Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom A GmbH (definition) in Germany is the most respected and popular legal structure for entrepreneurs looking to establish a business with limited liability. Renowned for its high credibility and robust legal framework, the GmbH offers a clear path for both domestic and international founders aiming to make their mark on Europe's largest economy. This article will explore the entire process, from understanding the core definition and navigating the formation steps to managing taxation and ongoing compliance.

This article explains the key concepts of a GmbH, helping businesses and entrepreneurs gain a clearer understanding of how this corporate structure operates. We specialize in company formation in Vietnam. For technical guidance on establishing or managing a GmbH, please consult a qualified German legal or financial expert.

What is GmbH?

A GmbH is a German legal entity and the most common type of private limited company in the country. The acronym GmbH stands for Gesellschaft mit beschrankter Haftung, which translates to "company with limited liability." This name highlights its core feature: the limitation of shareholder liability. As a legal entity, a GmbH can enter into contracts, own assets, and sue or be sued in its own name.

The fundamental advantage of a GmbH is the robust personal asset protection it offers its owners (Gesellschafter, or shareholders). In the event of insolvency or debt, creditors can typically only claim against the company's assets, not the personal wealth of the shareholders. This legal firewall makes it a secure and attractive option for entrepreneurs. The GmbH is internationally recognized as the equivalent of a private limited company (Ltd.) in the United Kingdom or a Limited Liability Company (LLC) in the United States. A GmbH requires a minimum share capital of €25,000, of which at least €12,500 must be paid in at the time of registration. Unlike public companies (AG in Germany), a GmbH is always a private limited entity.

How to establish a GmbH?

The formation of a GmbH is a structured, formal process governed by German law and requires several mandatory steps. A GmbH needs at least one shareholder (which can be an individual or another company), a designated managing director, and a registered German business address. The entire process culminates in the company's registration in the Commercial Register, at which point it gains its full legal status and liability protection.

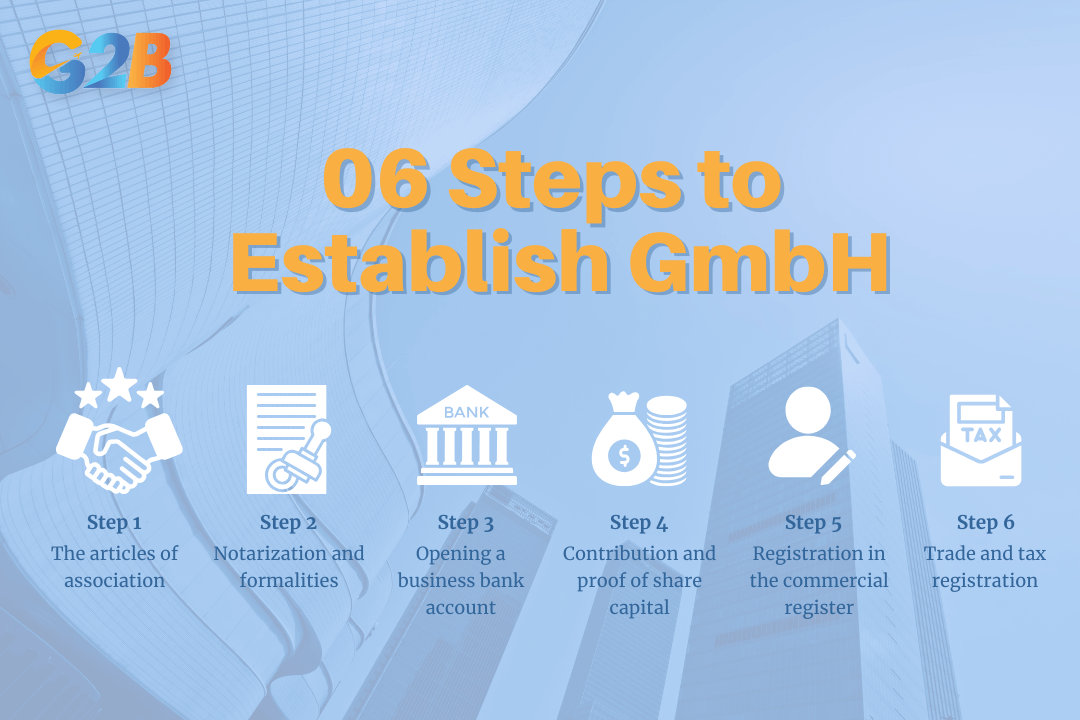

There are 06 steps to establish a GmbH

Step 1: The articles of association (Gesellschaftsvertrag)

The foundational document of any GmbH is the Gesellschaftsvertrag, or the articles of association. This document acts as the company's internal constitution, outlining its core operational rules and the rights and obligations of its shareholders. While a customized version is common for complex ventures, many founders opt for a standardized template known as the Musterprotokoll (model protocol). The Musterprotokoll is a cost-effective and simpler alternative suitable for straightforward formations, specifically those with:

- Cash-only capital contributions.

- A maximum of three shareholders.

- Only one appointed managing director.

Capital contribution may be made in cash or in-kind assets; in case of in-kind contributions, these must be clearly described and evaluated in the articles, supported by a founder's report.

Regardless of the format, the articles of association must legally contain several key pieces of information, including the company's name and official address, its business purpose, the amount of share capital, and the names of the shareholders and their respective contributions. Before proceeding, the company name should be checked and confirmed for uniqueness and compliance at the local chamber of commerce (IHK).

Step 2: Notarization and formalities

In Germany, the formation of a GmbH is not a simple paperwork filing; it requires formal certification by a public notary (Notar). This step is mandatory and cannot be skipped. The notary's role is to verify the identities of the founders, authenticate the articles of association, and ensure all legal requirements are met. The notary will also prepare and oversee the signing of the application to the Commercial Register. For standard cash-only formations, modern regulations now permit this notarization process to be conducted online via a secure video link, offering greater convenience for international founders. All shareholders or their properly authorized representatives must be present, and non-German speakers must have an officially recognized interpreter.

Step 3: Opening a business bank account

Once the articles of association have been notarized, the next step is to open a corporate bank account in the name of the GmbH. German banks will require the notarized formation documents to proceed. This account is essential for the next crucial stage: depositing the share capital. It must be a dedicated business account for the company, which will be styled as "GmbH in Grundung" or "GmbH i.G." (in formation) during this interim period. Foreign founders should note that some banks may apply strict screening to international applicants; preparing documentation in advance is recommended.

Step 4: Contribution and proof of share capital

The legal minimum share capital, known as Stammkapital, for a GmbH is €25,000. Before the company can be officially registered, the shareholders must pay in at least half of this amount, totaling a minimum of €12,500. The notary requires official proof of this deposit, typically in the form of a bank statement, before they will file the registration documents. It is critical to understand that even if only half is initially paid, the shareholders remain personally liable for the full, outstanding €25,000 until it is fully contributed to the company.

Step 5: Registration in the commercial register (Handelsregister)

This is the most critical step in the formation process. The Handelsregister, or Commercial Register, is the official public ledger for all businesses in Germany. The GmbH only legally comes into existence as a limited liability entity after its entry is published in this register. Until that moment, the founders are personally liable for any business activities conducted. The notary is responsible for electronically applying with the local court that manages the register, and the registration is typically completed within a few weeks.

Step 6: Trade and tax registration

With the company officially registered in the Commercial Register, the final administrative steps involve registering with the relevant authorities. This includes:

- Trade office (Gewerbeamt): All commercial business activities must be registered here to receive a trade license.

- Tax office (Finanzamt): The company must register with the local tax office to receive its tax number (Steuernummer) and VAT identification number.

- Transparency register (Transparenzregister): This register requires the disclosure of the company's beneficial owners, and registration must be completed within two weeks of receiving the Commercial Register statement.

- Chamber of commerce and industry (IHK): Membership is typically mandatory for commercial enterprises.

Taxation of a GmbH

A GmbH in Germany is subject to several distinct corporate taxes, resulting in a combined approximate tax burden of around 30% on profits. Understanding these components is crucial for financial planning.

- Corporate income tax (Korperschaftsteuer): This is a federal tax levied at a flat rate of 15% on the company's taxable profits.

- Solidarity surcharge (Solidaritatszuschlag): An additional surcharge of 5.5% is applied to the corporate income tax amount, not the profit itself, resulting in a total corporate tax burden of 15.825% on taxable profit.

- Trade tax (Gewerbesteuer): This is a municipal tax that varies depending on the company's location, as each municipality sets its own multiplier. The rate typically ranges from 7% to 17%.

- Value added tax (VAT) (Umsatzsteuer): A GmbH must charge VAT on its goods and services, with the standard rate currently at 19%. This is a pass-through tax, but it requires regular filings.

- Capital gains tax on dividends (Kapitalertragsteuer): When the GmbH distributes profits to its shareholders as dividends, these payments are subject to a withholding tax at a flat rate of 25% plus solidarity surcharge only if paid to foreign shareholders or domestic corporations. For individuals resident in Germany, only 60% of dividend income is taxed at progressive rates via the partial-income procedure.

Accounting and financial reporting

The German Commercial Code (Handelsgesetzbuch, HGB) imposes strict accounting and reporting obligations on a GmbH. The company is legally required to maintain a meticulous double-entry bookkeeping system.

Annually, the GmbH must prepare formal financial statements, known as the Jahresabschluss. This package includes a balance sheet, a profit and loss statement, and, depending on the company's size, an appendix with further details. Furthermore, a GmbH has a legal duty to publish these financial statements in the Federal Gazette (Bundesanzeiger). This ensures transparency and public access to the company's financial plan and health. The requirement for a formal audit depends on the company meeting certain size thresholds related to its balance sheet total, annual turnover, and number of employees.

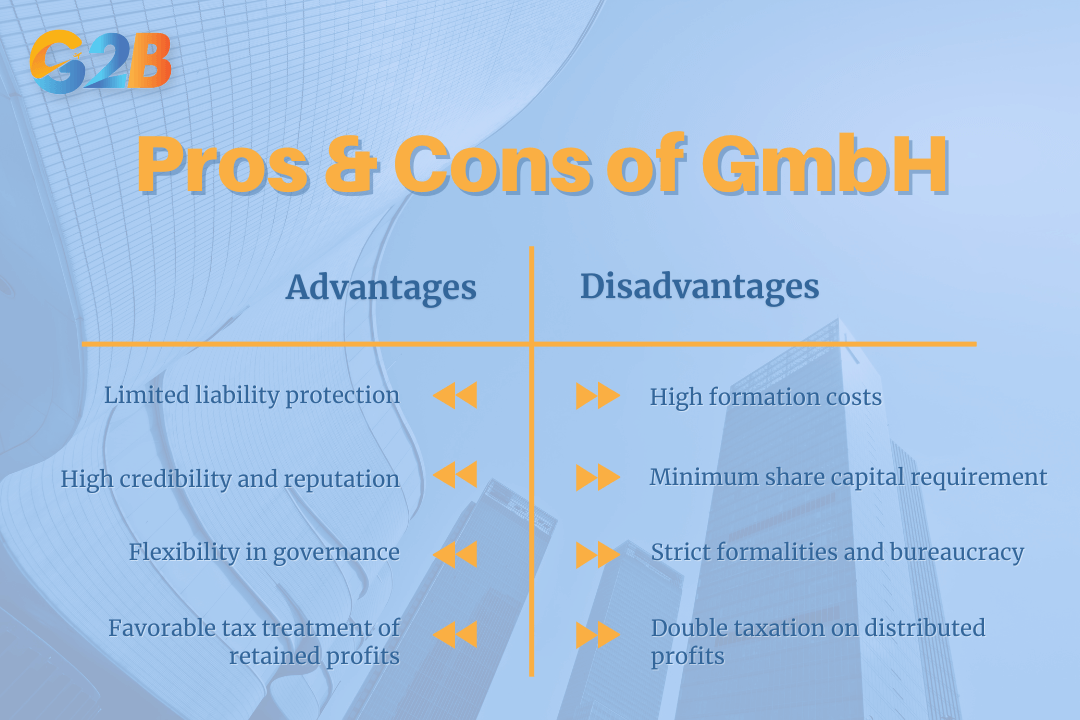

Advantages and disadvantages of a GmbH

Choosing the GmbH structure offers significant benefits but also comes with responsibilities and costs. A balanced view is essential for making an informed decision.

GmbH brings many advantages and disadvantages

Key advantages for businesses

- Limited liability protection: This is the primary advantage. Shareholders' personal assets are protected from business debts, limiting their financial risk to the amount of their capital contribution.

- High credibility and reputation: The GmbH is a highly respected legal form in Germany and internationally. The €25,000 minimum capital requirement signals financial stability and seriousness to banks, suppliers, and customers.

- Flexibility in governance: A GmbH can be established by a single shareholder and offers considerable flexibility in structuring its internal management through the articles of association.

- Favorable tax treatment of retained profits: Profits that are kept within the company (retained earnings) are taxed at the lower corporate rate of around 30%, which is often more favorable than the progressive personal income tax rates that would apply to sole proprietorship structures.

Potential disadvantages to consider

- High formation costs: Establishing a GmbH involves significant administrative expenses, including notary fees, court fees for the commercial register, and trade registration fees. These costs can easily amount to several thousand euros.

- Minimum share capital requirement: The €25,000 share capital is a significant financial hurdle for many startups and small entrepreneurs, even though only half must be paid initially.

- Strict formalities and bureaucracy: The formation process is rigid, and the ongoing obligations for accounting, annual reporting, and publication are demanding and require professional expertise.

- Double taxation on distributed profits: While retained profits are taxed at the corporate level, once they are distributed to shareholders as dividends, they are taxed again at the personal level (capital gains tax), leading to double taxation. This is a common consideration when comparing C-Corporation vs S-Corporation structures in other jurisdictions.

Comparison between GmbH and LLCs in Vietnam

While both the German GmbH and the Vietnamese Limited Liability Company (LLC) are designed to limit owner liability, they operate within very different legal and economic frameworks. A direct comparison highlights these key distinctions.

| Feature | GmbH in Germany | LLC in Vietnam |

|---|---|---|

| Legal Personality | A separate legal entity from its owners. | A separate legal entity from its owners. |

| Number of Members | Can be formed by a single member (Ein-Personen-GmbH) or multiple members. | Can be a single-member LLC or a multi-member LLC (limited to max 50 members). |

| Capital Requirement | Mandatory minimum share capital of €25,000. | No generally applicable minimum capital requirement, except for certain regulated business lines (e.g., finance, real estate). |

| Governance | Managed by one or more managing directors (Geschaftsfuhrer) appointed by the shareholders' meeting. | Governance structure includes a Members' Council, a Chairman, and a Director (or General Director). |

| Formation Formalities | Strict, formal process requiring a public notary, registration in the Commercial Register, and multiple administrative steps. | Requires application for an Enterprise Registration Certificate (ERC) and Investment Registration Certificate (IRC) for foreign investors; the process is administrative rather than notarial. |

| Credibility & Reputation | Very high national and international credibility due to strict regulations and high capital requirements. | Credibility is strong within Vietnam and Southeast Asia, but it may have less international recognition compared to a GmbH. |

The GmbH structure, with its strong liability protection and high reputation, offers a powerful vehicle for success in the German market. While the formation process is detailed and the compliance requirements are strict, the long-term benefits of credibility and legal security are invaluable. By understanding the steps, costs, and obligations outlined in this guide, you are well-equipped to make a strategic decision for your business venture.