Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Fintech in Vietnam has evolved from a burgeoning trend into the backbone of the national digital economy as we enter early 2026. With a tech-savvy population, decisive government support, and a rapidly maturing regulatory framework, Vietnam has solidified its position as the "Rising Star" of ASEAN fintech. However, navigating this landscape requires more than just capital; it demands deep market intelligence, legal compliance, and strategic partnerships. This article serves as a roadmap to understanding the market data, legalities, and setup procedures for 2026.

This article provides an overview of Vietnam’s fintech market in 2026, highlighting key trends and opportunities for businesses and investors. We offer company formation in Vietnam and do not provide investment advisory services. For detailed market analysis or investment-related matters, please consult qualified financial or industry professionals.

Vietnam Fintech market overview 2026

As of early 2026, the Vietnamese fintech sector has transcended its initial "hype cycle" to reach a stage of robust utility and mass adoption. The country is no longer just "promising"; it is delivering substantial returns for early movers and offers strategic gaps for new entrants.

Market data and scale

The numbers speak definitively to the opportunity at hand. In 2026, the aggregate transaction value of the Vietnamese fintech market is projected to exceed $45 billion USD. This surge is driven by a unique confluence of demographic and technological factors:

- Smartphone penetration: Approximately 90% of the adult population now owns a smartphone, serving as the primary gateway for digital financial services.

- Internet connectivity: With the nationwide rollout of 5G in major cities like Ho Chi Minh City, Hanoi, and Da Nang, mobile internet speed facilitates seamless real-time transactions.

- Startup ecosystem: There are now over 400 active fintech startups operating in Vietnam, a significant increase from previous years, signaling a mature competitive landscape.

- Regulatory support: The State Bank of Vietnam's (SBV) Fintech Sandbox enables safe innovation for digital payments and lending.

The "cashless" consumer behavior

The government’s goal of a cashless society is nearing reality. The ubiquitous presence of VietQR - the national standard for QR payments - has revolutionized how money moves. From high-end shopping malls in District 1 to street food vendors in rural provinces, scanning a QR code is now as common as breathing.

Consumer trust has also shifted. In 2026, Vietnamese users are not just using apps for payments; they are comfortable using digital platforms for wealth management, insurance purchasing (Insurtech), and micro-investing.

Investment inflows 2025-2026

Venture Capital (VC) activity remains strong, though the focus has shifted. Investors are moving away from "growth at all costs" toward "sustainable profitability." Late-stage funding rounds are prioritizing companies with strong unit economics and clear paths to IPO. However, early-stage funding remains vibrant for niche solutions addressing the unbanked population in Tier 2 and Tier 3 cities.

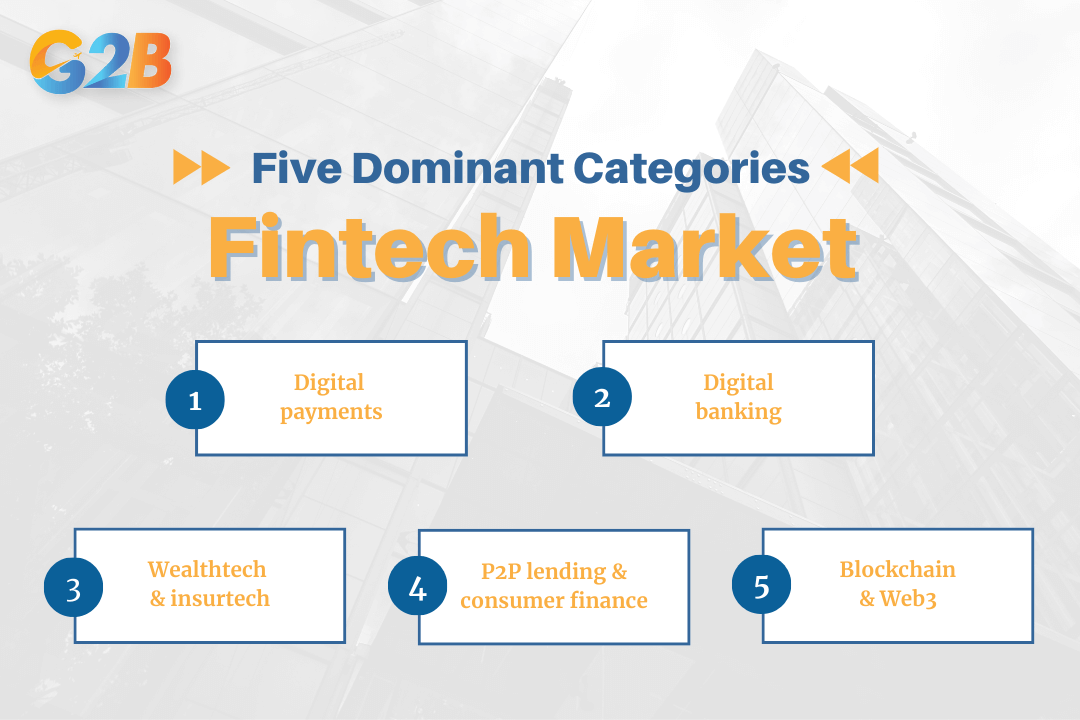

Key segments dominating the market

To succeed, investors must understand which pillars are holding up the ecosystem. The market is segmented into five dominant categories.

There are five dominant categories

1. Digital payments

This remains the largest segment by transaction volume. The "Super app" war has largely consolidated, with giants like MoMo, ZaloPay, VNPay and smaller such as Glodipay, ShopeePay, ViettelPay dominating the consumer space. However, the B2B payment space - specifically regarding cross-border payments and payroll solutions - remains an open battleground for new foreign players.

2. P2P lending and consumer finance

With a significant portion of the population still underbanked or lacking formal credit history, Peer-to-Peer (P2P) lending platforms fill a critical gap under SBV's regulatory sandbox trial (launched July 2025). These platforms utilize alternative data points to lend to Small and Medium Enterprises (SMEs) and individuals who are rejected by traditional banks.

3. Digital banking

Digital-only banks, often backed by traditional heavyweights, have gained massive traction among Gen Z and Millennials. Brands like Cake by VPBank and Timo have set the standard for frictionless user experience (UX), offering zero-fee accounts and high-interest savings directly via mobile apps.

4. Wealthtech & insurtech

As the Vietnamese middle class expands, so does the appetite for asset accumulation. Wealthtech apps allow users to invest small amounts (micro-investing) in stocks, bonds, or fund certificates. Similarly, Insurtech is disrupting the traditional agency model (fastest-growing at 31% CAGR to 2031) by offering bite-sized, on-demand insurance policies for travel, health, and motorbike accidents.

5. Blockchain and Web3

Despite strict regulations prohibiting crypto as a means of payment, Vietnam remains a global hub for blockchain development. The country consistently ranks in the top 3 globally for crypto adoption, driven by GameFi, NFTs, and DeFi protocols. Foreign investors often establish Blockchain Lab centers in Vietnam to leverage the high-quality, cost-effective developer talent pool.

Top 4 Fintech trends in Vietnam for 2026

Staying ahead in 2026 means aligning your business model with these four accelerating trends.

1. Embedded finance

Finance is no longer a destination; it is a feature. Non-financial platforms - such as e-commerce giants (Shopee, TikTok Shop) and ride-hailing apps (Grab, Be) - are integrating financial services directly into their user journeys. "Buy Now, Pay Later" (BNPL) is the standard checkout option, not an alternative.

2. AI & hyper-personalization

Artificial Intelligence is aggressively used for credit scoring and fraud detection. In 2026, lenders utilize machine learning algorithms to analyze thousands of data points - from telecom usage to social media behavior - to assess creditworthiness in seconds. This allows for hyper-personalized loan offers and investment advice tailored to individual risk profiles.

3. Biometric security & compliance

Following the State Bank of Vietnam's (SBV) mandates (specifically Decision 2345 implemented in 2024), biometric authentication is now mandatory for high-value transactions. Facial recognition and fingerprint scanning are standard integration requirements for any fintech app, reducing fraud and increasing user trust.

4. Green Fintech (ESG)

Aligned with Vietnam’s commitment to Net Zero by 2050, there is a rising trend in Green Fintech. Apps that track carbon footprints, offer green bonds, or incentivize eco-friendly spending behaviors are receiving preferential treatment from both consumers and government initiatives.

Legal framework & regulations

For foreign investors, this is the most critical section. Vietnam's legal environment is strict but increasingly transparent.

The regulators

The primary regulatory body is the State Bank of Vietnam (SBV). They control monetary policy and issue licenses for banking and intermediary payment services.

The Fintech sandbox mechanism

By early 2026, the long-awaited Fintech regulatory sandbox has entered a mature pilot phase. This mechanism allows startups to test new technologies (like P2P lending and API sharing) in a controlled environment before official laws are fully codified. Participation in the sandbox is often a prerequisite for operating in unregulated "grey" areas.

Intermediary payment service (IPS) license

To operate an e-wallet, payment gateway, or collection service, you must obtain an IPS License from the SBV.

- Conditions: Strict capital requirements (minimum 50 billion VND is standard for e-wallets), technical infrastructure audits, and personnel checks.

- Foreign ownership limit (FOL): While there is no hard legislative cap of 49% explicitly written in the Law on Credit Institutions for IPS specifically, the SBV exercises discretionary power. In practice, foreign investors typically enter via Joint Ventures or by acquiring stakes in existing licensed local entities to ensure smoother approval.

Decree 13: Personal data protection

Vietnam's Decree 13/2023/ND-CP on Personal Data Protection is in full force in 2026.

- Requirement: Fintech companies must appoint a Data Protection Officer (DPO) and conduct Data Protection Impact Assessments (DPIA).

- Cross-border transfer: Transferring user data outside Vietnam requires rigorous reporting to the Ministry of Public Security.

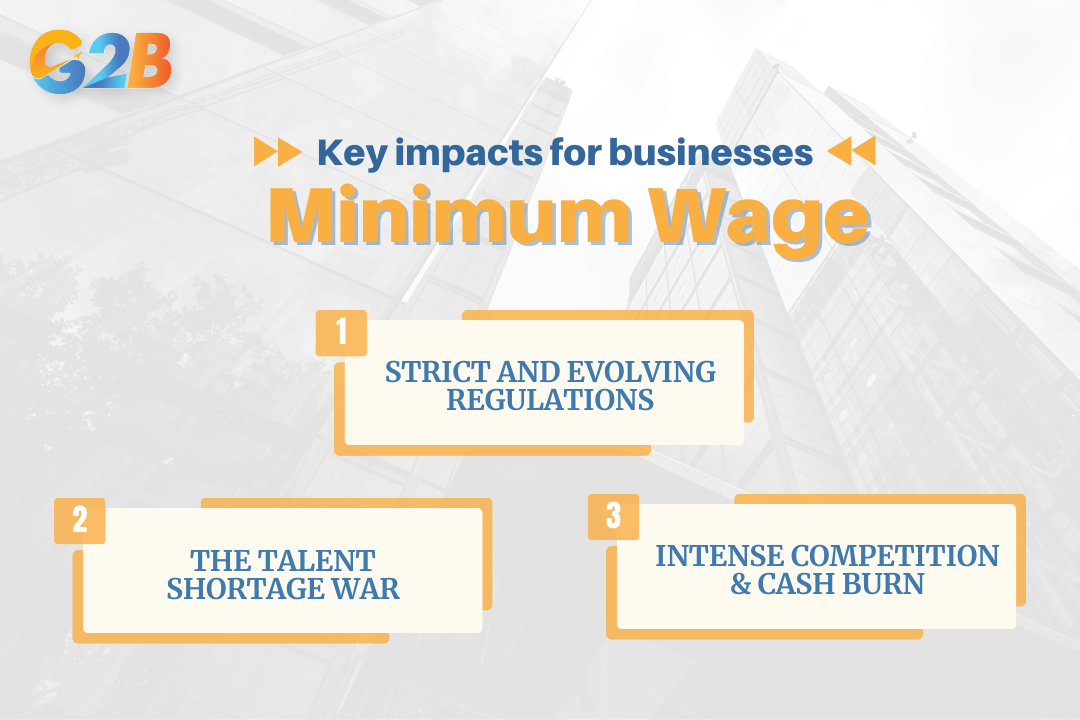

Challenges for foreign investors

While the potential is massive, the road is not without potholes. You must be prepared for the following hurdles.

Three main challenges for foreign investors

Strict and evolving regulations

The regulatory framework is playing catch-up with technology. Directives can change rapidly. For example, the definition of "digital assets" (including crypto) is now formally regulated under the 2025 Digital Technology Law. Investors must maintain constant dialogue with local legal counsels to ensure ongoing compliance.

The talent shortage war

While Vietnam has a surplus of junior developers, there is a severe shortage of C-level executives, product managers, and senior blockchain engineers who speak English fluently and possess global fintech experience.

- Solution: Many firms hire foreign experts (Expats) to fill these leadership roles while training local teams.

Intense competition & cash burn

The cost of customer acquisition (CAC) in Vietnam has risen. Users are "promo-sensitive," often switching apps based on which one offers the best voucher. Foreign entrants must be prepared for high initial "cash burn" rates to acquire market share against entrenched incumbents like MoMo or ZaloPay.

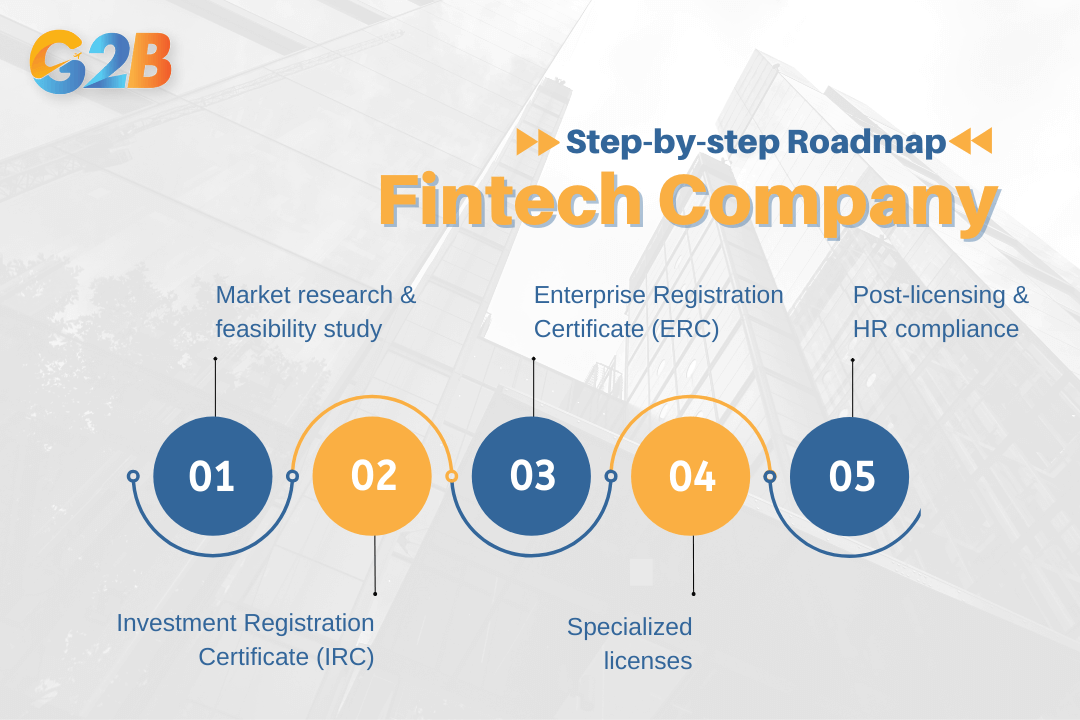

How to set up a Fintech company in Vietnam

Setting up a fintech entity requires a strategic approach. Here is the step-by-step roadmap for 2026.

Step 1: Market research & feasibility study

Before incorporating, validate your product-market fit. Are you targeting the banked or unbanked? Urban or rural?

Step 2: Investment Registration Certificate (IRC)

For foreign investors, the first legal document required is the Investment Registration Certificate. You must declare your project goals, location, and total investment capital. The Department of Planning and Investment (DPI) issues this.

Step 3: Enterprise Registration Certificate (ERC)

Once the IRC is obtained, you apply for the Enterprise Registration Certificate. This acts as your company's birth certificate and tax registration.

- Note: At this stage, you are a software or management consulting company. You are not yet a fintech payment provider.

Step 4: Specialized licenses

Depending on your business model, you must apply for sub-licenses:

- Payment services: Apply for the IPS license at the State Bank of Vietnam. This process can take 6–12 months.

- Lending/banking: Apply for participation in the Sandbox or partner with a local bank (Bank-as-a-Service model).

- Crypto/blockchain: Register as a software development firm; do not register as a financial exchange, as this is currently not licensable.

Step 5: Post-licensing & HR compliance

After licensing, you must handle:

- Tax registration: VAT, Corporate Income Tax (CIT).

- Bank account opening: Capital account for foreign investment.

- HR setup: Registering employees for Social Insurance, Health Insurance, and Unemployment Insurance.

The step-by-step roadmap for 2026

FAQs about the Vietnam Fintech market

As Vietnam’s fintech sector continues to expand, businesses and investors often have common questions regarding market entry, regulations, and growth potential. The following FAQs address key concerns to help readers gain a clearer understanding of the Vietnam fintech market.

Is Fintech legal in Vietnam?

Yes, fintech is legal and encouraged by the government. However, specific activities like Payment Intermediary Services (e-wallets, gateways) require a specific license from the State Bank of Vietnam. Cryptocurrencies are currently legal to hold but illegal to use as a means of payment.

What is the minimum capital requirement for a Fintech company?

For a standard tech software company, there is no fixed minimum, though $10,000–$20,000 USD is recommended for credibility. However, if you apply for an Intermediary Payment Service (IPS) license, the minimum charter capital requirement is generally 50 billion VND (approx. $2 million USD) for e-wallet providers.

Can foreigners own 100% of a Fintech company?

Foreigners can own 100% of a technology or software development company. However, for sensitive sectors like payment intermediaries, while 100% is theoretically possible under WTO commitments, the State Bank of Vietnam usually encourages Joint Ventures with local partners to ensure better regulatory control.

Do foreign tech experts need a work permit?

Yes, all foreign employees working in Vietnam for more than 3 months require a work permit. The penalties for non-compliance include deportation and heavy fines for the employer.

Vietnam’s fintech market in 2026 is poised for continued expansion, driven by strong digital adoption, a young and tech-savvy population, and ongoing government support for cashless payments and financial inclusion. As regulatory frameworks become more refined and competition intensifies, fintech companies will need to balance innovation with compliance, data security, and sustainable business models.