Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Among the various company type options, the Limited Liability Company (LLC) stands out as a flexible and powerful entity, blending the most useful features of corporations and partnerships. However, misconceptions - such as assuming LLCs provide absolute liability protection or overlooking tax classification options - can lead to costly mistakes. Understanding the nuances of formation requirements, operating agreements, and management structures is crucial for maximising the benefits of an LLC.

Introduction to limited liability companies (LLCs)

Let’s explore what an LLC is, why it's popular, what its key features are, how it compares to other entities, and what global regulations govern its operation in this part.

What is a limited liability company (LLC)?

A Limited Liability Company (LLC) is a legally recognized business structure that provides personal liability protection to its owners, known as "members". Unlike sole proprietorships or partnerships, an LLC separates personal assets from business debts and legal obligations, ensuring that members’ property is safeguarded against lawsuits or financial liabilities of the company.

Key aspects of an LLC:

- Separate legal entity: The LLC exists independently from its owners, meaning it can enter contracts, own property, and be sued.

- Flexible ownership structure: Members can be individuals, corporations, other LLCs, or even foreign entities.

- Pass-through taxation: In most cases, LLCs are not taxed at the entity level; instead, profits and losses flow through to members’ personal tax returns.

- Operational flexibility: Unlike corporations, LLCs do not require a board of directors or rigid management structures.

Why are LLCs popular among entrepreneurs?

LLCs have gained widespread popularity due to their balance of legal protection, tax efficiency, and operational simplicity. For many business owners, forming an LLC offers a strategic advantage over other entity types. Key reasons for their appeal include:

- Liability protection: Personal assets (homes, cars, savings) are protected from business debts and lawsuits, as long as the corporate veil remains intact.

- Ease of formation: Unlike corporations, LLCs have fewer regulatory requirements and do not mandate shareholder meetings or complex reporting.

- Tax flexibility: LLCs can choose between default pass-through taxation, S corporation tax treatment, or C corporation taxation, depending on their financial goals.

- Minimal compliance burden: Unlike corporations, LLCs are not required to follow strict record-keeping, meeting, or reporting requirements.

- Enhanced credibility: Compared to sole proprietorships, an LLC signals legitimacy and professionalism to customers, partners, and investors.

Key features that define an LLC

LLCs are defined by several distinctive features that set them apart from other business entities:

| Feature | Description |

|---|---|

| Limited liability protection | Members are not personally liable for business debts, similar to corporate shareholders. |

| Pass-through taxation | Profits are reported on individual tax returns, avoiding double taxation. |

| Flexible management | Members can manage the LLC directly (member-managed) or appoint a manager (manager-managed). |

| Ownership flexibility | LLCs can have a single member or multiple members, and membership can include individuals, corporations, or other LLCs. |

| Less paperwork | Unlike corporations, LLCs are not required to hold annual meetings or maintain extensive records. |

| State-specific regulations | Each U.S. state has different LLC formation and compliance rules. |

How LLCs fit into the business landscape

To determine whether an LLC is the right choice, it is essential to compare it with other common business structures:

| Business entity | Liability protection | Taxation | Ownership & management | Compliance requirements |

|---|---|---|---|---|

| Sole proprietorship | No | Personal tax return | Single owner | Minimal |

| General partnership | No | Pass-through taxation | Two or more partners | Minimal |

| Limited partnership (LP) | Limited for some partners | Pass-through taxation | General and limited partners | Moderate |

| Limited liability partnership (LLP) | Yes (for partners) | Pass-through taxation | Two or more partners | Moderate |

| LLC | Yes | Pass-through (default) or corporate taxation | Flexible | Low to moderate |

| Corporation (C Corp) | Yes | Corporate tax & potential double taxation | Shareholders, directors, officers | High |

| S Corporation (S Corp) | Yes | Pass-through taxation (restrictions apply) | Limited to 100 U.S. shareholders | High |

Overview of global LLC regulations

While LLCs are most commonly associated with the U.S., similar structures exist in other countries, albeit with variations in rules and benefits. Here’s how LLC regulations compare across different regions:

- United States: LLCs are governed at the state level, with varying requirements for formation, annual fees, and tax treatment. Some states, like Wyoming and Delaware, offer stronger asset protection and business-friendly tax policies.

- United Kingdom: The equivalent of an LLC is a "Private Limited Company (Ltd)", which provides limited liability but requires more compliance and financial reporting.

- European Union: Many EU countries allow limited liability entities, such as the German "GmbH" or the French "SARL", which offer liability protection but have stricter capital requirements.

- Asia: Countries like Singapore have the "Private Limited Company (Pte Ltd)", offering significant tax benefits for startups. In contrast, China’s "Limited Liability Company" has stricter foreign ownership regulations.

- Australia & Canada: Both countries recognize LLC-like structures, such as the "Proprietary Limited Company (Pty Ltd)" in Australia and "Limited Partnerships" in Canada, with varying degrees of compliance and taxation rules.

16 Types of LLC: Key characteristics, pros & cons

Limited Liability Companies (LLCs) come in various forms, each designed to meet different business needs, legal structures, and tax requirements. The table below provides a comprehensive breakdown of 16 types of LLCs, highlighting their key characteristics, advantages, and potential drawbacks. This comparison will help business owners and investors determine the best LLC type for their specific goals:

| Type of LLC | Key characteristics | Pros | Cons |

|---|---|---|---|

| Single-member LLC (SMLLC) | Owned by one person, taxed as a disregarded entity. | Simple setup, pass-through taxation, liability protection. | IRS scrutiny, additional state taxes. |

| Multi-member LLC (MMLLC) | Owned by two or more members, taxed as a partnership. | Shared financial burden, flexible profit allocation. | Potential conflicts, requiring formal agreements. |

| Manager-managed LLC | Managed by designated managers instead of members. | Professional management, ideal for passive investors. | Members lose direct control, additional costs. |

| Member-managed LLC | All members share decision-making and operations. | Full control for members, no separate contracts. | Conflicts in decision-making, inefficient for large businesses. |

| Series LLC | Multiple sub-entities under one umbrella LLC. | Cost-effective, separate liability for each series. | Not recognized in all states, legal complexities. |

| Anonymous LLC | Owners' identities remain private. | Enhanced privacy, lawsuit protection. | Limited state availability, complex tax compliance. |

| Foreign LLC | Operates in a different state than its registration. | Business expansion, maintains original structure. | Multiple state regulations, extra fees. |

| Domestic LLC | Operates within its state of formation. | Simpler compliance, lower costs. | Limited to one state unless registered elsewhere. |

| Professional LLC (PLLC) | Restricted to licensed professionals (doctors, lawyers). | Legal protection, required in some professions. | No protection from malpractice claims, compliance burdens. |

| Restricted LLC | Distributions restricted for 10 years (e.g., Nevada). | Strong asset protection, good for estate planning. | Limited flexibility, not widely available. |

| Low-profit LLC (L3C) | Designed for social enterprises. | Grant eligibility, combining profit and nonprofit benefits. | Hard to attract investors, strict regulations. |

| Nonprofit LLC | Functions as a nonprofit with LLC flexibility. | Tax exemption potential, liability protection. | Compliance with nonprofit laws, profit limitations. |

| General partnership LLC | Hybrid between a partnership and an LLC. | Simple formation, liability protection. | Less protection than a standard LLC, needs agreements. |

| Limited partnership LLC | General and limited partners with different roles. | Liability protection for limited partners, attracts investors. | General partners remain personally liable. |

| Formal LLC | Strict adherence to state filing rules. | Strong legal protection, enhances credibility. | More paperwork, higher costs. |

| Hybrid LLC | Combines features of multiple LLC types. | Highly customizable, flexible taxation. | Complex setup, may require legal assistance. |

8 steps to apply for an LLC

Establishing a Limited Liability Company (LLC) is a structured process that requires careful attention to legal and regulatory requirements. Below is a comprehensive breakdown of the eight essential steps to successfully apply for an LLC.

Establishing a Limited Liability Company (LLC) requires 8 steps

Step 1: Choose a business name

Selecting an appropriate name is the first crucial step in forming an LLC. The business name should be unique, compliant with state regulations, and aligned with your brand identity.

Key considerations:

- State naming requirements: The LLC name must include “Limited Liability Company” or an accepted abbreviation like “LLC” or “L.L.C".

- Uniqueness: Conduct a business name search via the Secretary of State’s website to ensure the name is not already in use.

- Trademark search: Check the U.S. Patent and Trademark Office (USPTO) database to avoid potential trademark conflicts.

- Domain availability: If an online presence is essential, secure a matching domain name for your business.

Step 2: Select a registered agent

A registered agent is an individual or entity responsible for receiving legal and tax documents on behalf of your LLC.

Requirements:

- Must have a physical address in the state of LLC formation.

- Must be available during standard business hours.

- Can be an individual (owner or employee) or a professional registered agent service.

Step 3: File Articles of Organization

The Articles of Organization, sometimes referred to as a Certificate of Formation, is the official document filed with the state to legally create an LLC.

Filing process:

- Prepare the document: It typically includes:

- Business name and address

- Registered agent information

- Names of LLC members or managers

- Purpose of the LLC (general or specific)

- Submit to the secretary of state: Filing methods vary by state (online, mail, or in-person).

- Pay the filing fee: Costs range from $40 to $500, depending on the state.

Step 4: Create an operating agreement (Optional but recommended)

An operating agreement outlines the governance structure and operating procedures of the LLC.

Key elements to include:

- Ownership percentages and capital contributions

- Profit and loss distribution

- Voting rights and decision-making processes

- Management structure (member-managed vs. manager-managed)

- Dissolution procedures

Even if not legally required, an operating agreement helps prevent disputes among members and provides a legal framework for business operations.

Step 5: Get an EIN (Employer Identification Number)

An Employer Identification Number (EIN) is issued by the IRS for tax and hiring purposes.

How to obtain an EIN:

- Apply online: The fastest method via the IRS website.

- Apply by mail or fax: Complete Form SS-4 and submit it to the IRS.

- Free of charge: EINs are issued at no cost.

Why an EIN is necessary:

- Required for federal tax filings

- Necessary for hiring employees

- Needed to open a business bank account

Step 6: Register for state taxes & business licenses

Depending on the nature of your business, you may need to register for state taxes and obtain licenses or permits.

Common tax registrations:

- Sales tax permit: Required if selling taxable goods or services.

- Employment taxes: If hiring employees, register for payroll taxes.

- Franchise tax: Some states impose an annual LLC tax or fee.

Business licenses & permits:

- Industry-specific permits (e.g., health department license for food businesses)

- Local business licenses (county or city requirements)

Step 7: Open a business bank account

Separating personal and business finances is crucial for maintaining the LLC’s limited liability protection.

Required documents to open a business account:

- EIN confirmation letter from the IRS

- Articles of Organization

- Operating agreement (if applicable)

- Business licenses (if required by the bank)

A dedicated business account enhances financial organization, simplifies tax preparation, and strengthens liability protection.

Step 8: Maintain compliance

Ongoing compliance is essential to keep your LLC in good standing with state authorities.

Annual reporting requirements:

- Annual reports: Many states require LLCs to submit yearly reports with updated business information.

- Renew business licenses: Ensure all permits remain valid.

- Maintain proper record-keeping: Store meeting minutes, tax filings, and financial records securely.

Failing to comply with state requirements may result in penalties, dissolution of the LLC, or loss of liability protection. Applying for an LLC involves multiple steps, but following a structured approach ensures legal compliance and a strong foundation for business success.

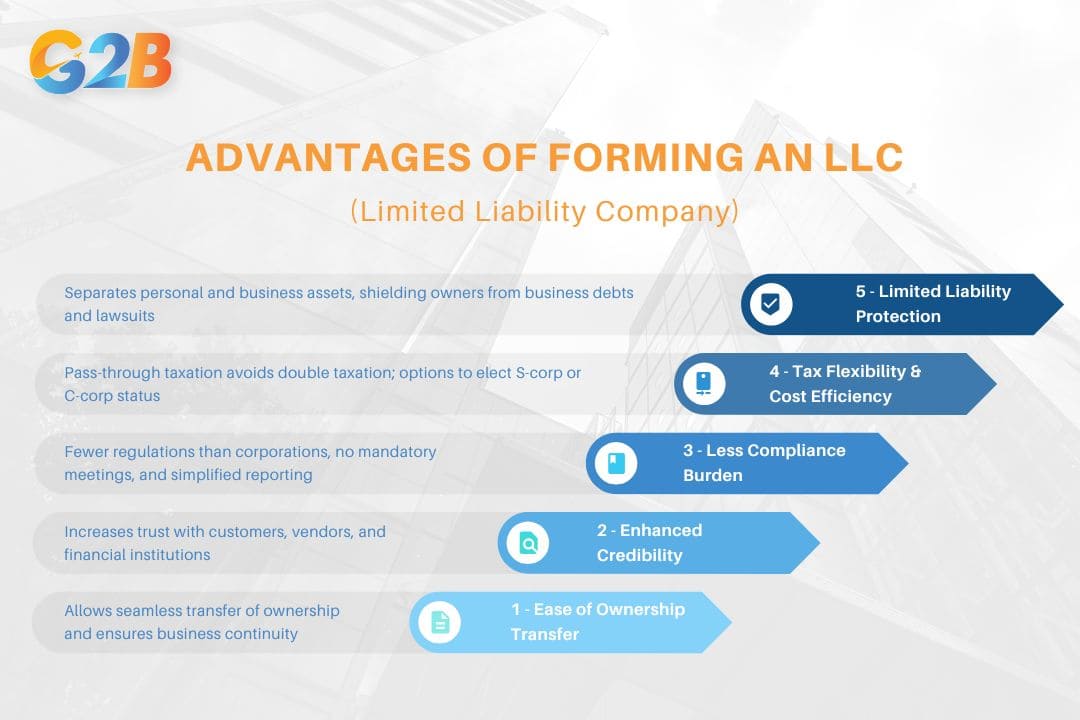

Advantages of forming an LLC

Entrepreneurs, small business owners, and investors often choose LLCs over corporations and sole proprietorships because of the numerous benefits they offer. Let’s explore the key advantages of forming an LLC in detail.

1. Limited liability protection: Separating personal and business assets

One of the most compelling reasons to establish an LLC is the limited liability protection it provides to its members. Unlike sole proprietorships or general partnerships, where personal assets are at risk in the event of business debts or lawsuits, an LLC creates a legal distinction between the business and its owners.

- Asset protection: Members’ assets - such as homes, vehicles, and personal savings - are generally safeguarded against business liabilities and lawsuits.

- Corporate veil: This protection exists as long as the business maintains proper financial and operational separations, such as keeping distinct bank accounts and adhering to regulatory requirements.

- Legal precedents: States with robust LLC laws, like Delaware and Wyoming, experience fewer instances of courts piercing the corporate veil.

2. Tax flexibility and cost efficiency

Unlike corporations that face double taxation, an LLC benefits from pass-through taxation, allowing profits to flow directly to members without being taxed at the entity level.

Tax options available for an LLC:

- Default classification: By default, a single-member LLC is treated as a sole proprietorship, while a multi-member LLC is classified as a partnership for tax purposes.

- Electing S-Corporation status: LLCs can opt for S-corp taxation, reducing self-employment taxes for owners who actively participate in business operations.

- C-Corporation option: If desired, an LLC can be taxed as a C-corp, which may be beneficial for businesses planning to reinvest profits or seek venture capital.

Additionally, LLCs avoid some of the costly compliance fees that corporations must pay, such as franchise taxes in certain states.

3. Less compliance burden compared to corporations

LLCs offer a more streamlined compliance framework, making them an attractive option for business owners who prefer minimal regulatory requirements. Unlike corporations, which must adhere to strict formalities such as annual meetings, board resolutions, and extensive record-keeping, LLCs enjoy greater operational flexibility.

- No mandatory annual meetings: Corporations must hold board meetings and document decisions, while LLCs are not required to do so.

- Simplified reporting: Many states only require LLCs to file an Annual Report and pay a nominal fee.

- Fewer restrictions on ownership: LLCs can have an unlimited number of members, unlike S-corporations, which are restricted to 100 shareholders.

This lower administrative burden allows entrepreneurs to focus on growing their business rather than navigating excessive paperwork.

4. Credibility and trust in business transactions

Forming an LLC enhances a business's professional image, making it more appealing to customers, suppliers, and financial institutions.

- Customer perception: Consumers tend to trust businesses that operate as LLCs rather than sole proprietorships, perceiving them as more stable and legitimate.

- Vendor and supplier agreements: Many suppliers prefer working with LLCs, as they demonstrate financial and legal commitment.

- Easier access to funding: Banks and investors often require businesses to be legally structured as an LLC or corporation before approving loans or investments.

5. Ease of ownership transfer and business continuity

Unlike sole proprietorships and partnerships, which may dissolve upon an owner's departure, an LLC offers greater stability and continuity.

- Transferability of ownership: While traditional partnerships often require dissolution upon a partner’s exit, LLCs can continue operating by simply transferring membership interests.

- Perpetual existence: Many states allow LLCs to exist indefinitely, ensuring the business survives beyond the involvement of its original founders.

- Estate planning benefits: LLC ownership can be passed down to heirs, making it a viable structure for long-term family businesses.

An LLC combines liability protection, tax benefits, and operational flexibility, making it an ideal choice for entrepreneurs and small businesses. With fewer compliance burdens than corporations and stronger legal protections than sole proprietorships, LLCs strike a balance between security and efficiency.

Limited Liability Company brings numerous benefits to entrepreneurs

Disadvantages of an LLC

Entrepreneurs and business owners should carefully consider these disadvantages before forming an LLC. Below are the key challenges associated with LLCs.

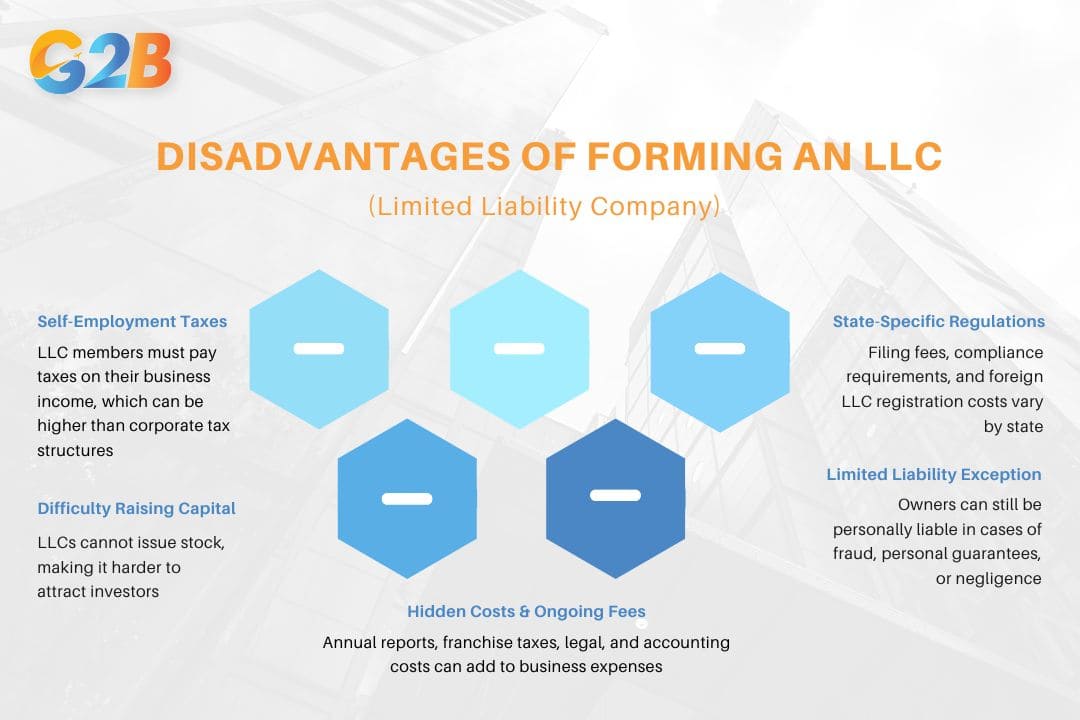

1. Self-employment taxes and financial obligations

One of the biggest financial drawbacks of an LLC is the self-employment tax. Unlike corporations that allow for various tax strategies, LLC owners (members) are subject to self-employment taxes, which include Social Security and Medicare taxes (15.3%) on their net earnings.

- Tax burden: Since LLCs are taxed as pass-through entities, profits are passed directly to members and reported on their individual tax returns. This means LLC members must pay self-employment taxes on the entire net income, whereas corporate shareholders (C-corporations) can structure their compensation to minimize self-employment taxes.

- Limited tax flexibility: While LLCs can elect to be taxed as S-corporations or C-corporations, doing so requires additional paperwork, accounting, and compliance obligations.

- State-level tax variations: Some states impose additional taxes on LLCs. For example, California charges an $800 annual franchise tax, while New York requires publication fees, adding to the operational costs.

Comparative table: Taxation burden for business entities

| Business structure | Self-employment taxes | Corporate taxation | Additional state fees |

|---|---|---|---|

| LLC (Default) | 15.3% on net income | No corporate tax | Varies by state |

| S-Corp Election | Only on salaries | No corporate tax | Additional paperwork |

| C-Corporation | No self-employment tax | 21% corporate tax | Franchise tax |

2. Difficulty in raising capital compared to corporations

Another major disadvantage of an LLC is its limited ability to raise capital compared to corporations. Investors and venture capitalists generally prefer corporate structures (C-corporations) due to the ability to issue shares and attract institutional funding.

- No stock issuance: LLCs cannot issue publicly traded stock, making it harder to attract large-scale investment.

- Investor preference: Many venture capitalists and angel investors prefer investing in corporations because they provide clearer exit strategies, such as public offerings or stock sales.

- Equity distribution challenges: Unlike corporations, where stock allocation is straightforward, LLCs must define profit-sharing and ownership stakes through an Operating Agreement, which can be legally complex and deter investors.

3. Differences in state laws and filing fees

LLCs are governed by state-specific regulations, which means the rules, costs, and filing requirements vary significantly depending on the state in which the LLC is formed.

- Formation and renewal fees: Some states impose high formation and annual renewal fees.

- State-specific compliance: Certain states have additional regulations, such as publication requirements in New York, which require LLCs to publish notices in local newspapers for several weeks, costing thousands of dollars.

- Foreign LLC registration costs: If an LLC conducts business in multiple states, it may need to register as a foreign LLC in each state, leading to additional compliance costs and administrative work.

4. Limited liability exceptions: When owners can still be sued

While LLCs offer limited liability protection, it is not absolute. There are specific situations where members can still be held personally liable:

- Piercing the corporate veil: If an LLC does not maintain proper separation between personal and business finances, courts may disregard liability protection. Common causes include:

- Commingling personal and business funds

- Fraudulent business activities

- Lack of proper record-keeping

- Personal guarantees on loans: Many lenders require personal guarantees from LLC members, meaning they are personally responsible for debts if the business defaults.

- Negligence and misconduct: If an LLC member engages in illegal or negligent behavior, personal liability may still apply, even if the business is structured as an LLC.

5. Hidden costs and ongoing compliance fees

Running an LLC is not always as inexpensive as it appears. In addition to state filing fees and taxes, there are ongoing compliance costs that may not be immediately apparent.

- Registered agent fees: Most states require an LLC to appoint a registered agent, which can cost between $50 to $300 per year.

- Annual reports and franchise taxes: Many states mandate annual reports, costing between $50 to $500 per year.

- Operating agreement and legal fees: Drafting a comprehensive Operating Agreement requires professional legal services, which can range from $500 to $5,000.

- Accounting and tax preparation: Since LLCs have unique taxation structures, hiring a tax professional for compliance and reporting adds to the expenses.

Note: While an LLC offers flexibility and liability protection, its tax implications, state-specific rules, limited fundraising potential, and ongoing costs can present challenges. Entrepreneurs should weigh these factors carefully before deciding on an LLC structure.

Entrepreneurs and business owners should consider 5 disadvantages before forming an LLC

Legal and tax implications of an LLC

Understanding the legal and tax implications of an LLC is crucial for any entrepreneur. Let’s investigate how LLCs shield business owners from personal liability while offering flexible taxation options that help optimize financial efficiency.

How LLCs provide liability protection for business owners

One of the primary reasons entrepreneurs choose a Limited Liability Company (LLC) over other business structures is liability protection. Unlike sole proprietorships and general partnerships, where business owners are personally responsible for debts and lawsuits, LLCs create a legal separation between the owner’s personal assets and business liabilities. This legal doctrine, known as the corporate veil, ensures that members of the LLC are not personally liable for the company’s financial obligations unless they engage in fraudulent or reckless behavior.

Key aspects of LLC liability protection:

- Personal asset safeguard: Creditors generally cannot pursue personal assets such as houses, cars, or bank accounts to satisfy business debts.

- Legal distinction: The LLC itself, as a separate legal entity, assumes responsibility for contracts, lawsuits, and financial obligations.

- Exceptions to protection: Personal guarantees, co-mingling personal and business finances, or fraudulent activities can result in "piercing the corporate veil", making owners personally liable.

- State variability: Some states offer stronger liability protection than others; for instance, Wyoming and Nevada are known for robust LLC protection laws.

Pass-through taxation: A major advantage of LLCs

LLCs benefit from a flexible tax structure, primarily through pass-through taxation, which prevents double taxation faced by traditional C-corporations.

How pass-through taxation works:

- No corporate tax: Unlike C-corporations, where profits are taxed at the corporate level and again when distributed to shareholders, LLCs avoid this double taxation.

- Income flow-through: Profits and losses "pass through" to the owners (members) and are reported on their individual tax returns.

- Flexibility in tax classification: LLCs can elect to be taxed as a sole proprietorship (single-member), a partnership (multi-member), or even as an S-corp or C-corp if it benefits the business.

Comparing LLC vs. other business structures:

| Business structure | Tax treatment | Double taxation? |

|---|---|---|

| LLC (default) | Pass-through | No |

| S Corporation | Pass-through | No |

| C Corporation | Corporate & Dividend tax | Yes |

| Sole proprietorship | Pass-through | No |

| Partnership | Pass-through | No |

Understanding self-employment tax for LLC owners

While pass-through taxation offers advantages, LLC members must consider self-employment tax, which can impact their overall tax liability.

Self-employment tax breakdown:

- The IRS classifies LLC members as self-employed, meaning they must pay Social Security and Medicare taxes (15.3%) on their share of net earnings.

- In contrast, corporate shareholders only pay FICA taxes (7.65%) on their wages, with their corporation covering the remaining 7.65%.

- LLCs electing S-corp taxation can reduce self-employment taxes by paying members a "reasonable salary" and distributing remaining profits as dividends, which are not subject to self-employment tax.

Compliance requirements: Annual filings, fees & state-specific regulations

Each state has specific regulations governing LLCs, requiring compliance with ongoing reporting, fees, and record-keeping to maintain good standing.

Common LLC compliance requirements:

- Annual reports & filing fees: Most states require LLCs to file an annual or biennial report, with fees ranging from $50 to $500, depending on the jurisdiction.

- Registered agent requirement: LLCs must appoint a registered agent within their state of formation to handle legal documents and government correspondence.

- State-specific operating agreements: While not mandatory in all states, having an Operating agreement ensures legal clarity in ownership and management responsibilities.

- Foreign qualification: If an LLC operates in multiple states, it must register as a foreign LLC in each additional state, incurring extra filing fees and compliance obligations.

- Federal Employer Identification Number (EIN): Required for hiring employees, opening business bank accounts, and filing taxes.

| Compliance requirement | Purpose | Cost Range |

|---|---|---|

| Annual/Biennial report | Maintain LLC status | $50 - $500 |

| Registered agent | Legal contact for LLC | Up to $300/year |

| EIN (IRS) | Tax & payroll processing | Free |

| Foreign qualification | Operate in multiple states | Varies |

| Operating agreement | Define ownership terms | Optional |

The legal and tax implications of an LLC are pivotal to structuring a business efficiently. While LLCs provide liability protection and tax flexibility, owners must carefully navigate self-employment tax obligations and state-specific compliance requirements.

LLC vs. Other business entities: A detailed comparison

This section provides a detailed comparison of LLCs with other common business entities to help entrepreneurs make informed decisions.

LLC vs. Sole proprietorship: Which one is better for small businesses?

A sole proprietorship is the simplest and most common business structure for individual entrepreneurs. However, it lacks the legal protections and flexibility offered by an LLC. Below is a comparison:

| Feature | LLC | Sole proprietorship |

|---|---|---|

| Liability protection | Owners have limited liability | Personal liability for debts and lawsuits |

| Tax treatment | Pass-through taxation, but can elect corporate tax status | Personal income tax on profits |

| Formation requirements | Requires state registration, fees, and an operating agreement | No formal registration required |

| Compliance & costs | Annual filings, fees vary by state | Minimal compliance costs |

| Business credibility | More credibility with banks and investors | Limited credibility |

Key takeaway: An LLC provides liability protection and increased business credibility, making it a better choice for entrepreneurs looking to scale. A sole proprietorship, however, is easier to set up and maintain.

LLC vs. Corporation (C corp & S corp): Key differences

Corporations offer strong legal protections and easier access to capital but come with more rigid regulations. Below is a comparison between LLCs and corporations:

| Feature | LLC | C Corporation (C Corp) | S Corporation (S Corp) |

|---|---|---|---|

| Liability protection | Yes, limited liability | Yes, limited liability | Yes, limited liability |

| Tax treatment | Pass-through by default | Double taxation (corporate & personal) | Pass-through taxation |

| Ownership restrictions | No restrictions | No restrictions | Limited to 100 shareholders, U.S. residents only |

| Profit distribution | Flexible, as per operating agreement | Fixed via dividends | Fixed via stock ownership |

| Compliance & costs | Moderate, annual filings required | High, strict regulations and corporate governance | High, similar to C Corp |

Key takeaway: Corporations are ideal for businesses seeking external funding and scalability, while LLCs provide flexibility with simpler tax benefits and fewer regulatory burdens.

LLC vs. Limited Partnership (LP) & Limited Liability Partnership (LLP)

Partnerships provide a collaborative business structure, but liability protection varies significantly between LPs, LLPs, and LLCs.

| Feature | LLC | Limited partnership (LP) | Limited liability partnership (LLP) |

|---|---|---|---|

| Liability protection | All members have limited liability | Only limited partners have liability protection | All partners have limited liability |

| Tax treatment | Pass-through taxation | Pass-through taxation | Pass-through taxation |

| Management structure | Flexible, member- or manager-managed | General partners manage, limited partners invest | All partners share management |

| Formation complexity | Moderate, requires state registration | Requires partnership agreement | Requires partnership agreement |

Key takeaway: LLPs and LPs are useful for professional services and investment-based ventures, while LLCs offer broader liability protection and management flexibility.

When to convert an LLC to a corporation

While an LLC provides flexibility and tax advantages, there are scenarios where converting to a corporation may be beneficial:

- Seeking venture capital or public funding: Investors and venture capitalists often prefer corporations due to stock-based compensation and shareholder rights.

- Scaling beyond a small business: Corporations are better suited for complex ownership structures and expansion.

- Reinvesting profits for growth: C corporations allow profits to be reinvested without pass-through taxation.

- Selling the business: Potential buyers often find corporations more attractive due to clear governance and stock transferability.

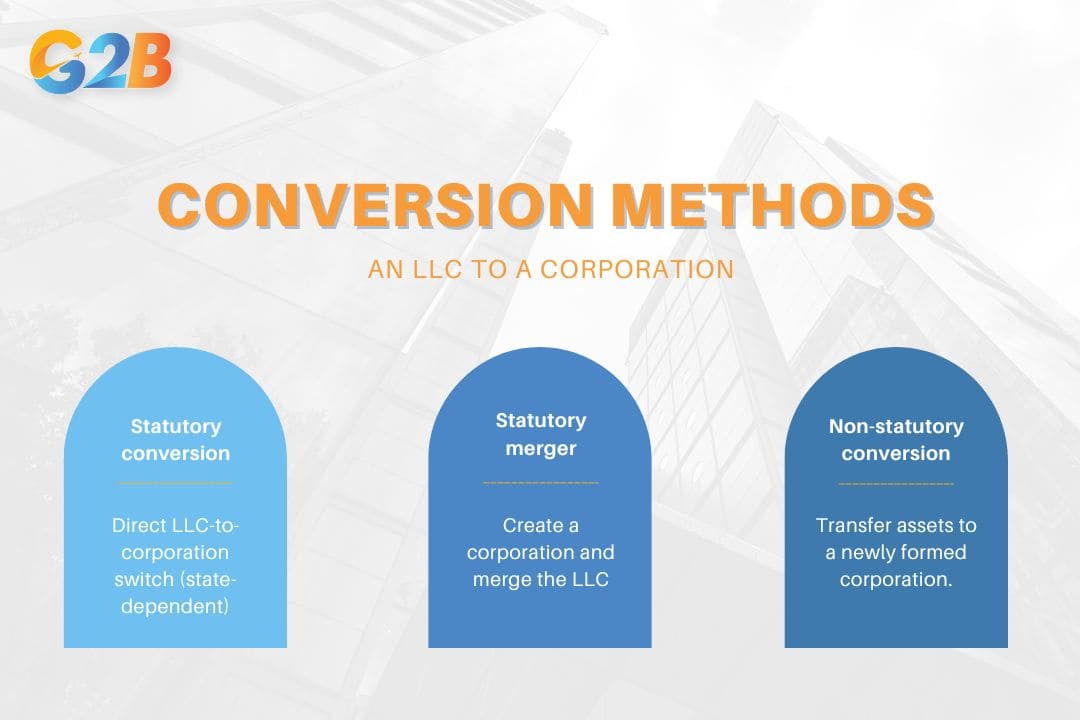

Conversion methods:

- Statutory conversion - Direct transformation from LLC to a corporation (available in certain states).

- Statutory merger - Form a corporation and merge the LLC into it.

- Non-statutory conversion - Form a corporation and transfer assets, contracts, and ownership.

Key takeaway: If your business is growing rapidly or requires outside investment, transitioning from an LLC to a corporation is a strategic move.

Converting an LLC to a corporation can be a strategic move for businesses looking to scale with 3 steps

Frequently asked questions (FAQs) about LLCs

Limited Liability Companies (LLCs) are a popular business structure, but entrepreneurs and business owners often have specific questions about their formation, management, and legal implications. Below, we answer some of the most common FAQs regarding LLCs.

What is the best state to form an LLC in the USA?

Choosing the right state for LLC formation depends on various factors such as tax benefits, filing fees, and business-friendly regulations. Some of the most preferred states for LLC formation include:

- Wyoming: Offers strong asset protection, low annual fees, and no state income tax.

- Delaware: Known for its well-established business laws and the Court of Chancery, which specializes in business disputes.

- Nevada: Provides no state income tax and strong privacy protections for business owners.

- Texas: A good option for businesses operating locally due to no state income tax and a large economic market.

For businesses that operate in a single state, forming an LLC in that state is often the best choice to avoid additional compliance and tax obligations.

If you are looking for a partner to accompany you throughout the process of forming an LLC in Delaware, G2B is a reputable partner with the enthusiastic support of our professional staff.

Can a non-US resident open an LLC in the US?

Yes, non-US residents can form an LLC in the United States. The process is similar to that for US citizens but involves some additional considerations:

- State selection: Popular states for non-resident LLC formation include Wyoming, Delaware, and Nevada due to their favorable tax and privacy laws.

- Registered agent requirement: A non-resident must appoint a registered agent in the state where the LLC is formed.

- Tax obligations: Foreign LLC owners are subject to US tax laws, and income generated in the US is taxable by the IRS.

- Banking challenges: Opening a US business bank account may require a visit to the US or the use of specialized services.

Despite these challenges, many international entrepreneurs choose the LLC structure for its limited liability protection and business flexibility.

How much does it cost to start and maintain an LLC?

The costs associated with forming and maintaining an LLC vary by state and include:

Formation costs:

- State filing fees: Range from $40 (Kentucky) to $500 (Massachusetts) depending on the state.

- Registered agent fees: Typically $50-$300 per year if hiring a professional agent.

- Operating agreement (optional but recommended): If drafted professionally, costs may range from $100-$500.

Ongoing maintenance costs:

- Annual report fees: Required in most states, up to $800 (California).

- State franchise taxes: Some states impose an annual franchise tax (e.g., Delaware: $300, California: $800 minimum).

- Business licenses & permits: Additional costs depend on the industry and location of operation.

Keeping up with state-specific compliance ensures the LLC remains in good standing and avoids penalties.

Do I need a lawyer to form an LLC?

Hiring a lawyer is not mandatory to form an LLC, but legal assistance can be beneficial in the following scenarios:

- Complex operating agreements: If the LLC has multiple members or special management structures.

- Regulatory compliance: Businesses in regulated industries (e.g., healthcare, finance) may require legal guidance.

- Multi-state operations: If an LLC operates in multiple states, legal advice ensures compliance with different state laws.

For straightforward LLC formations, many entrepreneurs use online services like LegalZoom, Incfile, or direct state registration portals.

Can an LLC own another LLC? (Parent-Child LLC Structures)

Yes, an LLC can own another LLC, forming a parent-child structure or a series LLC depending on the business needs:

- Traditional parent-child LLC structure: A holding company LLC owns multiple subsidiary LLCs, allowing for liability separation between different business units.

- Series LLC: Available in some states (e.g., Delaware, Texas, Illinois), this structure enables one LLC to have multiple "series" or compartments with separate liabilities.

- Tax considerations: Subsidiary LLCs may be taxed as pass-through entities or classified differently depending on IRS elections.

Establishing a limited liability company (LLC) is a strategic move for entrepreneurs seeking liability protection, tax flexibility, and operational simplicity. By understanding the advantages, legal considerations, and best practices, investors are now equipped to determine whether an LLC aligns with their business goals. For entrepreneurs launching a new venture or restructuring an existing one, leveraging these insights ensures a solid foundation for growth.