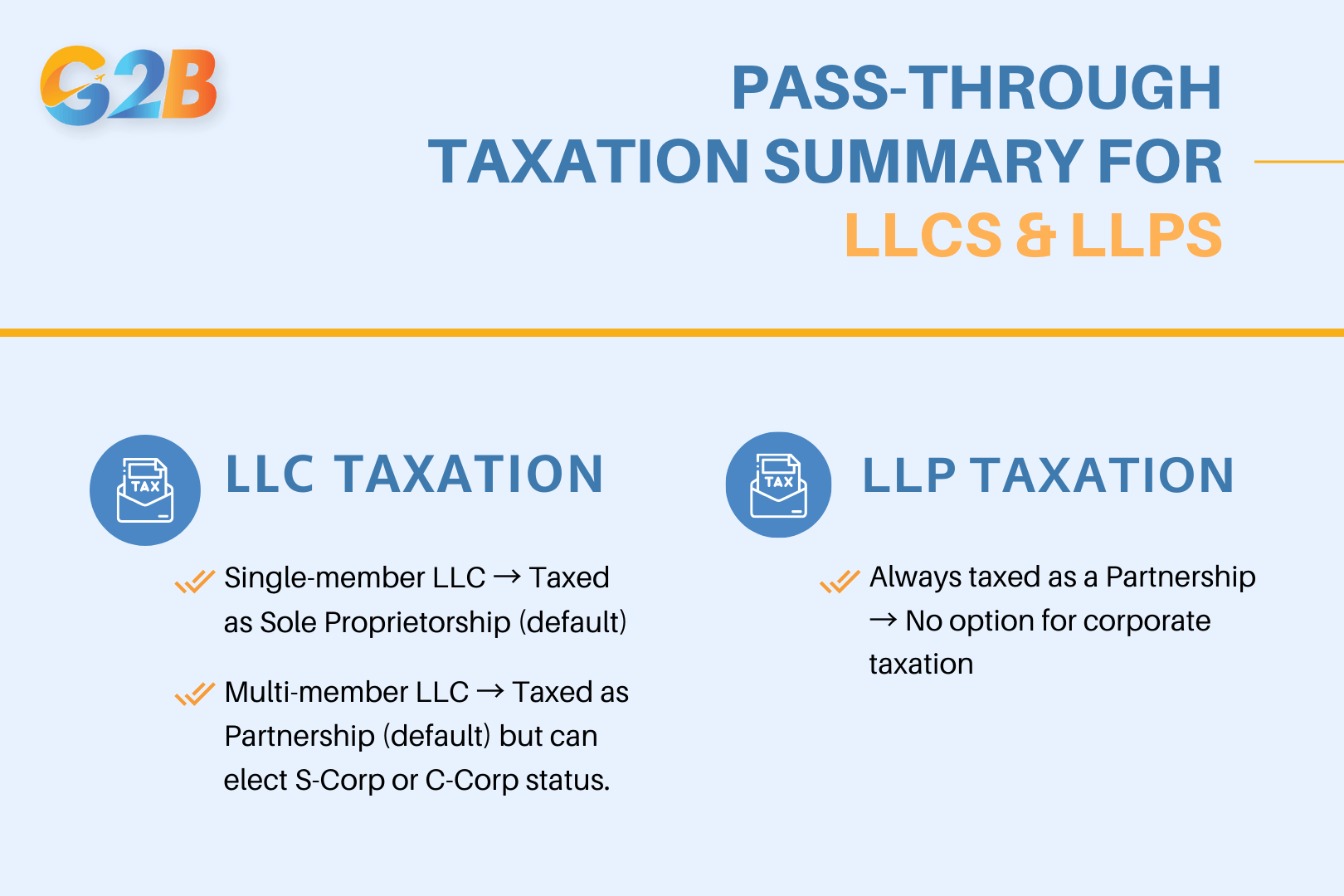

Both LLCs and LLPs are classified as pass-through entities by default. This means that the business itself does not pay federal income tax. Instead, profits and losses “pass-through” to the owners, who report them on their personal tax returns.

- LLCs: Single-member LLCs are taxed as sole proprietorships by default, while multi-member LLCs are taxed as partnerships unless an election is made to be treated as an S-corporation or C-corporation.

- LLPs: Always taxed as a partnership, meaning each partner reports their share of the business income on their individual tax returns. LLPs cannot elect to be taxed as a corporation.

- Implications:

- Profits are subject to self-employment tax in both structures.

- Business losses can offset other income on the owners' tax returns, reducing overall tax liability.

Both LLCs and LLPs are classified as pass-through entities by default

Taxation options for LLCs: Sole prop, S-corp, C-corp election

LLCs offer tax flexibility, allowing members to choose. This is a major advantage over LLPs.

| Tax classification | Description | Best for |

|---|---|---|

| Sole proprietorship (Single-member LLCs) | Default classification; income is reported on Schedule C of the owner's personal tax return. | Small businesses with low administrative burden. |

| Partnership (Multi-member LLCs) | Default classification for multi-member LLCs; profits and losses are divided among members based on ownership percentage. | Small businesses with multiple owners who want simple taxation. |

| S-Corporation election | Owners pay themselves a “reasonable salary” and take the remaining profits as distributions, reducing self-employment tax. | Businesses with high net profits (above ~$50,000) that want to lower self-employment tax. |

| C-Corporation election | LLC is taxed separately from owners, and profits are subject to corporate tax. It can result in double taxation (corporate + dividend tax). | Businesses seeking outside investors or planning for future IPO. |

Key takeaway: LLPs do not have these election options; they are always taxed as partnerships. LLC owners, however, can optimize their tax strategy based on business goals.

Self-employment tax: Which entity has a tax advantage?

Self-employment tax (Social security and medicare) is an important factor when comparing LLCs and LLPs:

- LLCs electing S-corp taxation: Owners can take part of their income as a salary (subject to payroll tax) and the rest as distributions, which are not subject to self-employment tax.

- LLPs: Partners must report all income as self-employment earnings, paying the full self-employment tax.

- Example comparison:

- LLP partner earning $100,000 pays self-employment tax on the full amount.

- LLC (S-corp) owners with $100,000 profit could pay themselves a $60,000 salary (subject to payroll taxes) and take the remaining $40,000 as a distribution (exempt from self-employment tax).

While both LLCs and LLPs enjoy pass-through taxation, LLCs offer more flexibility, including the ability to elect S-corp or C-corp status. This can lead to significant tax savings, especially for businesses with high earnings. LLPs, however, remain a straightforward structure for professional services firms where corporate tax elections are unnecessary. Business owners should consult a tax professional to determine the best strategy for their specific financial situation.

Management and ownership structures compared

Choosing between a Limited Liability Company (LLC) and a Limited Liability Partnership (LLP) requires a deep understanding of how management and ownership are structured in each business entity.

Member-managed vs. manager-managed LLCs

An LLC provides business owners (members) with two primary management structures:

- Member-managed LLC - All members actively participate in daily operations and decision-making. This structure is common among small businesses and startups where owners want direct control over operations.

- Manager-managed LLC - Members appoint one or more managers to handle operations. Managers can be members themselves or external professionals. This structure suits larger LLCs or those with passive investors who prefer not to be involved in daily management.

Key differences:

| Feature | Member-managed LLC | Manager-managed LLC |

|---|---|---|

| Decision-making | Shared among all members | Centralized with designated managers |

| Operational control | Hands-on by all members | Delegated to managers |

| Suitability | Small businesses, startups | Larger LLCs, passive investors |

| Complexity | Less complex, fewer formalities | More structured, requires oversight |

Partner roles and responsibilities in LLPs

Unlike LLCs, LLPs operate under a partnership model, where each partner plays a distinct role:

- General partners - Have active management responsibilities and decision-making authority.

- Silent (or passive) partners - Contribute capital but have limited or no involvement in daily operations.

Partners in an LLP typically share management responsibilities equally unless stated otherwise in the partnership agreement. This agreement defines:

- Profit and loss distribution

- Voting rights and decision-making processes

- Roles and responsibilities of each partner

- Dispute resolution mechanisms

One major distinction of LLPs is joint management, where all active partners share control, unlike LLCs, which can opt for centralized management.

Flexibility in decision-making and operational control

One of the most significant factors in choosing between an LLC and an LLP is the flexibility of decision-making and operational control.

- LLCs provide structured flexibility - Members can choose between a democratic (member-managed) or centralized (manager-managed) approach. LLCs also allow for an operating agreement, which can be customized to define decision-making authority, voting rights, and operational procedures.

- LLPs rely on equal partnership participation - Unless explicitly defined in the partnership agreement, all partners have an equal say in major business decisions. This structure works well for professional services firms, such as law firms and accounting firms, where collective decision-making is preferred.

Which is better for control?

- If you prefer centralized decision-making, an LLC with a manager-managed structure may be ideal.

- If you want equal partner involvement, an LLP offers a framework that fosters collective responsibility.

Both LLCs and LLPs offer flexible management structures, but their approach to ownership, decision-making, and operational control varies. LLCs allow customization through operating agreements, making them more adaptable to different business models, while LLPs emphasize joint management, making them ideal for professional service providers.

Formation process & legal requirements

While both structures offer limited liability, their registration procedures, documentation requirements, and state-specific regulations differ significantly. Below is a breakdown of establishing each entity and key legal considerations.

The process of forming a limited liability company (LLC) and limited liability partnership (LLP)

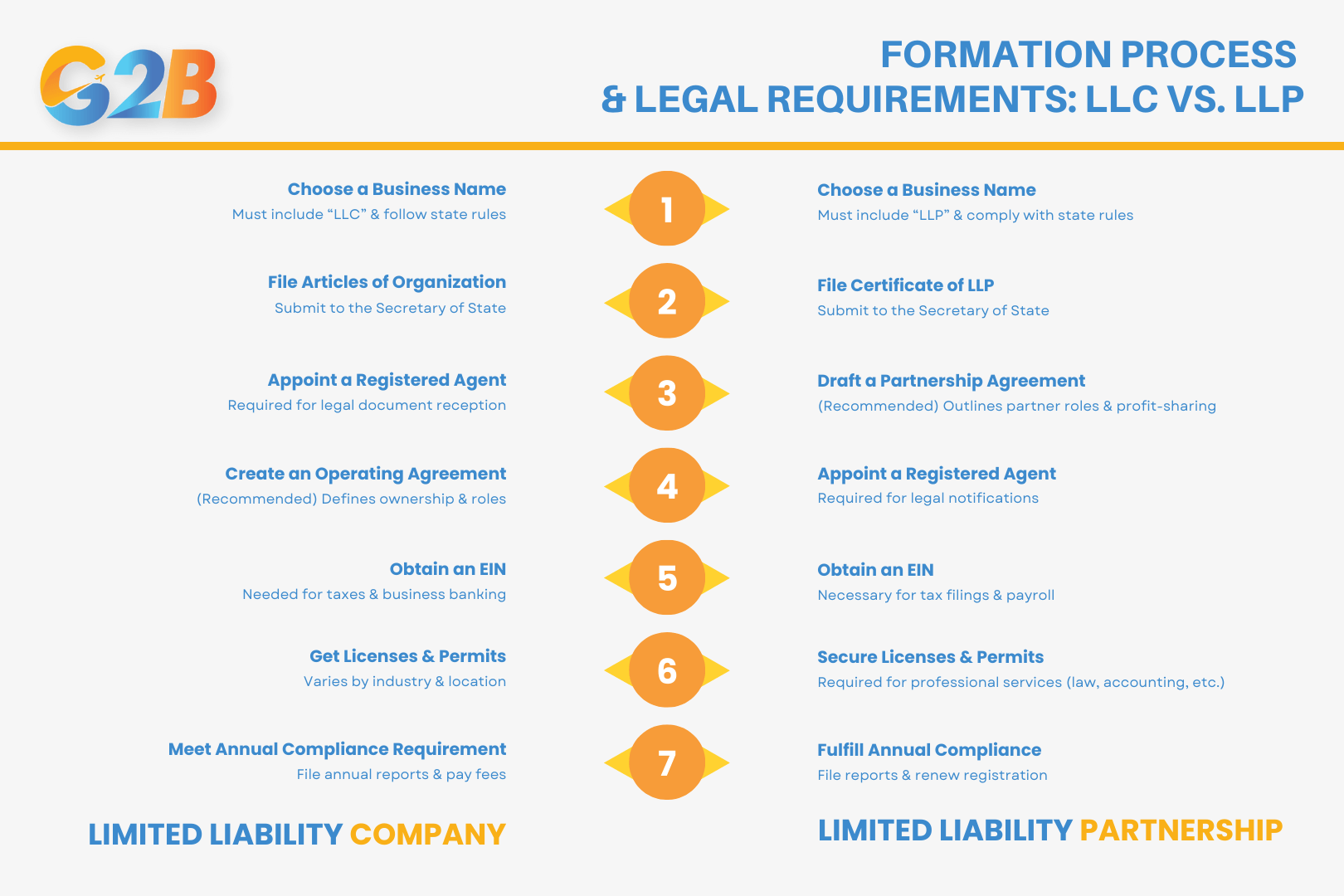

7 steps to register an LLC

The process of forming a limited liability company (LLC) involves several legal and administrative steps. While requirements vary by state, the core steps include:

- Choose a business name

- Must comply with state-specific naming rules (e.g., must include “LLC” or “Limited Liability Company” in the name)

- Cannot duplicate an existing registered entity in the state

- Some states restrict certain words (e.g., “bank” or “insurance” may require special approval)

- File articles of organization

- The Articles of Organization (also called a Certificate of Formation in some states) is the primary document to establish an LLC

- Filed with the Secretary of State or relevant state agency

- Requires basic information such as business name, registered agent, and business address

- Appoint a registered agent

- Every LLC must designate a registered agent to receive legal documents on behalf of the company

- The agent can be an individual (including a company member) or a professional service

- Must have a physical address in the state of formation

- Create an operating agreement (Recommended)

- Defines ownership structure, member roles, voting rights, and profit-sharing

- Helps prevent future disputes and provides clarity in business operations

- Obtain an employer identification number (EIN)

- Issued by the IRS for tax purposes

- Required for businesses with employees or multiple members

- Necessary to open a business bank account

- Comply with state and local licensing requirements

- Some LLCs need industry-specific licenses or local permits

- Sales tax permits may be necessary for businesses selling taxable goods/services

- Meet annual compliance requirements

- Most states require LLCs to file an annual report and pay renewal fees

- Failure to comply may lead to administrative dissolution

7 steps to register an LLP

A limited liability partnership (LLP) is typically chosen by professional service providers such as attorneys, accountants, and architects. The formation process varies but generally includes the following steps:

- Choose a business name

- Must follow state naming conventions, often requiring “LLP” or “Limited Liability Partnership” in the name

- Should not be deceptively similar to existing businesses

- Some states limit LLPs to professional firms (e.g., law or accounting firms)

- File a certificate of limited liability partnership

- Also called a Statement of Qualification in some states

- Must be filed with the Secretary of State

- Includes business name, principal office address, names of partners, and registered agent details

- Draft a partnership agreement

- Defines each partner's role, capital contributions, profit distribution, and decision-making processes

- Helps resolve potential disputes and ensures smooth business operations

- Not always legally required, but highly recommended

- Appoint a registered agent

- Required in most states for receiving legal documents

- Must have a physical presence in the state where the LLP is registered

- Obtain an employer identification number (EIN)

- Required for tax filings and payroll purposes

- Essential for partnerships with employees

- Secure necessary business licenses and permits

- Professional LLPs (law firms, medical practices) may require additional state licensing

- Local business permits may also be necessary, depending on the jurisdiction

- Fulfill annual reporting and compliance requirements

- Some states require annual LLP renewals and reports

- Non-compliance may result in penalties or loss of liability protection

Pros and cons of LLCs and LLPs

When choosing between a Limited Liability Company (LLC) and a Limited Liability Partnership (LLP), entrepreneurs and professionals must carefully evaluate the advantages and disadvantages of each structure.

Entrepreneurs should evaluate the advantages and disadvantages of LLC and LLP

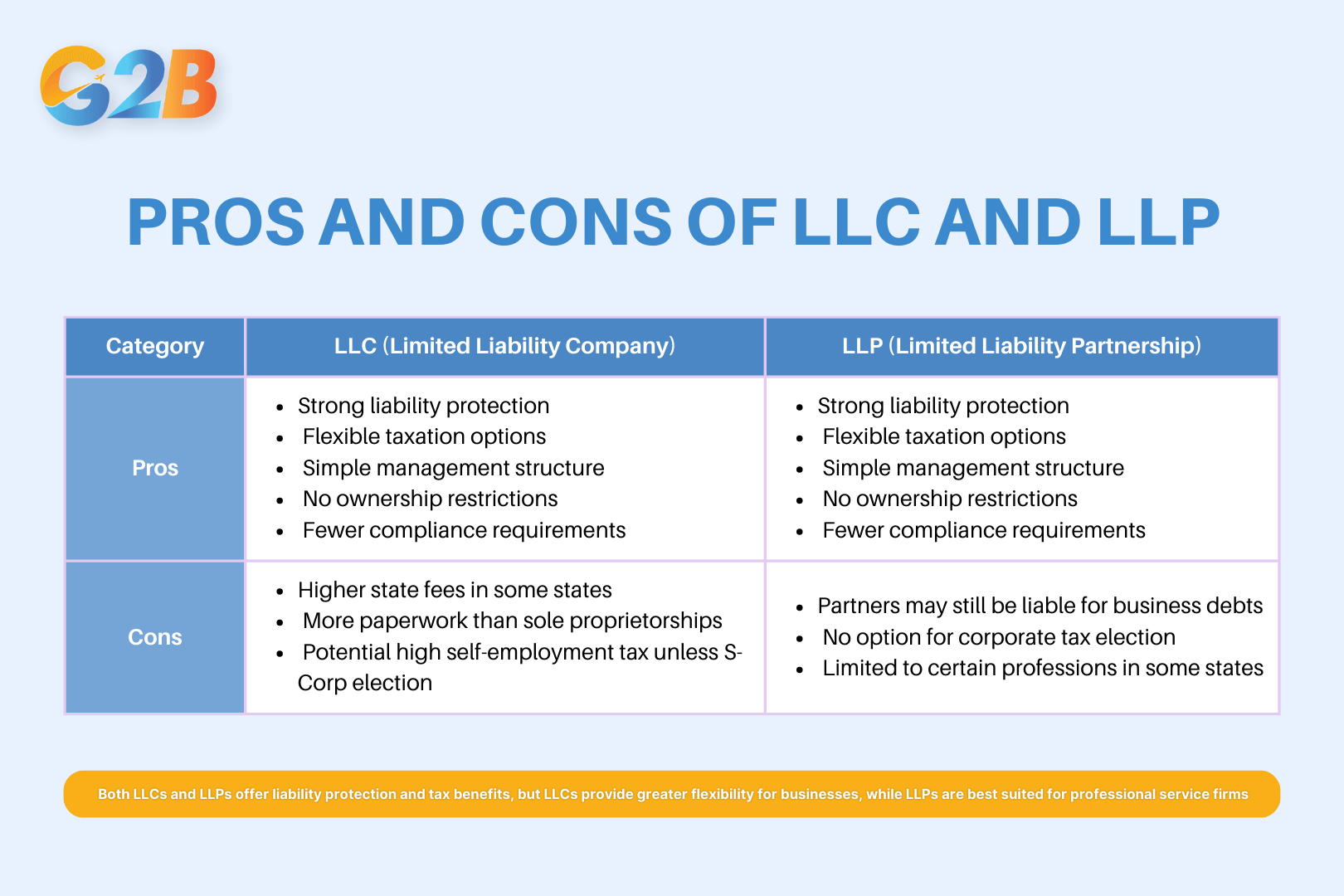

Key advantages of forming an LLC

An LLC provides strong liability protection, flexible taxation options, and a simplified management structure, making it a popular choice for small businesses and startups. With fewer compliance requirements and no ownership restrictions, LLCs offer entrepreneurs an adaptable and efficient way to structure their businesses.

1. Strong liability protection

An LLC offers limited liability, meaning that members' personal assets (such as homes, cars, and savings) are shielded from the company's debts and legal claims. This protection applies unless a member engages in fraud, personal guarantees, or wrongful acts.

2. Flexible taxation options

Unlike corporations, LLCs provide pass-through taxation, meaning profits and losses flow directly to members' personal tax returns, avoiding double taxation. However, LLCs also have the option to be taxed as:

- S-Corporation (reducing self-employment tax for eligible owners)

- C-Corporation (for businesses seeking investment and scalability)

3. Simple management and structure

LLCs allow for either member-managed or manager-managed structures, offering flexibility for small businesses and larger entities. There are fewer formalities compared to corporations, making them easier to operate.

4. No ownership restrictions

LLCs can have an unlimited number of members, including individuals, corporations, foreign investors, and even other LLCs. This makes them an attractive option for startups and joint ventures.

5. Fewer compliance requirements

Compared to corporations, LLCs do not need to hold annual meetings or file extensive records, reducing administrative burdens. This makes them a preferred choice for small businesses.

Key advantages of forming an LLP

LLPs offer liability protection for partners, pass-through taxation benefits, and equal management rights, making them ideal for professional service firms. Their industry credibility, along with flexible partner transitions, ensures a stable yet dynamic structure for growing businesses.

1. Liability protection for partners

In an LLP, each partner is protected from the negligence or misconduct of other partners, which is a crucial advantage for professional services firms like lawyers, accountants, and architects. However, partners remain personally liable for their own actions and business debts if state laws dictate.

2. Pass-through taxation benefits

LLPs are always taxed as pass-through entities, meaning that profits and losses are reported on each partner's individual tax return. This avoids double taxation and allows for greater tax efficiency.

3. Equal management rights

Unlike LLCs, where ownership and management can be separate, LLPs distribute management responsibilities equally among partners. This structure works well for firms where all partners play an active role in decision-making.

4. Professional credibility and industry acceptance

Many states require licensed professionals (lawyers, doctors, CPAs, architects) to operate as LLPs instead of LLCs due to ethical and regulatory constraints. This makes LLPs a trusted structure in professional industries.

5. Easier transition for new partners

LLPs offer more flexible partner admission and exit processes, making it easier for firms to bring in new talent without disrupting operations.

Potential drawbacks and risks of each structure

| Factor | LLC | LLP |

|---|---|---|

| Liability protection | Strong asset protection for all members | Protects partners from others' negligence but not always from business debts |

| Taxation | Flexible (can be taxed as sole proprietorship, partnership, S-Corp, or C-Corp) | Always pass-through taxation |

| Management structure | Member-managed or manager-managed | Partners have equal management rights |

| Industry suitability | Ideal for small businesses, startups, and real estate | Best for professional firms (lawyers, accountants, doctors) |

| State restrictions | Allowed in all states | Some states limit LLPs to professionals only |

| Compliance | Fewer formalities than in corporations | Requires annual filings in some states |

| Ownership structure | This can include individuals, corporations, and foreign investors | Restricted to partners only |

LLC drawbacks

- Some states impose higher fees and franchise taxes on LLCs compared to LLPs.

- LLCs require more paperwork than sole proprietorships to maintain compliance.

- Self-employment taxes on LLC members' income can be higher unless electing S-Corp taxation.

LLP drawbacks

- Partners are still personally liable for business debts in certain states.

- LLPs cannot elect different tax treatments like LLCs can.

- Some states restrict LLP formation to specific professions, limiting flexibility.

Both LLC vs. LLP offer liability protection and tax benefits, but their suitability depends on the business type. LLCs are ideal for entrepreneurs, startups, and multi-member businesses seeking tax flexibility and liability protection. LLPs are better suited for licensed professionals who need protection from partners' malpractice while maintaining a collaborative management structure.

Frequently asked questions (FAQs) - LLC vs. LLP

This section addresses some of the most common and critical questions about LLCs and LLPs, helping business owners and entrepreneurs make informed decisions.

What is the main difference between an LLC and an LLP?

The primary difference between a Limited Liability Company (LLC) and a Limited Liability Partnership (LLP) lies in their ownership structure, liability protection, and tax treatment:

| Feature | LLC | LLP |

|---|---|---|

| Ownership | Members (individuals, corporations, or other entities) | Partners (typically professionals in licensed industries) |

| Liability Protection | Full protection for all members' personal assets | Partners shielded from each other's negligence but may be liable for their actions |

| Taxation | Can be taxed as a pass-through entity, S corp, or C corp | Always taxed as a pass-through entity |

| Management | Flexible (member-managed or manager-managed) | Partners have equal control unless stated otherwise |

| Best For | Small businesses, startups, real estate investors | Professional service firms (law firms, accounting, medical practices) |

- LLCs offer greater flexibility in ownership and taxation, making them suitable for a wide range of businesses.

- LLPs are ideal for professional service firms where partners want liability protection but maintain operational control.

Can an LLP be converted into an LLC?

Yes, in most states, an LLP can be converted into an LLC, but the process depends on state laws and business circumstances. Here's how the conversion typically works:

- Check state regulations - Some states allow direct conversion by filing appropriate documents, while others require dissolution and reformation.

- Draft a new operating agreement - Since LLCs and LLPs have different management structures, new agreements must outline ownership, roles, and voting rights.

- File conversion documents - Depending on the state, you may need to file a Certificate of conversion or Articles of organization.

- Tax implications - If the LLP is a pass-through entity, transitioning to an LLC with an S-corp election may alter tax obligations.

- Notify creditors & update licenses - Inform relevant authorities, banks, and business partners about the change.

- While conversion is possible, business owners should assess whether an LLC structure aligns with their long-term goals, taxation needs, and liability protection requirements.

Which structure is better for tax savings?

The tax advantages of an LLC vs. an LLP depend on how the entity is taxed and the income distribution among owners. Here's a breakdown:

LLC taxation options:

- Default: Pass-through taxation (profits and losses reported on individual tax returns).

- Elect S-Corp status: Owners pay themselves a “reasonable salary”, and only remaining profits are subject to self-employment tax.

- Elect C-Corp status: Profits taxed at corporate rates; dividends taxed separately.

LLP taxation:

- Always a pass-through entity, meaning all partners pay self-employment taxes on their share of the income.

- No option to elect S-corp status, which could help reduce self-employment tax.

| Scenario | LLC tax benefit | LLP tax drawback |

|---|---|---|

| Owner-operator business | Can choose S-Corp taxation to reduce payroll tax | Must pay self-employment tax on full income |

| Passive income (Real estate, investments) | Can take advantage of C-corp tax structures | LLPs do not have a corporate taxation option |

| Professional services firm | No major tax advantage over LLP | Traditional pass-through taxation |

- LLCs generally offer more tax flexibility, especially for business owners seeking to reduce self-employment tax.

- LLPs are more straightforward but may result in higher tax liabilities for partners in professional firms.

Can a single person form an LLP?

No, an LLP requires at least two partners. By definition, an LLP is a partnership, meaning it must have multiple owners sharing responsibility. If a partner leaves or a sole owner wants to continue operations, alternative structures may be needed:

- Convert to an LLC - A single-member LLC offers liability protection and pass-through taxation.

- Operate as a sole proprietorship - There is no liability protection, but it is the simplest structure with minimal compliance requirements.

- Form a corporation - If seeking outside investment, a C-corporation or S-corporation may be a better choice.

LLPs are structured to encourage shared management and risk, making them unsuitable for single-person operations.

Do all states allow LLP formation?

No, LLP formation is not universally allowed in all U.S. states. Additionally, some states restrict LLPs to specific licensed professions (such as law firms, accounting firms, and medical practices).

State variations in LLP formation:

- Full recognition - Some states allow any business type to form an LLP.

- Limited to licensed professionals - States like California only allow LLPs for law firms, accountants, and architects.

- Higher compliance requirements - Certain states require LLPs to carry additional insurance or meet specific financial disclosure standards.

- No LLP option - A few states do not permit LLP formation, requiring businesses to register as LLCs or other entities.

These frequently asked questions highlight key considerations when choosing between an LLC and an LLP. LLCs provide greater flexibility in ownership and taxation, making them ideal for startups and diverse business types. LLPs, however, cater specifically to professionals, offering liability protection but with stricter state regulations. Business owners should assess legal, tax, and liability implications before deciding on the best entity structure.

Choosing between an LLC and an LLP is a crucial decision that depends on your business goals, liability concerns, and tax preferences. If you want to know more about company formation, contact G2B today for expert consultation tailored to your unique needs! With a commitment to reliability and precision, G2B offers professional business support services, guiding entrepreneurs through every stage of business registration with confidence.