Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Growth company is defined as an organization that generates substantial positive cash flow or earnings that increase at significantly faster rates than the overall economy or the average rate of its specific industry. These entities are characterized by their aggressive prioritization of capital appreciation over immediate income distribution, choosing to plow profits back into the business rather than issuing dividends.

What is a growth company?

A growth company is distinct from a "Value Company" or a "Income Stock" based on its capital allocation strategy and market expectations. While a mature value company typically focuses on maintaining market share and returning capital to shareholders, a growth company focuses on capturing market share through innovation, disruption, and scaling.

The primary driver for a growth company is revenue growth, not just revenue expansion. Investors in these equities are willing to forgo current dividends in exchange for the potential of significant future capital appreciation. This expectation creates a unique valuation environment where the current stock price often reflects cash flows expected to occur years, sometimes decades, into the future.

The core trade-off: Dividends vs. Reinvestment

The defining financial behavior of a growth company is the reinvestment rate. Instead of paying out retained earnings as dividends, management reinvests capital into specific growth drivers, such as Research and Development (R&D), sales force expansion, infrastructure scaling, and strategic mergers and acquisitions.

By retaining earnings, the company aims to compound its intrinsic value. If a company can reinvest capital at a Return on Invested Capital (ROIC) that exceeds its Weighted Average Cost of Capital (WACC), it creates shareholder value. Conversely, if a company grows for the sake of growth but invests at returns below its cost of capital, it destroys value despite rising revenue figures.

Since these companies often burn cash to fuel expansion before becoming profitable, they frequently rely on external funding. Understanding the difference between Angel Investors vs Venture Capital is crucial for founders, as these are the primary sources of early-stage liquidity for high-growth entities.

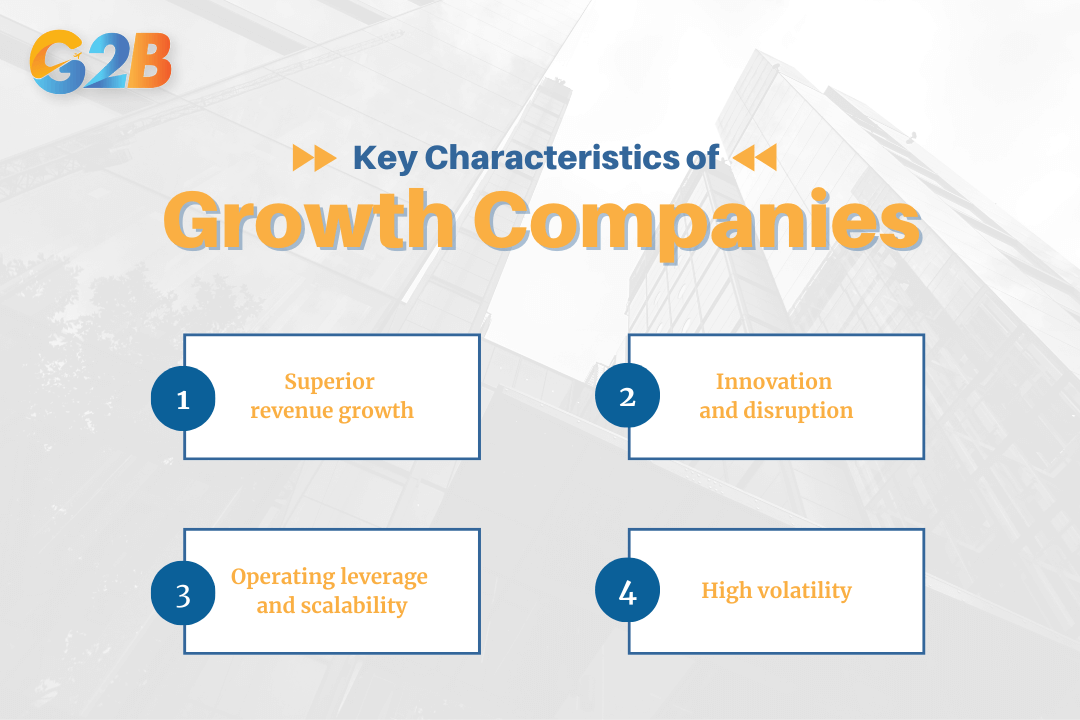

Key characteristics of growth companies

Identifying a true growth company requires analyzing specific financial characteristics, including high revenue growth rates, expanding operating margins, innovative product lines, and massive total addressable markets (TAM).

Identifying a true growth company requires analyzing specific financial characteristics

Superior revenue growth

The most visible metric is top-line growth. A growth company typically demonstrates annual revenue growth of 20% or higher, significantly outpacing the historical S&P 500 average or the list of Fortune 500 companies. This growth is rarely linear; it is often exponential in the early stages (the "hockey stick" curve) before stabilizing as the company matures.

Operating leverage and scalability

Successful growth companies utilize operating leverage to increase profitability as they scale. Operating leverage occurs when a company can grow revenue faster than its fixed costs, achieving economies of scale.

- Software-as-a-Service (SaaS) companies are prime examples of high operating leverage. Once the software is developed (a fixed cost), the cost to serve each additional customer (variable cost) is negligible.

- This dynamic allows for margin expansion over time. As revenue grows, the operating profit flows through to the bottom line at a higher rate.

Innovation and disruption

Growth companies often act as market disruptors. They leverage innovative technologies or business models to displace incumbents. This disruption often creates a temporary monopoly or a significant economic moat that protects their market share from competitors. They often emerge from a high-potential growth industry, riding a secular trend that lifts all boats in the sector.

High volatility

Because their value is derived from future expectations, growth stocks exhibit high beta, meaning they are significantly more volatile than the broader market. When market sentiment shifts, or if the company misses a quarterly earnings forecast, the stock price can fluctuate violently.

Stay ahead of global macro-economic trends and regulatory shifts. Follow G2B for more information on business strategy and company formation in Vietnam!

Critical KPIs for analyzing growth companies

Traditional accounting metrics like Net Income can be misleading for growth companies, specifically those in the tech or SaaS sectors that invest heavily in intangible assets. A robust financial plan for a growth company must focus on unit economics rather than just bottom-line profit.

1. LTV: CAC Ratio (Unit economics)

The health of a growth company is determined by its unit economics. The relationship between the Lifetime Value (LTV) of a customer and the Customer Acquisition Cost (CAC) dictates sustainability.

- CAC: The total cost of sales and marketing divided by the number of new customers acquired.

- LTV: The gross profit a customer generates over the entire duration of their relationship with the company.

A healthy growth company typically targets an LTV: CAC ratio of 3:1 or higher to ensure sustainable expansion. If the ratio is 1:1, the company is spending exactly what it makes to acquire a customer, which leads to value destruction after factoring in operating costs.

2. Churn rate

Growth is impossible if the "leaky bucket" effect drains customers faster than they can be acquired. Churn rate measures the percentage of customers who cancel their subscriptions or stop purchasing within a given period. Low churn is critical for the compounding effect of revenue. A high-growth company must maintain a monthly churn rate below 1% for enterprise clients or below 5% for SMB (Small to Mid-sized Business) clients to maintain its trajectory.

3. Net revenue retention (NRR)

NRR measures the percentage of recurring revenue retained from existing customers, including upgrades, cross-sells, and downgrades. An NRR above 100% indicates that the company can grow without acquiring a single new customer. This is the "Holy Grail" of growth investing. It signifies that the product is so "sticky" and valuable that existing customers naturally spend more over time (expansion revenue).

The mechanics of growth valuation

Valuing a growth company is challenging because standard metrics like the Price-to-Earnings (P/E) ratio are often undefined (due to negative earnings) or astronomically high. Financial professionals utilize alternative valuation methodologies, such as the Price-to-Sales (P/S) ratio, the PEG ratio, and Discounted Cash Flow (DCF) analysis.

1. Price-to-Sales (P/S) ratio

Since many growth companies sacrifice current profits for reinvestment, the P/E ratio is useless. The Price-to-Sales (P/S) ratio compares the company's market capitalization to its total revenue.

- This metric is useful for comparing companies within the same sector (e.g., Cloud Computing or Biotech).

- However, investors must be wary: a low P/S ratio can sometimes indicate low gross margins, while a high P/S typically implies high margins and high expected growth.

2. The PEG ratio (Price/earnings-to-growth)

Popularized by Peter Lynch, the PEG ratio refines the P/E ratio by dividing it by the annual earnings growth rate. It is directly tied to the concept of earnings per share (EPS).

- Formula: (P/E Ratio) / (Annual EPS Growth Rate)

- A PEG ratio of 1.0 is considered fairly valued.

- A PEG ratio below 1.0 suggests the stock may be undervalued relative to its growth potential.

- A PEG ratio above 2.0 often signals overvaluation, though high-quality growth companies often trade at premiums.

3. Discounted cash flow (DCF) and terminal value

The most rigorous valuation method is the Discounted Cash Flow (DCF) analysis. This involves forecasting the company's free cash flows to firm (FCFF) for 5 - 10 years and discounting them back to the present value using the Weighted Average Cost of Capital (WACC). For growth companies, a substantial portion of the valuation is derived from the Terminal Value - the estimated value of the company beyond the forecast period. Because the bulk of the cash flow is expected in the distant future, small changes in the discount rate (driven by interest rates) can cause massive swings in the estimated fair value.

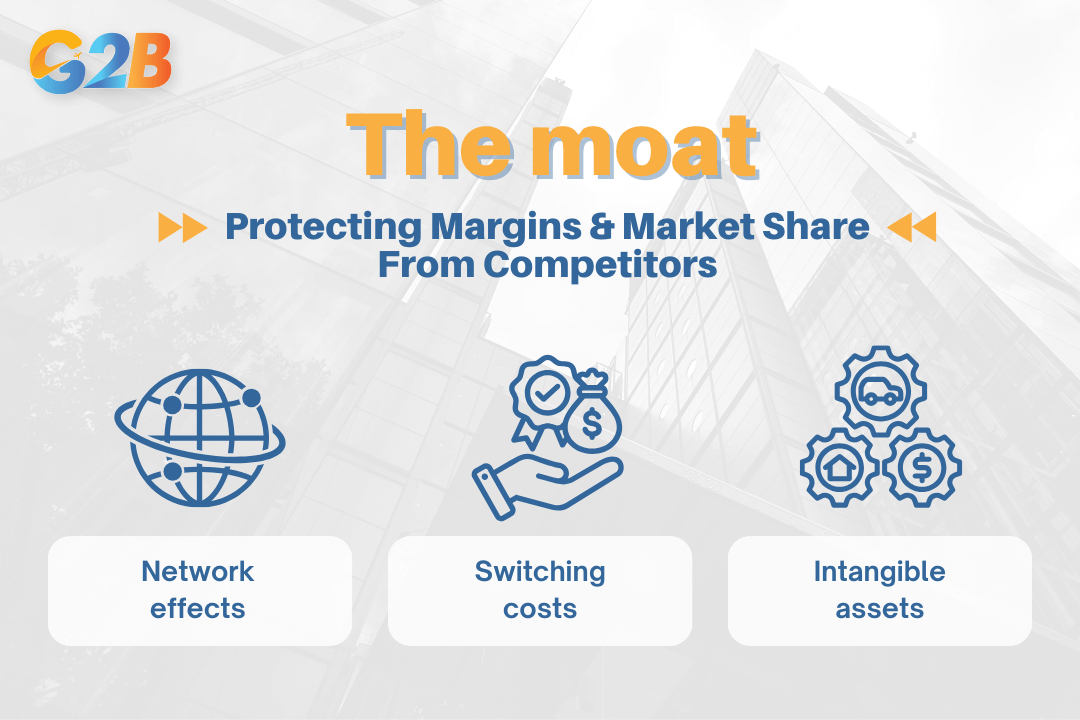

Economic moats

For a growth company to survive the transition to maturity, it must establish a durable economic moat. A moat is a structural advantage that protects margins and market share from competitors.

The moat protects margins and market share from competitors

1. Network effects

The network effect occurs when a product or service becomes more valuable as more people use it. Social media platforms, payment networks, and marketplaces rely on this moat. Once a critical mass is reached, it becomes nearly impossible for a competitor to displace the incumbent, granting them a significant first mover advantage.

2. Switching costs

High switching costs lock customers into an ecosystem. In the B2B SaaS world, once a company integrates a software solution into its workflow, migrating to a competitor is expensive, time-consuming, and risky. This creates pricing power and predictable recurring revenue.

3. Intangible assets

Intangible assets include patents, brand reputation, and regulatory licenses.

- Biotech companies rely on patents to protect their drug formulations.

- Consumer brands rely on reputation to charge premium prices.

Risks associated with growth investing

Investing in growth companies offers high rewards but carries significant specific risk factors, such as valuation multiple compression, execution failure, and interest rate sensitivity.

1. Multiple compression

Multiple compression occurs when the market decides that a company's future growth prospects are less rosy than previously thought. A company might continue to grow earnings, but if the P/E ratio contracts from 50x to 25x, the stock price will plummet by 50% even if earnings remain flat. This risk is highest when a growth company transitions from "hyper-growth" to "mature growth." Investors must anticipate this deceleration and value the company accordingly.

2. Interest rate sensitivity

Growth stocks are long-duration assets. Their value is tied to cash flows far in the future.

- Low interest rates: Future cash flows are discounted at a low rate, making them highly valuable today. This fuels growth stock rallies.

- High interest rates: The discount rate rises, significantly reducing the Present Value (PV) of future earnings.

When the Federal Reserve raises interest rates, growth stocks generally suffer more than value stocks because their valuations are more sensitive to the cost of capital. This sensitivity is often magnified during a global recession, where capital becomes expensive and risk appetite disappears.

3. The "growth trap"

A growth trap occurs when a company increases revenue but fails to ever achieve profitability. This often happens when the Total Addressable Market (TAM) is smaller than anticipated, or when competition erodes pricing power, preventing the company from ever leveraging its fixed costs.

Understanding the mechanics of a growth company requires moving beyond simple stock price observation and analyzing the underlying engine of value creation. Whether analyzing SaaS valuation metrics, calculating unit economics, or assessing economic moats, the goal is to identify businesses that can sustain high rates of return on invested capital over long periods. To support this trajectory, companies must secure the right equity financing partners early on to ensure they have the runway to achieve their vision.