Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Unlike corporations or limited liability companies (LLCs), a sole proprietorship does not create a legal distinction between the business and its owner, resulting in unlimited personal liability. While sole proprietorships are easy to establish and manage, they also come with unique challenges. This guide provides a comprehensive overview of sole proprietorships, covering their definition, registration process, taxation, liability implications, and key advantages and disadvantages.

What is a Sole Proprietorship?

A sole proprietorship is the simplest and most common form of business ownership, where a single individual owns and operates the business. Unlike corporations or limited liability companies (LLCs), a sole proprietorship is not a separate legal entity from its owner.

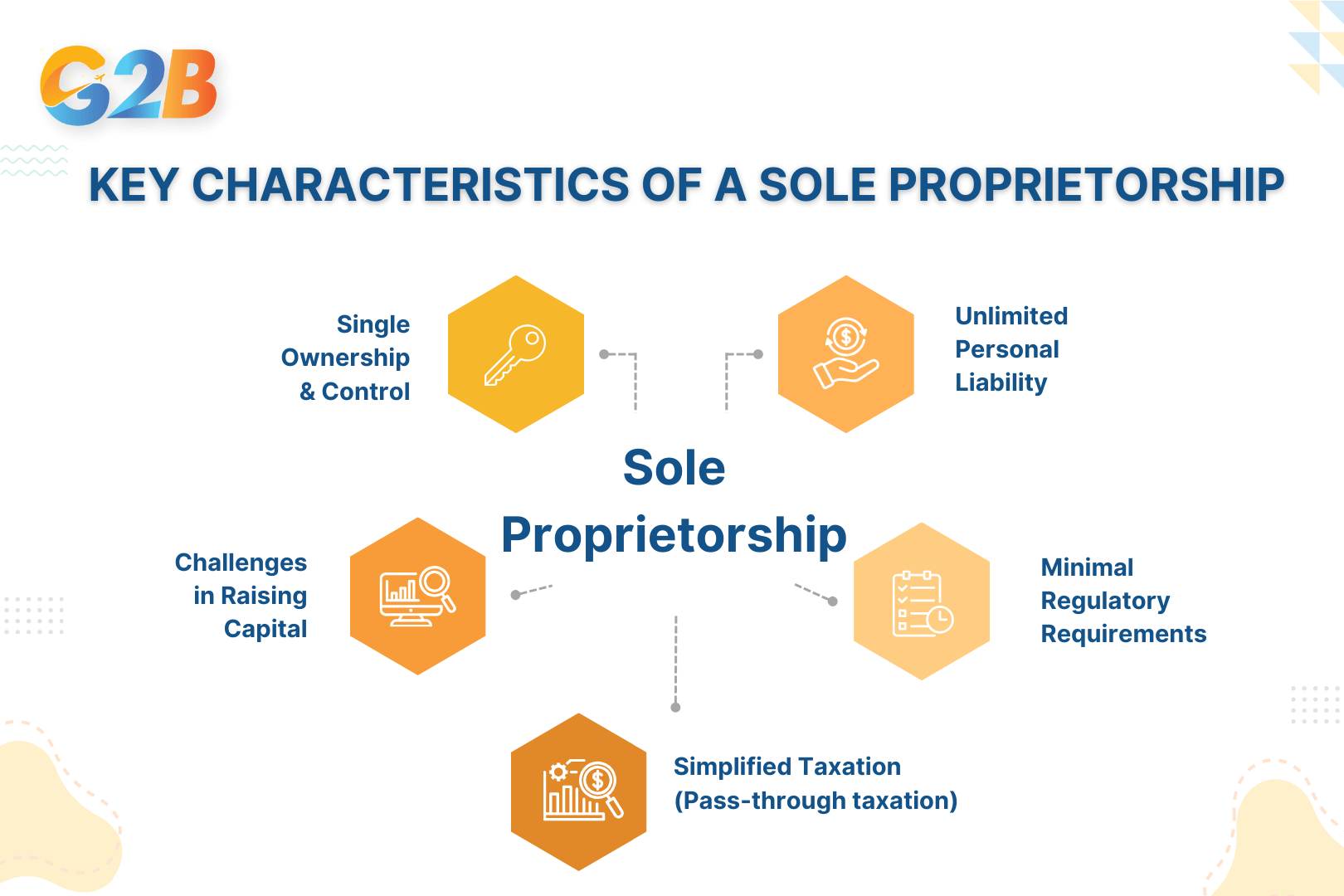

Key characteristics of a Sole Proprietorship

It is defined by single ownership and control, where one individual manages the business and retains full decision-making authority. While this structure offers simplicity and minimal regulatory requirements, it also comes with unlimited personal liability and challenges in securing external funding.

- Single ownership and control

- The business is owned and managed by one person.

- The owner has full decision-making authority without the need for board approvals or shareholder input.

- Unlimited personal liability

- The owner is personally responsible for all business debts and obligations.

- If the business incurs debt or legal issues, creditors can pursue the owner's personal assets (e.g., home, car, savings).

- Simplified taxation (pass-through taxation)

- Business profits and losses are reported on the owner's personal tax return (Form 1040, Schedule C in the U.S.).

- No separate corporate tax filings are required, avoiding double taxation.

- Minimal regulatory requirements

- No need for formal incorporation, bylaws, or board meetings.

- Depending on the industry and location, the owner may need a business license, permits, or a DBA registration.

- Challenges in raising capital

- Sole proprietors often rely on personal savings, loans, or investments from family and friends.

- Unlike corporations, they cannot issue stock or bring in equity investors easily.

A sole proprietorship has five key characteristics that entrepreneurs should consider

Sole Proprietorship vs. other business structures

| Feature | Sole Proprietorship | LLC | Corporation | Partnership |

|---|---|---|---|---|

| Ownership | One individual | One or more members | Shareholders | Two or more individuals |

| Liability | Unlimited personal liability | Limited liability | Limited liability | Varies (depends on type) |

| Taxation | Pass-through taxation | Pass-through or corporate | Corporate tax (double taxation possible) | Pass-through taxation |

| Complexity | Low (easy setup) | Moderate (state registration required) | High (requires more formalities) | Moderate (partnership agreement recommended) |

| Fundraising ability | Limited to personal funds | Easier than a sole proprietorship | Can issue stock to raise capital | Dependent on partners |

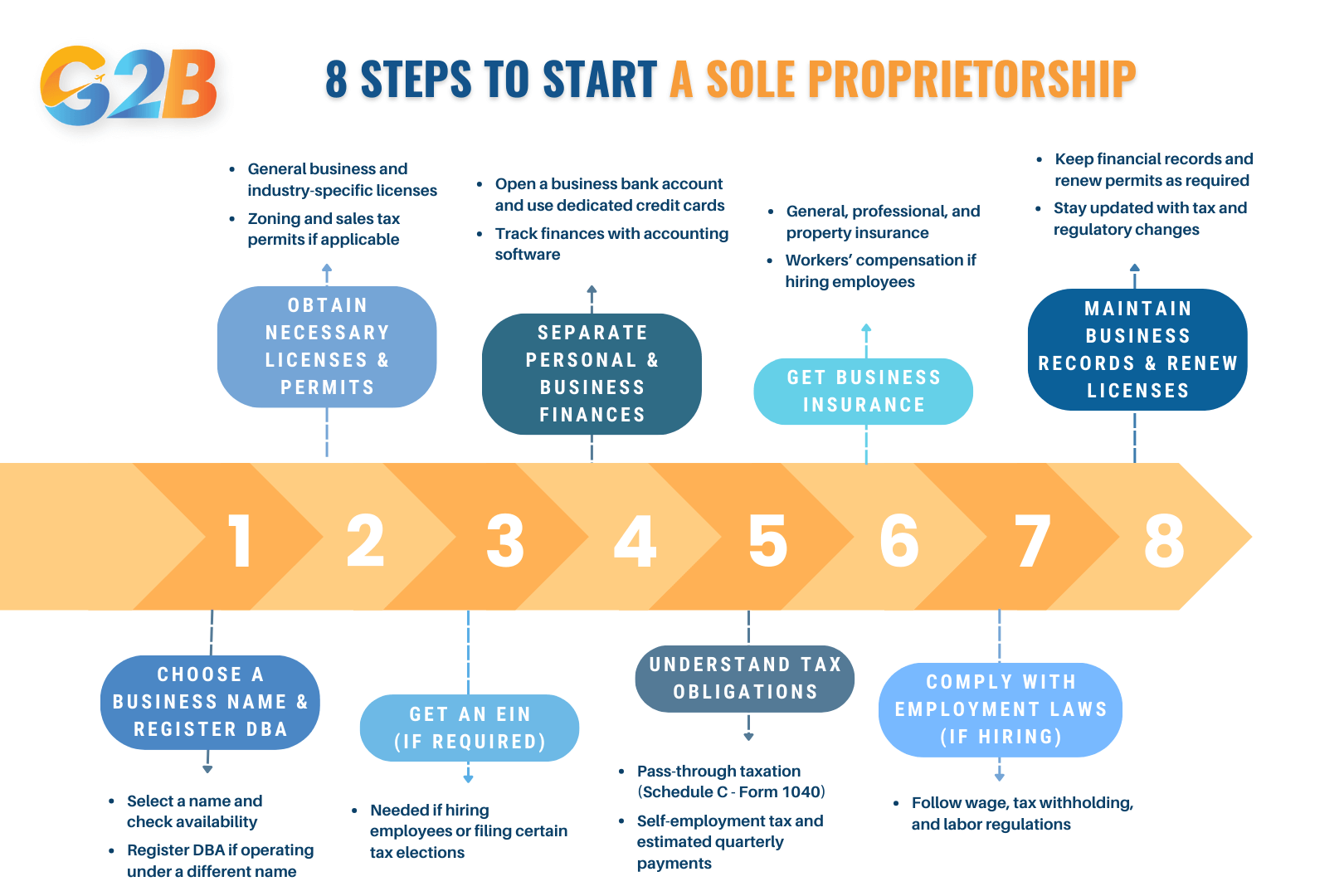

How to start a Sole Proprietorship? (8 steps)

With minimal paperwork and fewer regulatory requirements compared to corporations or LLCs, this business structure is one of the common choices. However, certain steps must be followed to ensure legal compliance and operational efficiency.

The process to start a Sole Proprietorship has 8 steps

1. Choose a business name and register a DBA (if necessary)

Selecting a business name is the first step in establishing your sole proprietorship. If you plan to operate under a name different from your legal name, you may need to register a Doing Business As (DBA) name. This process varies by state and locality but generally involves:

- Checking name availability through the state or county clerk’s office.

- Filing a DBA application and paying a registration fee.

- Publishing a DBA notice in a local newspaper (required in some states).

2. Obtain necessary business licenses and permits

Establishing a sole proprietorship must comply with local, state, and federal regulations. Depending on the nature of your business and its location, you may need:

- General business licenses (required in many cities and counties).

- Professional or industry-specific licenses (e.g., real estate, healthcare, food services).

- Zoning permits if operating from a physical location.

- Sales tax permits if selling taxable goods or services.

3. Obtain an employer identification number (EIN) (if required)

While sole proprietors can use their Social Security Number (SSN) for tax purposes, an Employer Identification Number (EIN) from the IRS is required in certain situations, such as:

- Hiring employees

- Operating as a partnership with another individual

- Filing for specific business tax elections

4. Separate personal and business finances

Although a sole proprietorship does not create a separate legal entity, it is crucial to distinguish personal and business finances to simplify accounting and tax reporting:

- Opening a business bank account to manage revenue and expenses.

- Using dedicated business credit cards to build credit history.

- Implementing accounting software such as QuickBooks or Wave for financial tracking.

5. Understand tax obligations

Sole proprietors are subject to pass-through taxation, meaning business profits are reported on the owner’s personal tax return using Schedule C (Form 1040):

- Self-employment tax covers Social Security and Medicare contributions.

- Estimated quarterly tax payments may be required to avoid IRS penalties.

- State and local tax obligations depend on your business location and industry.

6. Get business insurance to manage risks

Because sole proprietors have unlimited liability, they are personally responsible for business debts and lawsuits, hence to mitigate financial risks:

- General liability insurance to cover third-party claims.

- Professional liability insurance for service-based businesses.

- Property insurance if operating from a physical location.

- Workers' compensation insurance if hiring employees.

7. Comply with local employment laws (if hiring employees)

Although sole proprietors typically work alone, they can hire employees. This requires compliance with:

- State and federal employment regulations (e.g., wage laws, anti-discrimination policies).

- Payroll tax withholding (including Social Security, Medicare, and unemployment taxes).

- Workers’ compensation insurance (mandatory in most states for businesses with employees).

8. Maintain business records and renew licenses

Regular compliance with local and federal regulations ensures business continuity. Best practices include:

- Keeping financial and tax records.

- Renewing business licenses and permits as required by law.

- Staying updated with state and IRS tax changes affecting sole proprietors.

Starting a sole proprietorship is straightforward, but careful planning is necessary to ensure long-term success. By selecting the right business name, securing the necessary permits, managing taxes, and mitigating liability risks, entrepreneurs can build a strong foundation for their businesses.

Sole Proprietorship taxation: What business owners need to know?

Sole proprietorships operate under a unique tax structure that affects income reporting, self-employment taxes, and deductions. Let’s investigate what business owners need to know about taxation as a sole proprietor.

How do Sole Proprietors report income and expenses (Schedule C)?

Sole proprietors report business income and expenses using Schedule C (Form 1040). This form helps determine the business’s net profit or loss, which is then transferred to the owner’s personal tax return. Failing to accurately report income or claim legitimate deductions can lead to audits and penalties from the Internal Revenue Service (IRS).

- Income reporting: Sole proprietors must report all earnings from business activities, including cash payments, credit card transactions, and digital sales.

- Expense deductions: Eligible business expenses, such as rent, utilities, office supplies, and advertising costs, can be deducted to lower taxable income.

- Net profit calculation: The net profit (total income minus expenses) is subject to income tax and self-employment tax.

Self-employment tax and deductions

Unlike employees who have payroll taxes withheld by an employer, sole proprietors are responsible for self-employment tax, which covers Social Security and Medicare contributions. For example, in the US:

- Self-employment tax rate: Sole proprietors pay 15.3% of net earnings, consisting of:

- 12.4% for Social Security (on earnings up to $168,600 for 2024)

- 2.9% for Medicare (with no income limit)

- Self-employment tax deduction: 50% of self-employment tax is deductible when calculating taxable income, reducing overall tax liability.

Additionally, sole proprietors can take advantage of deductions such as:

- Home office deduction (if a portion of the home is exclusively used for business)

- Health insurance deduction (for self-employed individuals without employer-sponsored coverage)

- Retirement contributions (such as SEP IRAs or Solo 401(k) plans)

Estimated quarterly tax payments

Since taxes aren’t withheld from business income, sole proprietors must make estimated tax payments quarterly to the IRS to avoid penalties. Failing to make estimated tax payments can result in interest charges, making it crucial for sole proprietors to plan accordingly.

- Who needs to pay: If a sole proprietor expects to owe at least $1,000 in taxes for the year, they must make estimated payments.

- Due dates: Payments are due April 15, June 15, September 15, and January 15 of the following year (in the US).

- Calculation method: Estimated payments are based on prior-year tax liability or projected earnings for the current year. IRS Form 1040-ES helps calculate the correct amount.

Tax advantages and disadvantages compared to LLCs and corporations

When choosing a business structure, taxation is a key consideration. Sole proprietorships have pass-through taxation, meaning business income is taxed at the owner’s individual rate. However, they also come with limitations.

| Factor | Sole Proprietorship | LLC | Corporation |

|---|---|---|---|

| Taxation type | Pass-through (income taxed on personal return) | Pass-through (default) or corporate tax option | Corporate tax (C-corp) or pass-through (S-corp) |

| Self-employment tax | Required on all net earnings | Required (unless taxed as an S-Corp) | Only salaries are subject to payroll tax (C-Corp) |

| Deductions | Standard business deductions | More flexibility in tax planning | More options for tax savings and deferrals |

| Tax complexity | Simple filing with Schedule C | Moderate complexity | High complexity with corporate returns |

Key tax benefits of a Sole Proprietorship:

- Simplified tax filing (no need for separate business tax returns)

- Lower startup costs (no state registration fees beyond licenses and permits)

- Direct tax deductions for business expenses

Key tax drawbacks:

- Self-employment tax can be costly compared to an LLC taxed as an S-Corp

- No separation between personal and business income, making financial planning harder

- Limited access to tax-saving strategies that corporations can leverage

Sole proprietorship taxation is straightforward but requires careful planning to minimize tax liabilities. Business owners should maintain accurate financial records, understand deduction opportunities, and stay compliant with estimated tax payments. Consulting with a tax professional can help optimize tax strategies and ensure compliance with IRS regulations.

Unlimited liability in Sole Proprietorship: Risks and legal implications

One of the most significant challenges of running a sole proprietorship is the unlimited personal liability that comes with it - The business owner is personally responsible for all debts, lawsuits, and obligations of the business.

What unlimited liability means for business owners

Unlimited liability means that if the business incurs debts or legal claims, the owner’s personal assets - including bank accounts, real estate, and other valuables - can be seized to fulfil these obligations.

Key implications of unlimited liability:

- Personal asset exposure: Creditors can pursue an owner's personal savings, home, and car to cover business debts.

- Legal vulnerability: If the business faces a lawsuit (e.g., personal injury claims or contract disputes), the owner must personally handle all legal and financial consequences.

- Difficulty securing loans: Banks and investors may hesitate to finance sole proprietorships due to the lack of liability protection.

How do business debts impact personal assets?

Unlike corporate shareholders, who enjoy limited liability, sole proprietors must repay all business debts with personal resources if the business fails. This risk intensifies if the business:

- Takes on significant loans without sufficient revenue.

- Experiences economic downturns or unexpected losses.

- Faces legal action that results in high settlement costs.

For example, if a sole proprietor borrows $50,000 to expand operations but the business underperforms, the owner is still legally obligated to repay the loan - even if it means selling personal property to do so.

Common legal risks and how to mitigate them

Several legal risks accompany unlimited liability in a sole proprietorship. Understanding these risks and taking proactive steps can help reduce exposure:

| Legal risk | Potential consequences | Mitigation strategies |

|---|---|---|

| Business lawsuits | Personal liability for damages and legal fees | Get liability insurance, draft strong contracts |

| Debt default | Risk of bankruptcy and asset seizure | Limit borrowing, separate finances |

| Employee-related claims | Liability for workplace injuries or disputes | Follow labor laws, maintain proper documentation |

| Contract breaches | Legal disputes with vendors or clients | Use clear agreements, consult legal experts |

Business insurance options for sole proprietors

While sole proprietors cannot eliminate personal liability, business insurance can serve as a critical layer of protection. Key types of insurance include:

- General liability insurance: Covers third-party claims of bodily injury, property damage, and legal fees.

- Professional liability insurance: Protects against claims of negligence or inadequate service, essential for consultants and service-based businesses.

- Business interruption insurance: Helps cover lost income due to unexpected closures or disasters.

- Commercial property insurance: Protects business assets, including equipment and inventory, from damage or theft.

Unlimited liability is a fundamental risk of operating as a sole proprietorship. While the simplicity and tax advantages of this business structure are appealing, business owners must carefully consider the financial and legal risks involved. By implementing risk mitigation strategies - such as obtaining insurance, keeping personal and business finances separate, and considering alternative business structures like an LLC - sole proprietors can protect their assets while maintaining business flexibility.

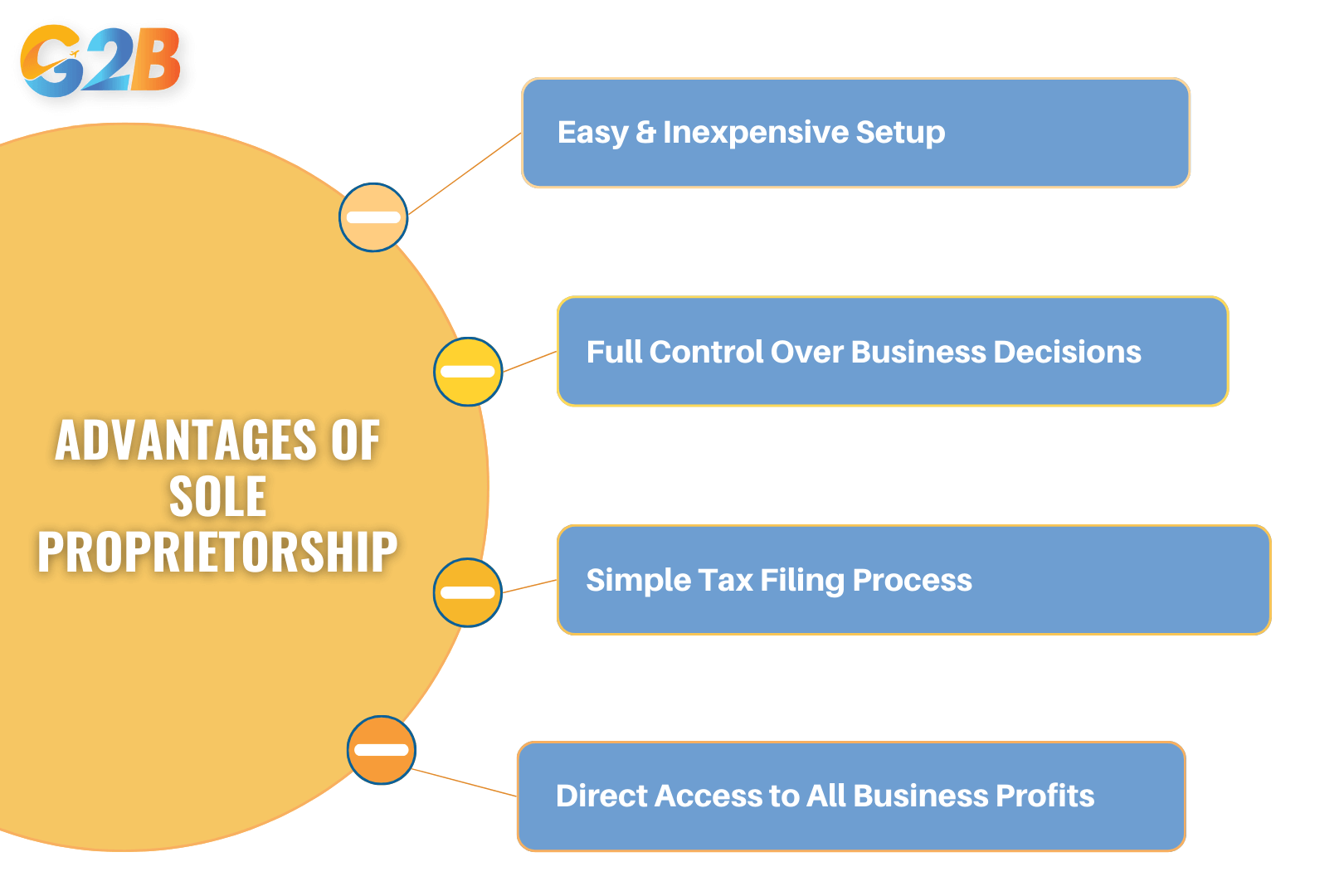

Advantages of Sole Proprietorship

Sole proprietorships remain the most common business structure in the United States. Let’s delve into the key advantages of operating as a sole proprietor, including ease of setup, full control over business decisions, and direct access to profits.

There are 4 key advantages of operating as a sole proprietor

Easy and inexpensive setup

One of the primary advantages of a sole proprietorship is its minimal setup requirements. Unlike corporations or limited liability companies (LLCs), which require formal registration, legal documentation, and compliance with ongoing regulatory obligations, sole proprietorships can be established quickly and with little to no cost.

- No formal registration: In most jurisdictions, a sole proprietorship does not require formal registration with the state. Entrepreneurs can operate under their legal name without additional paperwork.

- Low startup costs: Business formation expenses, such as incorporation fees or legal consulting, are significantly lower compared to other structures.

- Simple licensing process: While some businesses may require permits or licenses depending on industry regulations, the process is generally straightforward.

Full control over business decisions

As the sole owner, a proprietor has complete authority over all aspects of their business operations. This level of autonomy allows for quick decision-making, agility in responding to market trends, and greater creative and strategic freedom.

- No need for board approvals: Unlike corporations that require decisions to be approved by a board of directors or shareholders, sole proprietors can make immediate changes to their business models, pricing, or service offerings.

- Direct oversight of operations: Owners can maintain a hands-on approach to daily operations, ensuring quality control and customer satisfaction.

- Greater flexibility: Whether it’s adjusting business hours, pivoting strategies, or entering new markets, sole proprietors have full discretion to adapt as needed.

Simple tax filing process

Sole proprietorships benefit from pass-through taxation, which simplifies tax reporting and reduces administrative burdens. Unlike corporations that face double taxation (where income is taxed at both corporate and individual levels), sole proprietors report business earnings directly on their personal tax returns.

- No corporate tax: Business profits are taxed only once as personal income, avoiding the complexities of corporate tax filings.

- Use of Schedule C (Form 1040): Sole proprietors file a Schedule C along with their personal tax return, consolidating reporting and reducing compliance efforts.

- Eligible deductions: Business-related expenses, such as office supplies, travel, and home office costs, can be deducted to lower taxable income.

Direct access to all business profits

Unlike partnerships or corporations where profits are distributed among multiple stakeholders, sole proprietors retain all earnings generated by the business. This direct access to revenue allows for complete financial control and reinvestment opportunities.

- No profit-sharing requirements: Sole proprietors are not obligated to distribute earnings among partners or shareholders, enabling them to reinvest profits as they see fit.

- Unrestricted salary decisions: The owner determines their own compensation without restrictions from corporate structures or salary caps.

- Efficient cash flow management: Since there is no separation between the owner and the business entity, managing finances is more straightforward.

The advantages of a sole proprietorship make it an appealing choice for entrepreneurs seeking a simple, low-cost, and flexible business structure. From easy setup and full control over decision-making to streamlined taxation and direct access to earnings, this model offers significant benefits for independent business owners.

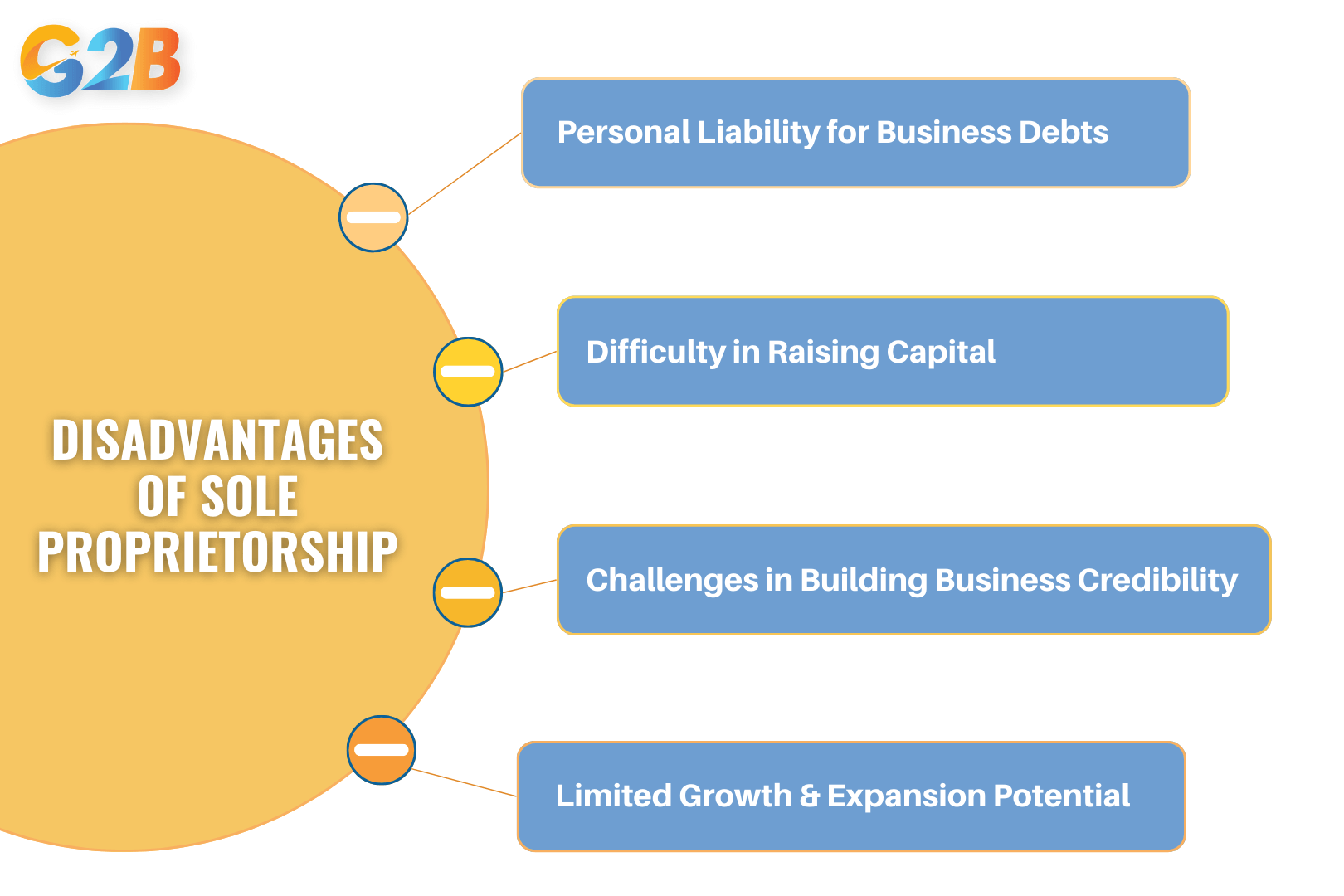

Disadvantages of Sole Proprietorship

While a sole proprietorship is one of the simplest business structures, it comes with significant disadvantages that can impact long-term sustainability and growth. Entrepreneurs must carefully assess these drawbacks before choosing this structure.

4 key disadvantages of operating as a sole proprietor

Personal liability for business debts

One of the disadvantages of a sole proprietorship is unlimited personal liability. The owner is personally responsible for all debts, legal actions, and financial obligations of the business.

- If the business incurs debt, the owner's personal assets, including savings accounts, real estate, and vehicles, can be seized to cover the liabilities.

- Lawsuits against the business directly affect the owner, exposing them to potential financial ruin.

- In cases of bankruptcy, the proprietor does not benefit from the legal protections that corporations or LLCs enjoy.

Difficulty in raising capital

Sole proprietors often struggle to secure funding due to the business’s lack of formal structure and perceived higher risk. Investors and banks tend to favour businesses with distinct legal identities, such as corporations and LLCs, because these structures provide greater financial stability and risk mitigation.

- Limited access to business loans: Many financial institutions are hesitant to lend to sole proprietors since their businesses lack separation from personal finances.

- No stock or equity options: Unlike corporations, sole proprietorships cannot issue shares to attract investors.

- Reliance on personal funds: Most sole proprietors finance their businesses through personal savings, credit cards, or small personal loans, which can limit expansion opportunities.

Challenges in building business credibility

Business credibility plays a vital role in attracting customers, securing partnerships, and obtaining favourable financial terms. However, sole proprietorships often face credibility issues due to their informal structure and lack of separation from the owner.

- Trust and reputation: Potential clients or partners may perceive sole proprietorships as less stable or professional compared to incorporated businesses.

- Supplier and vendor relationships: Many suppliers offer better terms and credit lines to registered entities like LLCs or corporations.

- Difficulty in hiring employees: Recruiting skilled employees can be challenging, as many professionals prefer to work for more established and legally structured businesses.

Limited growth and expansion potential

A study by the National Federation of Independent Business (NFIB) found that only 20% of sole proprietorships transition into larger entities. Sole proprietorships often struggle with scalability due to their structural limitations. Growth requires significant capital, resources, and strategic partnerships - areas where sole proprietors face significant obstacles.

- Business continuity risk: Since the business is tied directly to the owner, it often ceases to exist if the proprietor retires, becomes incapacitated, or passes away.

- Operational limitations: Expanding operations typically requires hiring employees, securing larger premises, or entering new markets, which can be difficult without sufficient funding or legal backing.

- Tax inefficiencies: Unlike corporations that can benefit from reinvesting profits at lower tax rates, sole proprietors are subject to self-employment taxes, which can be a financial burden as the business grows.

While sole proprietorships offer simplicity and control, they come with inherent disadvantages, including unlimited personal liability, difficulty in securing funding, challenges in building credibility, and limited growth potential. Entrepreneurs should weigh these drawbacks carefully.

Sole Proprietorship vs. LLC: Which is better for your business?

Both options have their advantages and drawbacks, depending on factors such as liability, taxation, and business goals. Below is a detailed comparison to help determine which is better for your business.

1. Liability protection

- Sole Proprietorship: The owner and the business are legally the same entity. This means the owner is personally liable for any debts or legal actions against the business.

- LLC: Provides limited liability protection, meaning personal assets (such as your house or car) are protected from business debts and lawsuits.

Key point: If limiting personal liability is a priority, an LLC is the better choice.

2. Setup and maintenance costs

- Sole Proprietorship: Minimal setup costs and fewer ongoing requirements.

- LLC: Requires filing formation documents and paying state registration fees, along with annual compliance costs.

Key point: If you’re looking for the simplest and most cost-effective option, a sole proprietorship is better.

3. Taxation

- Sole Proprietorship: Income is reported on the owner’s personal tax return, and profits are subject to self-employment taxes (Social Security and Medicare).

- LLC: By default, an LLC is taxed similarly to a sole proprietorship (pass-through taxation). However, an LLC can choose to be taxed as an S-corporation or C-corporation, potentially offering tax savings.

Key point: If you want more tax flexibility and potential savings, an LLC may be more beneficial.

4. Administrative requirements

- Sole Proprietorship: Minimal paperwork and no need for separate tax filings.

- LLC: Requires an operating agreement, state filings, and potentially more record-keeping.

Key point: If you prefer less administrative work, a sole proprietorship is the easier choice.

5. Business credibility and growth potential

- Sole Proprietorship: Easier to set up but may lack credibility when dealing with clients, investors, or financial institutions.

- LLC: Generally perceived as a more legitimate business structure, making it easier to attract investors and secure business loans.

Key point: If you plan to expand or seek external funding, an LLC is a better choice.

If you are still hesitant about other types of businesses, you can learn more about Sole Proprietorship vs LLC.

Sole Proprietorship vs. Corporation: Pros and cons

Sole proprietorship and corporation have their advantages and disadvantages in terms of liability, taxation, ease of formation, and business growth potential. Below is a detailed comparison to help entrepreneurs make an informed decision.

1. Liability protection

- Sole Proprietorship: The business owner and the business are legally the same entity. This means the owner has unlimited personal liability for debts and lawsuits, putting personal assets at risk.

- Corporation: A corporation is a separate legal entity, providing limited liability protection. Shareholders are not personally responsible for business debts or legal actions against the company.

Key point: A corporation offers better asset protection, making it preferable for businesses exposed to financial risk.

2. Taxation

- Sole Proprietorship: Business income is reported on the owner’s personal tax return (Form 1040, Schedule C). The owner pays self-employment taxes (Social Security & Medicare) on all business income.

- Corporation:

- C Corporation: Subject to double taxation - the company pays corporate tax, and shareholders pay taxes on dividends.

- S Corporation: Pass-through taxation avoids double taxation; profits and losses pass to shareholders’ personal tax returns.

Key point: Sole proprietorships have simpler tax filing but may result in higher self-employment taxes. S corporations offer a tax advantage for some businesses.

3. Business ownership & control

- Sole Proprietorship: The owner has full control over decision-making but has limited growth potential.

- Corporation: Ownership is divided into shares. While shareholders may have voting rights, decision-making is usually handled by a board of directors and executives.

Key point: Corporations allow for scalable ownership structures, making them suitable for larger ventures.

4. Ease of formation & maintenance

- Sole Proprietorship: Easiest to establish with minimal paperwork and costs. Requires only local business permits and tax registrations.

- Corporation: Requires state-level registration, Articles of Incorporation, annual reports, and compliance with corporate formalities.

Key point: Sole proprietorships are best for solo entrepreneurs seeking a low-cost, simple structure.

5. Funding & business growth

- Sole Proprietorship: Limited to personal savings, bank loans, or private investors. Cannot issue stock.

- Corporation: Can raise capital through stock issuance, making it attractive to venture capitalists and investors.

Key point: Corporations have a stronger ability to attract investment and scale.

6. Business continuity & exit strategy

- Sole Proprietorship: The business ends upon the owner’s death or decision to close.

- Corporation: Has perpetual existence, meaning it can continue regardless of ownership changes.

Key point: A corporation provides better long-term stability and transferability.

Link về bài so sánh tương ứng (SEO làm)

Transitioning from a Sole Proprietorship to another business structure

Below are key steps and considerations for making the transition from a sole proprietorship to another business structure.

1. Evaluating the need for a new business structure

Before transitioning, business owners should assess why they need a new structure. Common reasons include:

- Liability protection: Sole proprietors have unlimited personal liability, while structures such as LLCs and corporations offer limited liability.

- Tax benefits: Depending on the structure, tax treatment may be more favourable.

- Business growth: Corporations and partnerships can attract investors more easily.

- Credibility and professionalism: A formal business structure can improve trust among clients and partners.

2. Choosing the right business structure

The most common structures business owners transition to include:

- Limited Liability Company (LLC): Provides liability protection while maintaining pass-through taxation.

- S Corporation: Offers potential tax advantages and allows for multiple shareholders.

- C Corporation: Suitable for larger businesses looking to raise capital through stock issuance.

- Partnerships (General or limited): Ideal for businesses with multiple owners who want to share responsibilities and profits.

3. Registering the new business entity

Once the business owner selects the appropriate structure, they must complete the following steps:

- Choose a business name: Ensure the new name complies with state regulations and is available for registration.

- File formation documents:

- LLC: Articles of Organization

- Corporation: Articles of Incorporation

- Partnership: Partnership agreement (if applicable)

- Obtain an Employer Identification Number (EIN): Required for tax purposes and bank accounts.

- Update licenses and permits: Any existing business licenses may need to be transferred or reissued.

- Open a new business bank account: Helps separate personal and business finances.

4. Tax and financial considerations

The transition affects tax obligations, so business owners should:

- Notify the IRS and state tax agencies about the change.

- Understand new tax filing requirements (e.g., LLCs may file as sole proprietors, partnerships, or corporations).

- Update payroll systems and employee tax documents if applicable.

- Consult a tax professional for guidance on deductions and tax benefits.

5. Transferring assets, contracts, and agreements

A smooth transition requires transferring:

- Business assets and intellectual property to the new entity.

- Contracts and client agreements, ensuring they reflect the new structure.

- Leases and vendor agreements, which may need renegotiation.

- Employee records and benefits plans if the business has staff.

6. Notifying stakeholders

Inform all relevant parties about the transition, including:

- Clients and customers

- Vendors and suppliers

- Employees and contractors

- Financial institutions and lenders

7. Updating business records and compliance

Maintain compliance by:

- Filing annual reports and meeting state requirements.

- Keeping accurate financial and tax records.

- Adhering to ongoing legal obligations based on the new structure.

Understanding the key characteristics of a sole proprietorship is essential in determining whether it aligns with long-term business objectives. This structure offers simplicity, full managerial control, and direct tax advantages, making it an attractive option for many entrepreneurs. For those seeking expert guidance on company formation in Delaware, US, G2B provides expert consultation along with other professional business support services. We empower entrepreneurs through every stage of business registration with dedication.