Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Charter capital vs. investment capital in Vietnam represents the most critical financial distinction foreign investors must master during the FDI company establishment process. Misunderstanding these two metrics consistently leads to licensing rejections, compliance penalties, and frozen bank accounts. When entering the Vietnamese market, foreign investors must navigate a dual-licensing system where entirely different legal frameworks govern corporate ownership and project execution. This guide clarifies the exact differences between charter capital and investment capital, detailing their legal definitions, compliance timelines, and practical impacts on your business operations.

Legal framework in Vietnam

Establishing a Foreign Direct Investment (FDI) enterprise requires strict adherence to two primary legal frameworks: the Law on Enterprises 2020 and the Law on Investment 2020. Vietnamese jurisprudence mandates a clear separation between the corporate entity itself and the investment project that the entity executes. This separation creates the distinction between charter and investment capital.

The Law on Enterprises 2020 governs the corporate entity. It regulates the internal management, shareholder rights, and equity structures. Under this law, the licensing authorities issue the Enterprise Registration Certificate (ERC). The ERC functions as the corporate birth certificate and exclusively records the Charter Capital.

Conversely, the Law on Investment 2020 governs the specific business project. It assesses the project's socio-economic impact, land use, and overall financial feasibility. Under this law, licensing authorities, such as the Department of Planning and Investment (DPI) and the Management Boards of Industrial Zones, issue the Investment Registration Certificate (IRC). The IRC functions as the project approval document and exclusively records the Investment Capital.

Note: Under the Law on Investment 2025 (effective March 1, 2026), the licensing sequence may allow ERC issuance before IRC in certain cases.

What is the charter capital in Vietnam?

Charter capital is the total value of assets contributed or committed to be contributed by members or shareholders when establishing a company in Vietnam. It represents the actual equity ownership of the enterprise and establishes the limit of financial liability for the investors. Under the Law on Enterprises 2020, charter capital serves three fundamental functions. First, it dictates the exact ownership ratio, voting rights, and dividend distribution among shareholders. Second, it defines the financial liability ceiling for limited liability companies and joint-stock companies. Third, it serves as the primary indicator of a company’s financial capacity to business partners and creditors.

The strict 90-day capital contribution rule

The most critical compliance metric regarding charter capital is the 90-day capital contribution rule. The Law on Enterprises 2020 mandates that owners must fully contribute their committed charter capital within 90 days from the issuance date of the Enterprise Registration Certificate (ERC). Investors must remit this capital precisely. Funds must originate from the investor’s overseas bank account and be transferred directly into the newly established company's Direct Investment Capital Account (DICA) in Vietnam. Attempting to bring cash across the border or transferring funds from an unapproved third-party account violates Vietnamese foreign exchange regulations and will not be recognized as a legal capital contribution.

Allowable assets for contribution

Investors can contribute charter capital using various asset types, such as Vietnamese Dong, freely convertible foreign currencies, gold, land use rights, intellectual property rights, and technological know-how. Non-cash assets require formal valuation by independent appraisal agencies, such as state-licensed valuation firms or certified independent auditors, before they can be legally recorded as charter capital.

What is investment capital in Vietnam?

Investment capital is the total financial resource required to implement an investment project. While charter capital represents only the equity put in by the owners, investment capital encompasses the entire cost of the project from inception to operation, as approved and recorded on the Investment Registration Certificate (IRC). The Law on Investment 2020 defines investment capital as a comprehensive financial metric that proves to the licensing authorities that the project is financially viable. Licensing authorities use this figure to determine whether the investor possesses the capital required to secure land leases, build facilities, purchase equipment, and sustain initial operations.

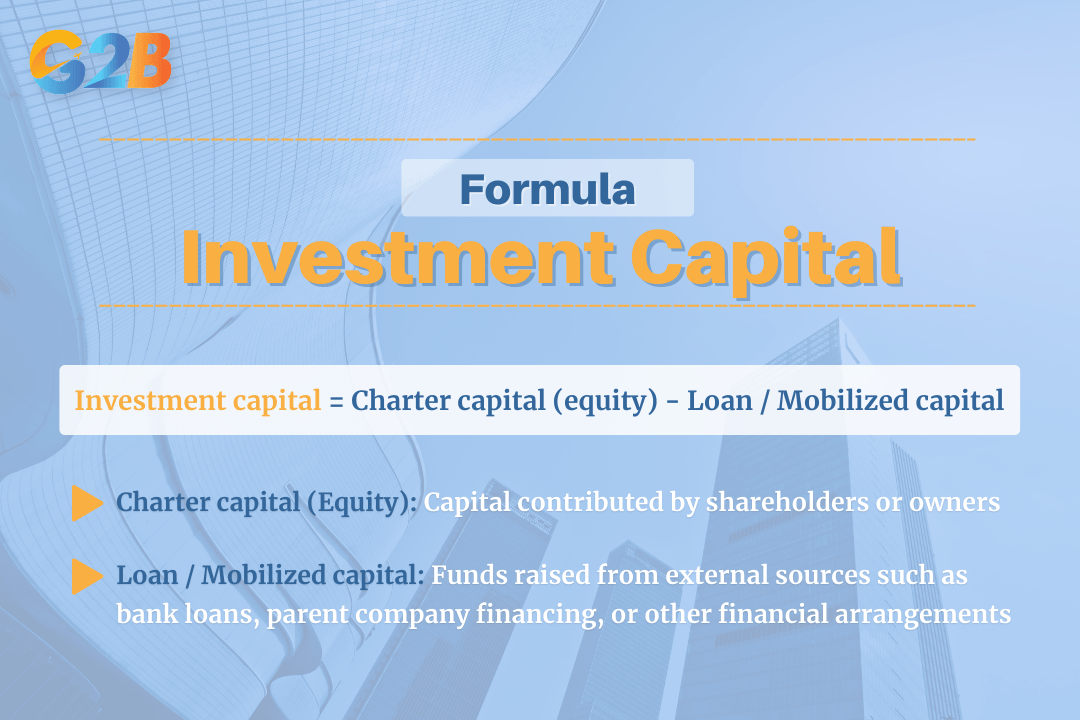

The components of investment capital

Investment capital includes various funding sources, such as equity contribution (charter capital), primarily loan capital including foreign bank loans, parent company loans, and domestic mobilized capital.

The fundamental formula is: Investment Capital = Charter Capital (Equity) + Loan Capital / Mobilized Capital

When foreign investors declare their investment capital, they must provide a detailed disbursement schedule to the DPI. This schedule outlines exactly when the equity will be injected and when the loans will be drawn down. If the project relies heavily on loan capital, the investors must provide proof of financial capacity to secure these loans, such as bank credit lines, parent company financial statements, or formal loan agreements.

The fundamental formula of investment capital

Regulatory oversight of loan capital

If the investment capital includes medium- or long-term foreign loans (loans with a term exceeding 12 months), the FDI enterprise must formally register these loans with the State Bank of Vietnam (SBV) before drawing down the funds. The SBV stringently monitors these loans to manage the national foreign debt limits. Furthermore, the total loan amount drawn down cannot exceed the difference between the registered investment capital and the registered charter capital.

Comparison between charter capital and investment capital in Vietnam

To ensure absolute clarity during the FDI company establishment process, foreign investors must understand the exact statutory differences between these two financial metrics.

| Criteria | Charter capital | Investment capital |

|---|---|---|

| Governing law | Law on Enterprises 2020 | Law on Investment 2020 |

| Shown on | Enterprise Registration Certificate (ERC) | Investment Registration Certificate (IRC) |

| Nature | Ownership capital (Equity limit of liability) | Total project capital (Required funds to execute business) |

| Includes loans? | No | Yes |

| Affects the ownership ratio? | Yes | No |

| Required for domestic companies? | Yes | Only if having an investment project (mostly FDI) |

| Mandatory 90-day contribution? | Yes (Strictly enforced) | Not always (Depends on the project timeline in the IRC) |

Why this distinction matters in Vietnam

Understanding the legal boundary between charter capital and investment capital is not a mere academic exercise; it dictates your corporate compliance, tax obligations, and operational freedom in Vietnam.

For licensing approval and feasibility assessment

During the FDI company establishment process, licensing authorities critically assess the proposed capital structure. The DPI evaluates whether the stated investment capital is mathematically sufficient to carry out the registered business lines. If a foreign investor proposes establishing a large-scale manufacturing plant but registers an investment capital of only VND 500 million, the DPI will reject the application due to financial infeasibility. The authorities mandate that the investment capital logically covers fixed assets and initial operating expenses until the company generates revenue.

For Direct Investment Capital Account (DICA) operations

Vietnamese foreign exchange control is exceptionally strict. Every FDI enterprise must open a Direct Investment Capital Account (DICA) at a licensed commercial bank in Vietnam. The bank monitors the DICA based on the figures listed in the IRC and ERC.

- Charter capital remittance: The bank strictly enforces the 90-day rule. If you attempt to remit charter capital on day 95, the bank will freeze the transaction.

- Loan capital drawdown: The bank will only allow foreign loan transfers into the DICA if the loan amount fits within the approved investment capital margin (Investment Capital minus Charter Capital). If an investor attempts to borrow more than this margin, the bank will block the transfer, requiring the investor to officially amend the IRC to increase the total investment capital.

For tax implications and thin capitalization

The ratio between charter capital and investment capital heavily influences corporate tax strategies. Vietnamese tax authorities scrutinize highly leveraged companies. Under Decree 132/2020/ND-CP regarding tax administration for enterprises with related-party transactions, the deductibility of loan interest is capped at 30% of the total net operating profit plus interest, taxes, depreciation, and amortization (EBITDA). If an investor relies too heavily on inter-company loans to fund the investment capital while keeping charter capital artificially low, a significant portion of their interest expenses will not be tax-deductible, dramatically increasing their corporate income tax burden.

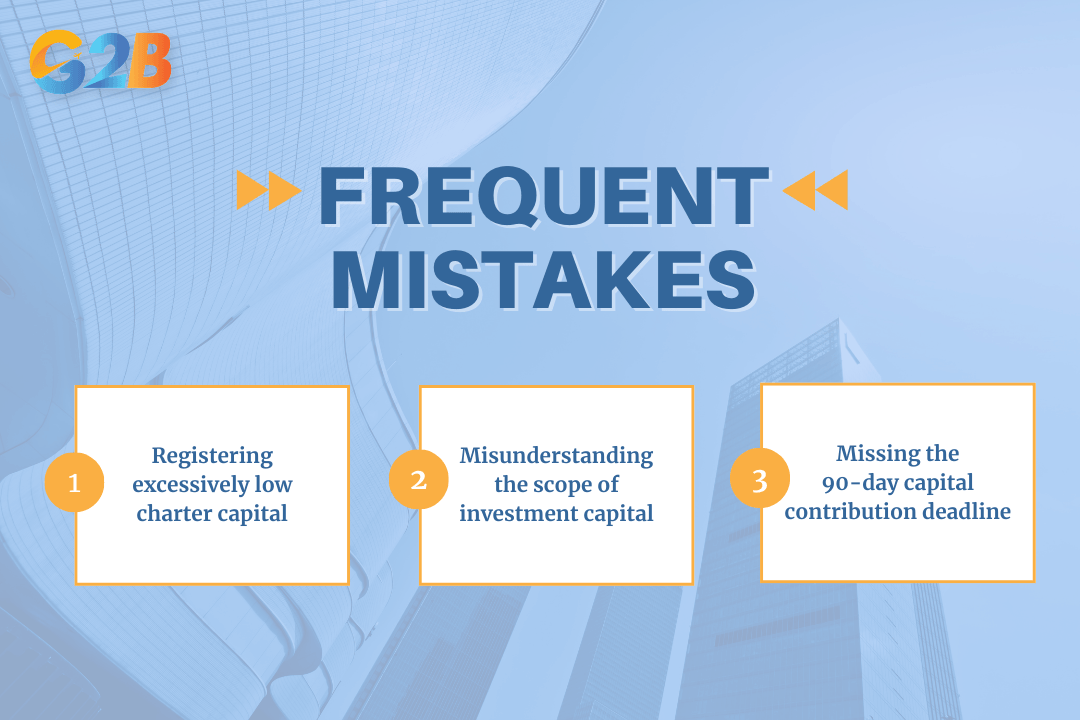

Frequent mistakes foreign investors make

Entering the Vietnamese market without expert legal guidance leads to predictable, costly errors regarding capital structuring.

Frequent mistakes that foreign investors usually make

Registering excessively low charter capital

Many investors attempt to register the absolute minimum charter capital (e.g., USD 10,000) to "reduce financial risk". This is a profound strategic error. A severely undercapitalized company will exhaust its funds within the first few months. Once the charter capital is depleted, the company cannot legally borrow foreign funds unless it has a higher approved investment capital on its IRC. Furthermore, low charter capital negatively impacts the issuance of investor visas and work permits, as authorities view the enterprise as a low-value contributor to the Vietnamese economy.

Misunderstanding the scope of investment capital

Foreign investors frequently mistake investment capital as solely the funds required for purchasing fixed assets. They fail to budget for operating expenses during the pre-revenue phase. Investment capital must encompass all financial requirements, including security deposits, legal fees, employee onboarding, and factory outfitting. Underestimating this figure forces the investor to undergo a complex, time-consuming administrative procedure to amend the IRC to inject more capital legally.

Missing the 90-day capital contribution deadline

The 90-day capital contribution rule is absolute. Investors often delay transferring funds due to internal parent-company approvals or banking delays in their home country. Failing to contribute charter capital within exactly 90 days from the ERC issuance date results in administrative fines ranging from VND 30 million to VND 100 million. Following the fine, the company is forced to adjust its registered charter capital down to the actually contributed amount, drastically damaging its corporate profile and potentially violating the financial commitments made in the IRC.

How to determine the right capital structure in Vietnam

Determining the exact figures for your charter capital and investment capital requires precise financial modeling and an understanding of DPI assessment criteria. Follow these steps to define your structure:

- Assess total project scale (investment capital): Calculate every expense required from day one until the company reaches the breakeven point. This includes capital expenditures (Capex) such as machinery, vehicles, and factory construction, alongside operating expenses (Opex) such as six to twelve months of payroll, rent, and administrative costs. The sum of these costs forms your target Investment Capital.

- Determine your equity strategy (charter capital): Decide how much cash the parent company or individual investors are willing to inject directly as non-refundable equity. This figure becomes your Charter Capital. Ensure this amount is liquid and ready to be wired within 90 days.

- Identify the funding gap (loan capital): Subtract the Charter Capital from the Investment Capital. This remaining amount must be covered by loans. Ensure you possess the verifiable financial capacity (e.g., parent company guarantee) to secure this loan amount, as the DPI will request proof during the licensing phase.

- Validate against Industry Standards: Consult with a corporate law consultant to ensure your proposed figures meet unwritten DPI expectations. For example, while there is no statutory minimum capital for a management consulting firm, DPI officials generally expect a minimum charter capital of USD 20,000 to USD 50,000 to consider the project viable.

Frequently asked questions (FAQs)

The FAQs below answer common questions and provide clearer insights into how these capital types are defined and applied in practice.

Can charter capital be equal to investment capital?

Yes, charter capital can be exactly equal to investment capital. This is the most common structure for foreign-invested service, trading, and technology companies that do not rely on bank loans or external debt to fund their operations. When these figures are equal, the investor commits to funding the entire project exclusively through equity contributions.

Can charter capital be increased or decreased later?

Yes, charter capital can be both increased and decreased after incorporation. Increasing charter capital is a standard procedure that requires passing a shareholder resolution, injecting the new funds into the DICA, and subsequently amending the ERC and IRC. Decreasing charter capital is legally permissible but administratively complex; it is generally only allowed after the company has operated continuously for more than two years, and the company must prove it can still pay all debts and liabilities after the capital reduction.

Does every foreign-invested company need to declare investment capital?

Yes, every foreign-invested company operating under an Investment Registration Certificate (IRC) must declare its investment capital. Because foreign investors must obtain an IRC to establish an enterprise in Vietnam (with rare exceptions regarding M&A transactions), declaring the total investment capital is a mandatory step in the FDI company establishment process.

What happens if you fail to contribute charter capital within 90 days?

If you fail to contribute the full charter capital within 90 days, you face severe administrative fines and mandatory corporate restructuring. The authorities will impose fines of up to VND 100 million. Furthermore, the company’s legal representative must immediately register a change to decrease the charter capital on the ERC to reflect the exact amount that was actually paid in. The shareholders who failed to contribute lose their corresponding voting rights and dividend entitlements.

Failing to differentiate between the equity recorded on your ERC and the total project financing recorded on your IRC leads to blocked bank transfers, rejected loan applications, and severe administrative penalties. Because the Department of Planning and Investment meticulously scrutinizes these figures before granting market entry, your capital structure must be mathematically sound, legally compliant, and strategically aligned with your long-term business goals.