Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Flotation cost is a critical financial concept that companies must carefully manage when issuing new securities to raise capital. These costs, incurred during the process of “floating” new stocks or bonds, directly affect the net funds a business receives and can significantly shape strategic financial decisions. For businesses seeking to expand operations or register a company in Vietnam, a thorough understanding of flotation costs is essential for accurate capital planning. This article explores flotation costs, calculation methods, and their substantial impact on financial strategies.

This article outlines the key aspects of flotation cost to help businesses and investors gain a clearer understanding. We specialize in company formation and do not provide financial or investment advisory services. For specific financial or legal matters, please consult a qualified advisor or relevant authority.

What is a flotation cost?

A flotation cost is the total expense incurred by a company when it issues new securities, such as stocks or bonds, to raise funds from investors. Think of it as the "entry fee" a company pays to access capital from the public markets. These costs are unavoidable and directly reduce the net proceeds - the actual amount of cash the company gets to keep and use from the offering.

When a company undertakes an Initial Public Offering (IPO) or a secondary offering, it enlists the help of various professionals to navigate the complex process. These costs arise from various professional services, such as investment banking, legal counsel, and accounting audits. For example, investment banks are hired to manage the sale of the securities, lawyers are needed to ensure compliance with regulatory bodies like the Securities and Exchange Commission (SEC), and auditors must verify the company's financial statements.

The significance of flotation costs lies in their direct impact on a company's cost of capital. The cost of capital is the return a company must generate on an investment to satisfy its investors. Because flotation costs reduce the usable funds from a securities issue, the company must earn a higher return on those funds to provide the same expected return to its investors. Consequently, understanding and accurately calculating these costs is a crucial component of corporate finance and strategic financial planning.

Types of flotation costs

Flotation costs have two primary categories: Direct costs and Indirect costs. Both types are critical to consider, as they collectively diminish the net proceeds from a securities issuance.

Flotation costs have two primary categories

Direct costs

Direct costs are the tangible, out-of-pocket expenses paid to third parties during the issuance process. These are the most visible and easily quantifiable expenses. The primary direct costs include a variety of out-of-pocket expenses, such as underwriting spreads, legal fees for drafting the prospectus, and SEC registration fees.

- Underwriting fees (spread): This is typically the largest component of direct costs, representing the compensation paid to investment banks for their role in selling the securities. The underwriter, or syndicate of underwriters, buys the securities from the company at a discount and sells them to the public at a higher price. The difference between the purchase price and the public offering price is known as the underwriting spread. For IPOs, this spread can range from 3.5% to 7% of the gross proceeds.

- Legal fees: Companies must hire experienced legal counsel to prepare and file the extensive documentation required by regulatory authorities. This includes drafting the prospectus, ensuring compliance with securities laws, and providing overall legal guidance throughout the issuance process.

- Accounting and audit fees: Public offerings require rigorous auditing of a company's financial statements by an independent accounting firm to ensure accuracy and transparency for potential investors. These fees cover the cost of the audit and the preparation of financial documents for the prospectus.

- Registration fees: Companies are required to pay fees to regulatory bodies like the SEC to register the new securities before they can be sold to the public.

- Printing and promotional costs: This category includes the costs of printing the prospectus, preparing marketing materials, and conducting "roadshows" where management presents to potential investors to generate interest in the offering.

Indirect costs

Indirect costs are less tangible and harder to quantify, but they can be just as significant as direct costs. These costs represent value that is lost or diverted as a result of the issuance process.

- Underpricing: This is often the largest indirect cost associated with an IPO. It occurs when the offering price of the new shares is set below their true market value. This is done intentionally to create strong initial demand and ensure the offering is fully subscribed, leading to a "pop" in the stock price on the first day of trading. While this benefits initial investors, it represents a significant opportunity cost for the issuing company, as it leaves potential capital on the table.

- Management time and effort: A securities issuance is an enormously time-consuming process for a company's senior management team. Executives, including the CEO and CFO, must dedicate hundreds of hours to meetings with underwriters, lawyers, and accountants, as well as participating in roadshows. This diverts their attention from running the core business, which can be a substantial, albeit hidden, cost.

- Market pressure costs (abnormal returns): The announcement of a new equity issuance can sometimes cause a temporary drop in the company's existing stock price. This happens because the new shares can dilute the ownership stake of existing shareholders, and the market may interpret the move as a sign that the company believes its stock is overvalued. This decline in share price represents a real cost to the company and its current investors.

Key components of flotation costs

To effectively plan for a securities offering, a company's financial leadership needs to have a clear checklist of the expenses they will encounter. This section summarizes the most critical components that make up the total flotation cost, reinforcing the key takeaways from the previous section. A CFO must anticipate and budget for these items to ensure the capital-raising process is smooth and the financial impact is fully understood.

- Underwriting fees: This is the primary fee paid to investment bankers for marketing and selling the new securities. It is the largest single direct expense and is calculated as a percentage of the total funds raised.

- Legal and compliance fees: These are payments to law firms for drafting the offering documents, such as the prospectus, and for ensuring the entire process adheres to strict regulatory compliance standards set by bodies like the SEC.

- Accounting and auditing costs: These fees are for the services of certified public accountants who must audit the company's financial statements to meet the disclosure requirements for a public offering.

- Regulatory fees (sec registration): This includes the fees paid directly to the SEC and other regulatory agencies for the official registration and filing of the new securities.

- Printing and distribution costs: These are the costs associated with producing and distributing the official prospectus and other promotional materials to potential investors.

- Underpricing of the issue: A significant indirect cost, especially in an IPO, where shares are intentionally sold for less than their anticipated market price to ensure a successful launch. This represents a substantial opportunity cost for the issuing company.

- Management time: A crucial but often overlooked indirect cost. The time senior executives spend on the offering process is time they are not spending on the company's core operations, representing a diversion of valuable resources.

How to calculate flotation costs

Accurately calculating flotation costs is essential for determining the net proceeds of a securities issue and for adjusting the company's cost of capital. There are two primary formulas used in this process: one calculates the flotation cost as a percentage, and the other integrates this cost into the valuation of new equity.

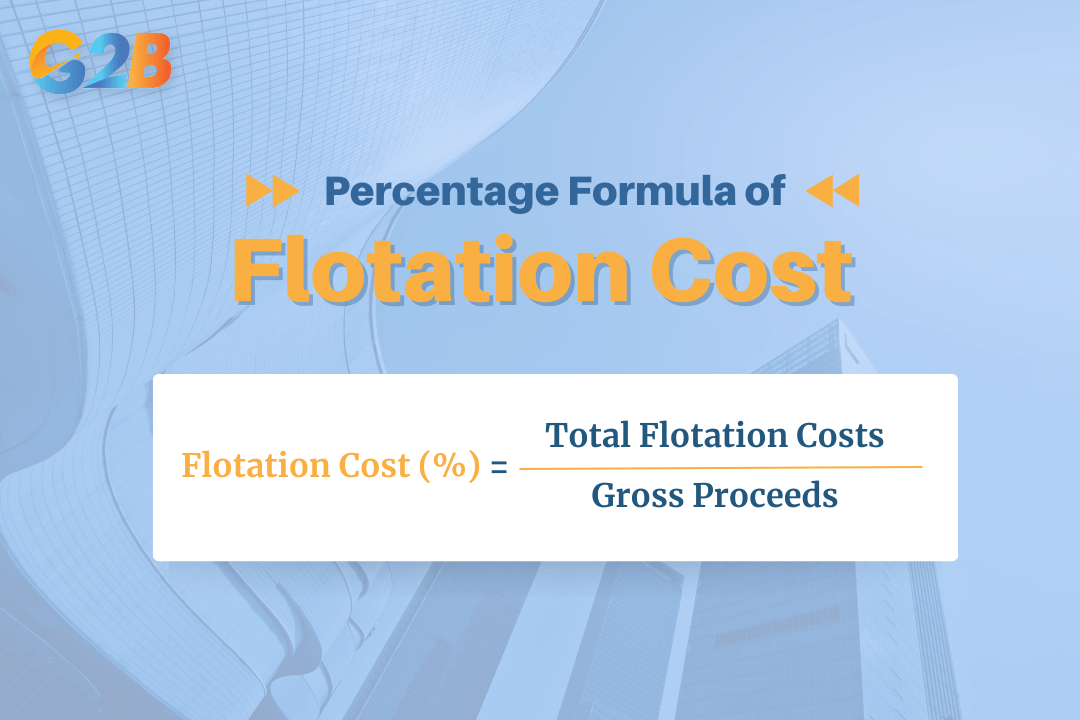

1. Flotation cost percentage formula

The most straightforward way to express flotation cost is as a percentage of the total or gross proceeds from the offering. This gives a clear picture of how much of the raised capital is consumed by issuance expenses.

The formula is: Flotation Cost (%) = Total Flotation Costs / Gross Proceeds

For example, imagine a company launches an IPO to raise $10 million in gross proceeds. The total direct and indirect expenses associated with this offering (underwriting fees, legal costs, etc.) amount to $500,000.

The calculation would be: Flotation Cost (%) = $500,000 / $10,000,000 = 0.05 or 5%

This means that for every dollar raised, 5 cents were spent on flotation costs, and the company received only 95 cents in net proceeds.

The flotation cost percentage formula

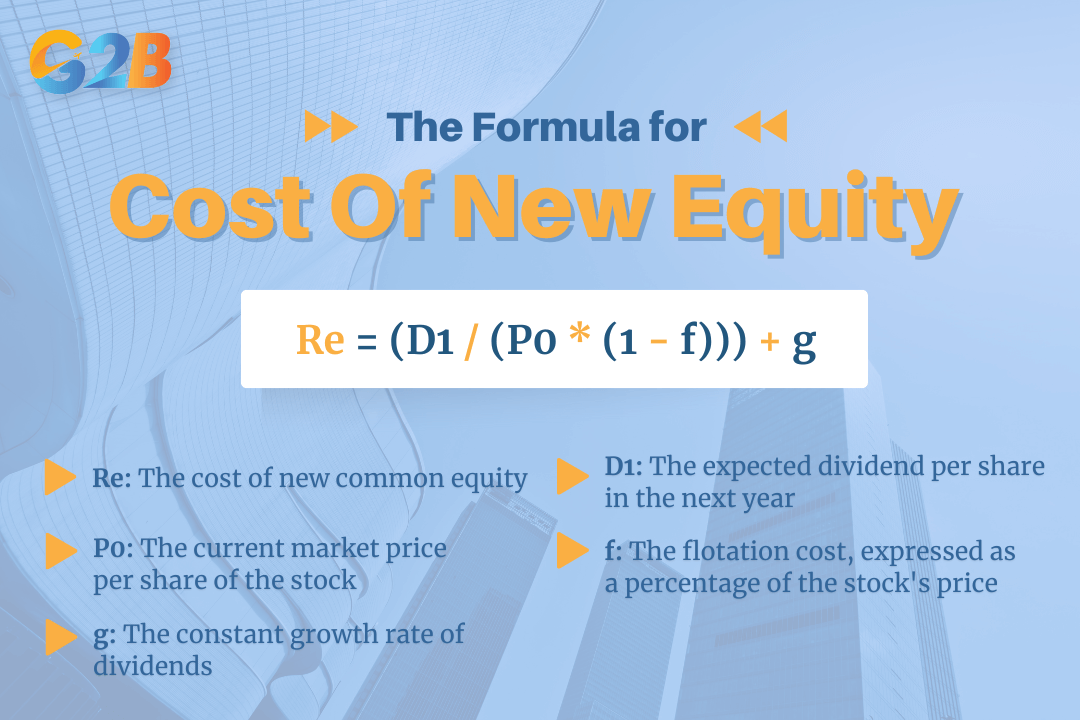

2. Cost of new equity with the dividend growth model

Flotation costs have a direct and significant impact on the cost of raising new equity capital. When a company issues new common stock, the funds it receives are reduced by these costs. To account for this, the widely used Dividend Growth Model (also known as the Gordon Growth Model) is adjusted. This adjusted formula shows that the cost of new external equity is higher than the cost of existing equity (or retained earnings) because of the presence of flotation costs.

The formula for the cost of new equity (Re) is: Re = (D1 / (P0 * (1 - f))) + g

Where:

- Re = The cost of new common equity

- D1 = The expected dividend per share in the next year

- P0 = The current market price per share of the stock

- f = The flotation cost, expressed as a percentage of the stock's price

- g = The constant growth rate of dividends

Let's illustrate with an example. A company's stock currently trades at $20 per share (P0). It just paid a dividend of $3.80, and dividends are expected to grow at 10% per year (g). The flotation cost (f) for a new stock issue is 5.5%. First, we calculate D1: D1 = $3.80 * (1 + 0.10) = $4.18.

Now, we can calculate the cost of new equity: Re = ($4.18 / ($20 * (1 - 0.055))) + 0.10 Re = ($4.18 / ($20 * 0.945)) + 0.10 Re = ($4.18 / $18.90) + 0.10 Re = 0.2212 + 0.10 = 0.3212 or 32.12%

If there were no flotation costs (f=0), the cost of equity would be 30.9%. The presence of flotation costs increases the company's cost of new equity, demonstrating the real financial burden these expenses create.

The formula for the cost of new equity (Re)

The impact of flotation cost on a company

Flotation costs are not merely transactional expenses; they have far-reaching strategic consequences that affect a company's financial structure, investment decisions, and ultimately, its value. Failing to account for flotation costs accurately leads to overestimated project returns and poor capital budgeting decisions.

Increased cost of capital

The most direct impact of flotation costs is an increase in the company's cost of capital. As shown in the calculation for the cost of new equity, flotation costs reduce the net proceeds from a stock issuance. This means the company has less capital to invest, yet it must still generate returns sufficient to satisfy investors who paid the full price for their shares. This effectively makes new capital more expensive. This higher cost of capital can lead to an increased Weighted Average Cost of Capital (WACC), which is the discount rate used to evaluate the profitability of future projects. A higher WACC means that fewer projects will meet the required rate of return, potentially causing the company to pass on otherwise viable investment opportunities.

Impact on financing decisions

Flotation costs play a significant role in a company's capital structure decisions - specifically, choosing between debt, equity, and internal financing (retained earnings). The costs for issuing common stock are generally the highest, often ranging from 2% to 8%, while the costs for issuing preferred stock or debt are typically lower. This cost differential encourages a "pecking order" for financing:

- Internal funds: Companies prefer to first use retained earnings for new projects because there are no flotation costs.

- Debt: If external capital is needed, debt is often the next choice due to its lower issuance costs and the tax-deductibility of interest payments.

- New equity: Issuing new common stock is typically the last resort because it incurs the highest flotation costs and can also dilute ownership for existing shareholders.

Reduction of net present value (NPV)

In capital budgeting, flotation costs must be accounted for to get a true measure of a project's profitability. A project's Net Present Value (NPV) is the present value of its future cash inflows minus the initial investment. Flotation costs make the initial investment higher, which in turn reduces the project's NPV. There are two common methods for handling flotation costs in NPV analysis, though one is strongly preferred by financial analysts:

- Adjusting the cost of capital (incorrect method): Some practitioners incorporate flotation costs by increasing the discount rate (WACC) used to evaluate the project's cash flows. However, this method is considered inaccurate because it penalizes the project's cash flows in perpetuity for a one-time expense. Flotation costs are incurred only at the beginning of the project, so treating them as an ongoing cost overstates their impact and can lead to the rejection of profitable projects.

- Treating as an initial cash outflow (correct method): The more theoretically sound and recommended approach is to treat the total flotation cost as part of the initial investment (the time-zero cash outflow). This accurately reflects the fact that these are one-time costs that reduce the project's initial value. For example, if a project requires a $50 million investment and the flotation costs to raise that capital are $2 million, the true initial cost for the NPV calculation is $52 million. This method correctly assesses the cost without distorting the project's long-term cost of capital.

Dilution of ownership

When a company issues new shares of stock, it increases the total number of shares outstanding. This means that the ownership stake of existing shareholders is diluted. While not a direct monetary cost, this dilution is a significant consideration for current owners and can impact corporate governance and control. The high costs associated with new equity issuance can exacerbate this issue, as the company receives less cash per share than what new investors pay, making the dilution less efficient from a capital-raising perspective.

Flotation cost is an unavoidable expense in the journey of raising capital through new securities. These costs, encompassing both direct out-of-pocket fees and more subtle indirect expenses, play a pivotal role in corporate finance. By understanding their various components - from underwriting fees to the opportunity cost of management's time - a company can better anticipate the true expense of floating a new stock or bond issue.