Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom A general account is the foundational building block of a company's entire financial reporting system. Though the name might suggest a type of bank account, its true role is far more fundamental to the health and clarity of your business finances. It's not a place to hold money, but rather a core category within your accounting records used to sort and summarize every single financial transaction your business makes. Understanding this concept is the first step toward achieving a clear, accurate, and actionable view of your company's performance.

This article highlights the key aspects of managing a General Account to help businesses and investors gain a clear understanding of financial reporting. We specialize in company formation and do not provide legal or dispute resolution advice. For any legal matters, please consult a qualified lawyer or the relevant authorities.

What is a general account in business?

The general ledger acts as the central repository - the master book of accounts - that contains a complete record of every financial transaction a company has ever made, organized by account. If the general ledger is the filing cabinet, then the general accounts are the individual files within it, each labeled for a specific category like "Cash," "Sales Revenue," or "Office Supplies Expense."

The purpose of a general account is to systematically sort, store, and summarize a company's transactions. This systematic organization is what allows a business to translate thousands of individual transactions into meaningful financial reports. Every time your business engages in a financial activity - whether it's making a sale, paying an employee, purchasing inventory, or taking out a loan - the transaction is recorded in at least two general accounts using the double-entry bookkeeping method. This method ensures that the accounting equation (Assets = Liabilities + Equity) always remains in balance. The key functions and relationships of general accounts include:

- Serving the general ledger: The general ledger is the complete collection of all general accounts, summarizing all of a business's financial activities. It is the primary source of data used to generate a company's trial balance and official financial statements.

- Building the financial statements: The ultimate purpose of organizing transactions into general accounts is to prepare the key financial statements that reveal a company's performance and position. These statements are the balance sheet and the income statement.

- The balance sheet: This statement provides a snapshot of your company's financial health at a single point in time. It is built using the balances from your asset, liability, and equity accounts.

- The income statement: Also known as the Profit and Loss (P&L) statement, this report shows your company's profitability over a period of time (such as a month, quarter, or year). It is constructed from your revenue and expense accounts.

- Creating the chart of accounts: A well-organized list of all the general accounts used by a company is called a chart of accounts. This chart serves as the backbone of your financial reporting, providing a structured index of every category your business uses to track money. Each account is typically assigned a unique number for easy organization and identification in the accounting software.

In essence, a general account is not a physical account but a classification system. It is the core concept that brings order to the financial chaos of daily business operations, ensuring that every dollar is tracked, categorized, and reported accurately. Without this structure, creating reliable financial statements would be impossible.

A well-maintained General Account is crucial for any business to track financial performance, monitor cash flow, and ensure compliance with accounting standards. For entrepreneurs looking to expand or start a business in Vietnam, the first step is to register a company properly in Vietnam, which lays the legal foundation for proper accounting and financial management.

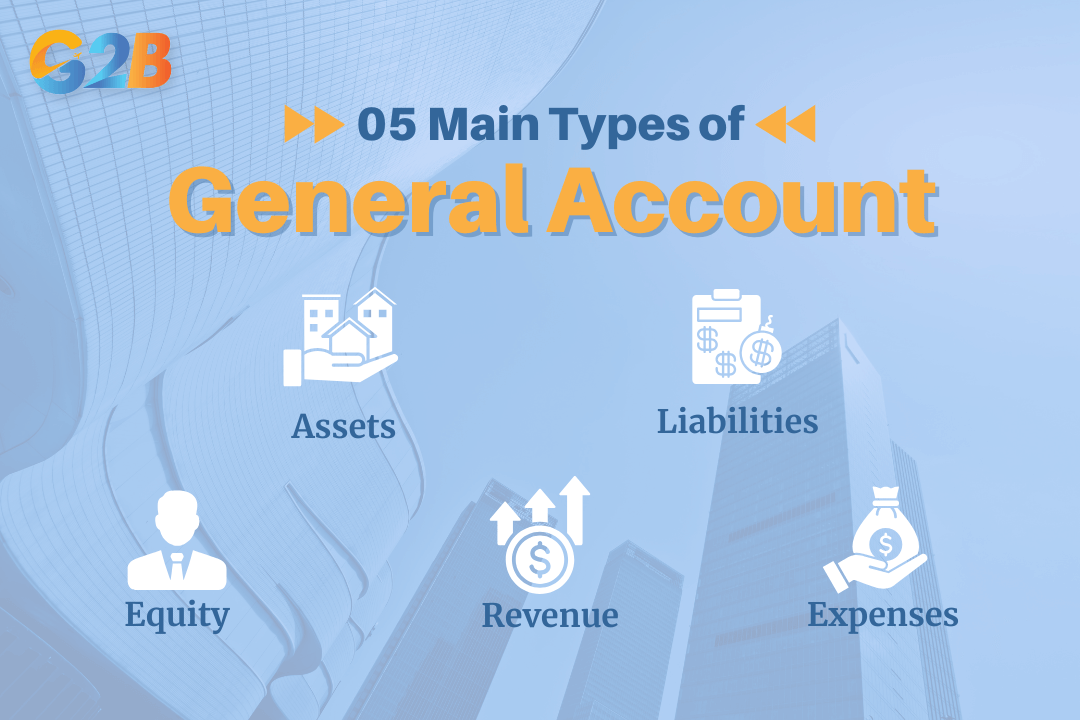

The 5 main types of general ledger accounts

Every transaction a business conducts can be sorted into one of five fundamental categories or types of general accounts. These five pillars form the basis of the entire accounting system and are directly linked to the core accounting equation. They provide the complete framework needed to understand a company's financial position, performance, and overall health. The information from asset, liability, and equity accounts flows into the balance sheet, while information from revenue and expense accounts flows into the income statement. Understanding these five types is the first step in mastering your company's finances, a core part of our small business bookkeeping services. The five main types of general ledger accounts are:

- Assets

- Liabilities

- Equity

- Revenue

- Expenses

The 5 main types of general ledger accounts

Assets

An asset is any resource that your business owns that has future economic value. Assets are economic resources owned by the business that can be used to produce positive economic value, can be converted into cash, or are used to generate revenue and support business operations. In simpler terms, assets are the valuable items your company owns and uses to operate.

Asset accounts are a critical component of the balance sheet and are typically listed first, reflecting what the company has at its disposal. They are often categorized based on their liquidity, or how easily they can be converted into cash.

- Current assets: These are assets that are expected to be converted into cash or used up within one year. They are essential for funding day-to-day operations. Examples of current asset accounts include:

- Cash and cash equivalents: The most liquid of all assets, this includes physical currency, bank account balances, and other highly liquid instruments.

- Accounts receivable: This is the money owed to your business by customers for goods or services that have been delivered but not yet paid for.

- Inventory: This includes the value of raw materials, work-in-progress goods, and finished products that the company plans to sell.

- Prepaid expenses: These are payments made in advance for future expenses, such as an annual insurance premium or a rent deposit. The portion that has not yet been used is considered an asset.

- Non-current assets (or fixed assets): These are long-term assets that are not expected to be converted into cash or used up within one year. They are used over multiple periods to help generate revenue. Examples of non-current asset accounts include:

- Property, plant, and equipment (PP&E): These are tangible, long-term assets used in business operations, such as land, buildings, vehicles, machinery, and office furniture.

- Intangible assets: These are non-physical assets that still hold significant value, such as patents, trademarks, copyrights, and goodwill.

- Long-term investments: This includes investments in other companies or financial instruments that the business intends to hold for more than a year.

Liabilities

Liabilities represent what your business owes to others. Liabilities are the financial obligations or debts of a company that arise during the course of its business operations. They are claims by external parties against the company’s assets, meaning they are debts that must be settled over time.

Like assets, liabilities are a key component of the balance sheet and are also categorized based on their due date.

- Current liabilities: These are debts and obligations that are due to be paid within one year. Managing current liabilities is essential for maintaining healthy cash flow. Examples of current liability accounts include:

- Accounts payable: This represents the money your business owes to its suppliers or vendors for goods and services purchased on credit.

- Salaries and wages payable: This is the amount owed to employees for work they have performed but have not yet been paid for.

- Taxes payable: This includes all forms of taxes that the company has incurred but not yet paid to the government, such as income tax, payroll tax, and sales tax.

- Accrued expenses: These are expenses that have been incurred but not yet paid, such as interest on a loan or utility bills.

- Unearned revenue: This is money received from a customer for a product or service that has not yet been delivered or rendered. It represents an obligation to the customer.

- Non-current liabilities (or long-term liabilities): These are obligations that are not due for payment within one year. They typically relate to long-term financing and investment. Examples of non-current liability accounts include:

- Bank loans payable: This includes the principal amount of long-term loans taken from financial institutions.

- Bonds payable: This is money raised from investors through the issuance of bonds, which the company is obligated to repay over a period of years.

- Mortgage payable: This is a long-term loan used to finance the purchase of real estate.

Equity

Equity represents the net worth of the business. Equity is the residual interest in the assets of the business after deducting all liabilities. It is what is left over for the owners after all debts have been paid. Equity is calculated using the fundamental accounting equation: Assets - Liabilities = Equity.

The composition of equity accounts varies depending on the business structure (sole proprietorship, partnership, or corporation), but they all represent the ownership stake in the company.

Examples of common equity accounts include:

- Owner's capital or contributed capital: This account tracks the money or other assets that the owner(s) have invested into the business. For corporations, this is often represented by accounts like Common Stock and Paid-in Capital.

- Retained earnings: This account represents the cumulative net income of the business that has been retained for reinvestment rather than being paid out to owners as dividends or distributions. Every year, the company's net profit or loss is added to or subtracted from the retained earnings balance.

- Owner's draws or dividends: While technically contra-equity accounts, these track the money paid out from the business to its owners. Draws are common in sole proprietorships and partnerships, while dividends are distributions of profit to shareholders in a corporation.

- Other comprehensive income (OCI): This represents gains or losses that are excluded from net income, such as unrealized gains on certain investments or foreign currency translation adjustments.

Revenue

Revenue is the income your company generates from its primary business operations. Revenue, often called the "top line," represents the money a business earns from the sale of goods or the provision of services before any costs or expenses are deducted. Tracking revenue is essential for understanding sales performance and business growth.

Revenue accounts are temporary accounts that are reported on the income statement. At the end of each accounting period, their balances are closed out to retained earnings. Different types of revenue are recorded in separate general accounts to provide a more detailed view of the company's income streams. Examples of revenue accounts include:

- Sales revenue: The primary account for income generated from selling products.

- Service revenue: Income earned from providing services to customers.

- Interest income: Revenue earned from investments, such as interest from a business savings account or from loans made to others.

- Rental income: If a company owns and rents out property, this account tracks the income generated from those rentals.

- Commission revenue: Income earned by acting as an agent or intermediary in a transaction.

Expenses

Expenses are the costs of doing business. Expenses are the costs incurred in the process of generating revenue. They represent the outflow of money or consumption of assets required to run the company's day-to-day operations. Effectively managing expenses is critical for maximizing profitability.

Like revenue accounts, expense accounts are temporary accounts reported on the income statement. Their purpose is to be matched against the revenues they helped generate in a given period to calculate the company's net income or loss. Businesses incur many types of expenses, and each is tracked in its own general account for better analysis and control. Examples of common expense accounts include:

- Cost of goods sold (COGS): For companies that sell products, this represents the direct costs of producing or acquiring the goods that were sold during a period.

- Salaries and wages expense: The cost of employee compensation for the services they provide.

- Rent expense: The cost of leasing office space, retail locations, or other business premises.

- Utilities expense: The costs for essential services like electricity, water, gas, and internet.

- Marketing and advertising expense: Costs associated with promoting the business and its products or services.

- Office supplies expense: The cost of consumable items used in the office, such as paper, pens, and printer ink.

- Depreciation expense: The systematic allocation of the cost of a tangible asset (like a vehicle or equipment) over its useful life.

- Insurance expense: The cost of business insurance policies.

- Interest expense: The cost of borrowing money, such as interest on a loan.

Distinguishing a general account from a general investment account (GIA)

While the term "general account" is a core concept in business accounting, it's crucial not to confuse it with a very similar-sounding term used in the world of personal and corporate finance: the General Investment Account (GIA). This section will clarify the difference to ensure you avoid this common pitfall.

What is a general investment account (GIA)?

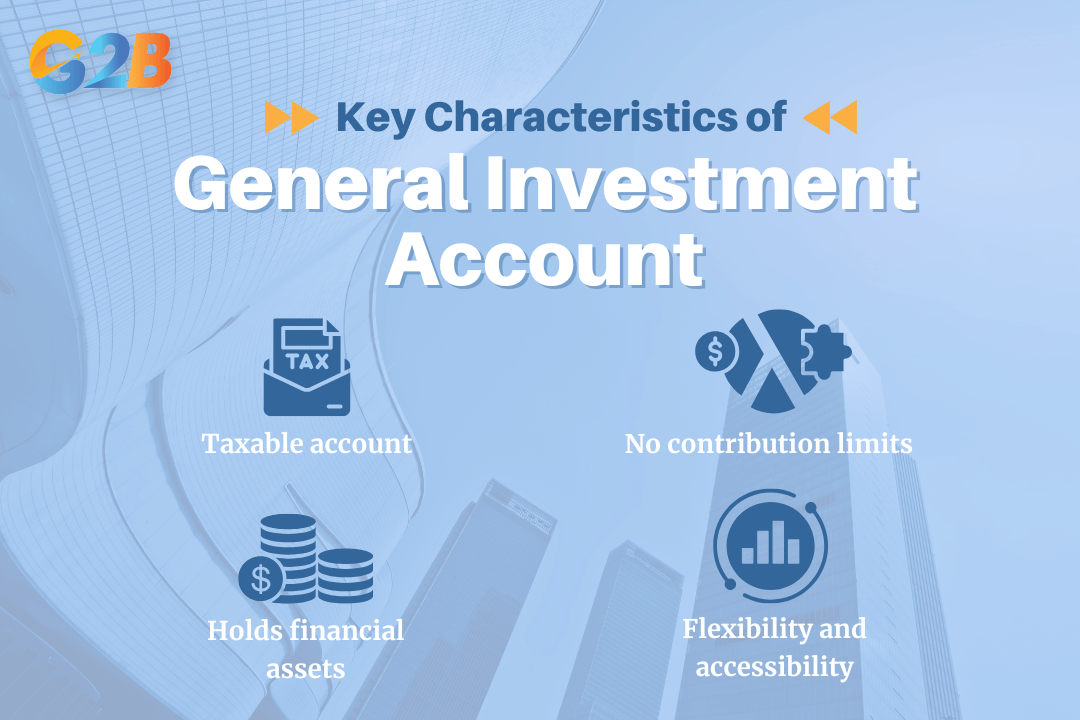

A General Investment Account, or GIA, is a standard, flexible investment account that allows individuals or entities to buy and hold a wide range of financial assets. Unlike an accounting general account, which is a record-keeping category, a GIA is an actual account provided by a bank or brokerage firm that holds real assets. It is a vehicle for investing money with the goal of generating a return. Key characteristics of a GIA include:

- Holds financial assets: A GIA is used to hold various types of investments, such as stocks, bonds, exchange-traded funds (ETFs), and mutual funds.

- No contribution limits: Unlike tax-advantaged retirement or savings accounts like an ISA (Individual Savings Account) in the UK or a 401(k) in the US, there is typically no limit to how much money you can invest in a GIA. This makes it a popular choice for investors who have already maxed out their contributions to tax-sheltered accounts.

- Flexibility and accessibility: Money in a GIA is generally not locked in, meaning you can withdraw your funds at any time. This flexibility makes it suitable for a variety of investment goals, from short-term to long-term.

- Taxable account: This is the most significant feature of a GIA. Unlike tax-advantaged accounts, the investment returns within a GIA are subject to tax. This means you may have to pay tax on any dividends you receive and Capital Gains Tax on any profits you make when you sell your investments.

There are 4 key characteristics of a GIA

Key differences in purpose and taxation

The primary differences between a business's general account and a General Investment Account come down to their fundamental purpose, context, and tax treatment. Let's break down these distinctions side-by-side.

1. Purpose and function:

- General account (accounting): Its purpose is purely for bookkeeping and financial reporting. It is an internal classification tool used to record, categorize, and summarize every financial transaction a business makes. It does not hold money or assets itself; it simply tracks them.

- General investment account (GIA): Its purpose is for investing and generating a return. It is an external account that actively holds financial assets like stocks and bonds. Its function is to grow wealth, not to track routine business operations.

2. Context and usage:

- General account (accounting): It exists solely within a company's accounting system (the general ledger). Every business, regardless of size, uses a system of general accounts to manage its finances.

- General investment account (GIA): It exists in the world of personal finance and corporate treasury. An individual might use a GIA for their personal savings, and a corporation might use one to invest its excess cash. It is a financial product offered by brokerage firms and banks.

3. What they contain:

- General account (accounting): It contains a historical record of transactions. For example, the "Cash" general account contains a detailed log of all cash inflows and outflows.

- General investment account (GIA): It contains financial assets. When you look at your GIA, you see a portfolio of stocks, bonds, funds, and a cash balance waiting to be invested.

4. Tax implications:

- General account (accounting): A general account is an internal calculation tool and has no direct tax implications itself. The balances within these accounts (specifically revenue and expense accounts) are used to calculate the company's taxable profit, upon which the business then pays income tax. But the account itself is not a taxable entity.

- General investment account (GIA): A GIA is a taxable investment account. Any income generated within the account, such as dividends or interest, may be subject to income tax. Furthermore, when an investment is sold for a profit, that profit may be subject to Capital Gains Tax. These taxes are a direct consequence of the investment activity within the GIA itself.

Summary table of differences:

| Feature | General Account (Accounting) | General Investment Account (GIA) |

|---|---|---|

| Primary Purpose | Record-keeping and financial reporting | Investing and generating a return |

| Nature | An internal classification category | An external account holding assets |

| Contains | A history of transactions | Financial assets (stocks, bonds, etc.) |

| Context | Business accounting (General Ledger) | Personal/Corporate finance |

| Tax Treatment | An internal tool used to calculate taxable profit | Investment returns are subject to income and capital gains tax |

A general account is a fundamental category within the general ledger used to organize financial transactions. These accounts are systematically divided into five main types - assets, liabilities, equity, revenue, and expenses - which together provide a complete picture of a company's financial health and performance. Recognizing that these internal bookkeeping tools are fundamentally different from an external General Investment Account (GIA) used for wealth-building is crucial for clear financial communication and decision-making.