Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom For foreign investors and business owners establishing companies in Vietnam, understanding the role of a chief accountant in Vietnam is critical. Unlike in many Western jurisdictions where a "CFO" or "Financial Controller" suffices, the Vietnamese legal framework strictly dictates that companies must appoint a designated Chief Accountant who holds specific government-issued certifications. Failure to appoint this position - or appointing an unqualified individual - can lead to severe administrative penalties, frozen bank accounts, and the inability to submit valid tax declarations.

Legal requirements for chief accountants in Vietnam

Chief Accountant is a legal obligation codified in national law. Investors must understand the nuances of the Law on Accounting No. 88/2015/QH13 to ensure their corporate structure is compliant from day one.

Law on accounting Article 53

According to Article 53 of the Law on Accounting, all agencies and organizations utilizing state budget funds, as well as enterprises established and operating under Vietnamese law, are required to organize an accounting apparatus and appoint a Chief Accountant. This means that whether you are a Limited Liability Company (LLC) or a Joint Stock Company (JSC), the state expects a specific individual to be legally registered as the head of your accounting department. This individual acts as the primary liaison between your business and the General Department of Taxation.

12-month grace period

Recognizing the difficulties startups face in finding qualified personnel immediately, the law offers a temporary reprieve. Upon establishment, a company may appoint a "Person in Charge of Accounting" instead of a formal Chief Accountant. However, this is a time-limited exemption.

Enterprises must appoint a formal Chief Accountant within 12 months from the date of establishment. If a qualified Chief Accountant cannot be found immediately, the person in charge of accounting can serve in this interim capacity, but they must still meet specific academic and ethical standards.

Micro-enterprise exemptions

There is a notable exception to this rule designed to reduce the burden on very small businesses. According to the guidance on micro-enterprises, companies that meet specific revenue or labor criteria (typically having fewer than 10 employees and low annual revenue) are exempted from the mandatory appointment of a Chief Accountant.

Key roles and statutory responsibilities

The Chief Accountant in Vietnam wields significant power and carries substantial liability. Their role extends far beyond bookkeeping; they are the gatekeepers of financial legality.

Role of chief accountant vs. legal representative

It is vital to distinguish between these two key roles.

- The legal representative (General director): Bears the ultimate legal responsibility for the company's operations, including financial truthfulness. If tax evasion occurs, the Legal Representative is the primary individual held accountable by the law.

- The chief accountant: Is responsible for the compliance and accuracy of the accounting records. They operate under the direction of the Legal Representative but have the statutory right and duty to refuse instructions that violate accounting regulations.

If a Legal Representative orders a fraudulent transaction, the Chief Accountant must legally refuse and report it. If they proceed with the transaction, they become jointly liable for the violation.

It is vital to distinguish between these two key roles

Signing authority and financial statements

A company’s financial documents are not considered valid by the Ministry of Finance (MoF) or tax authorities without the Chief Accountant's signature. The Chief Accountant must sign essential documents, including:

- Annual financial statements.

- Value added tax (VAT) declarations and Corporate income tax (CIT) finalizations.

- Payment vouchers and bank transfer orders.

- Documents regarding the liquidation of assets.

This signing authority is a key requirement when opening a bank account in Vietnam, as banks need to register the chief accountant's specimen signature for all corporate transactions

Banks in Vietnam will strictly reject any payment order that lacks the registered Chief Accountant’s signature if the company constitutes a structure requiring one.

Compliance with Vietnamese accounting standards (VAS)

Vietnam currently utilizes the Vietnamese Accounting Standards (VAS), which differs significantly from International Financial Reporting Standards (IFRS). The Chief Accountant must ensure all ledgers, the chart of accounts, and financial reports comply strictly with VAS.

This includes specific rules on revenue recognition, asset depreciation, and the usage of the mandatory Vietnamese Chart of Accounts (Circular 200 or Circular 133). A foreign CFO may understand GAAP or IFRS, but without deep knowledge of VAS, they cannot legally fulfill the statutory duties of a Chief Accountant in Vietnam.

Mandatory qualifications and appointment criteria

You cannot simply promote a senior accountant to this role. The Ministry of Finance imposes strict barriers to entry to ensure professional quality.

Academic and experience requirements

To be appointed, a candidate must possess a Bachelor’s degree in accounting, auditing, or finance. Furthermore, they must demonstrate actual work experience in accounting:

- At least 02 years of experience for those with a university degree.

- At least 03 years of experience for those with an intermediate or college degree.

Chief accountant certificate (certificate of foster training)

This is the most critical requirement often overlooked by foreign investors. A degree is not enough. The candidate must hold a valid Chief Accountant Certificate issued by the Ministry of Finance or a recognized training institution.

To obtain this, accountants must undergo a specific training course ("Foster Training") and pass an examination. International certificates such as ACCA, CPA Australia, or CIMA are not automatic substitutes. Holders of international certificates must still undergo a simplified conversion exam or obtain the specific local certification to be legally recognized as a Chief Accountant on tax registration forms.

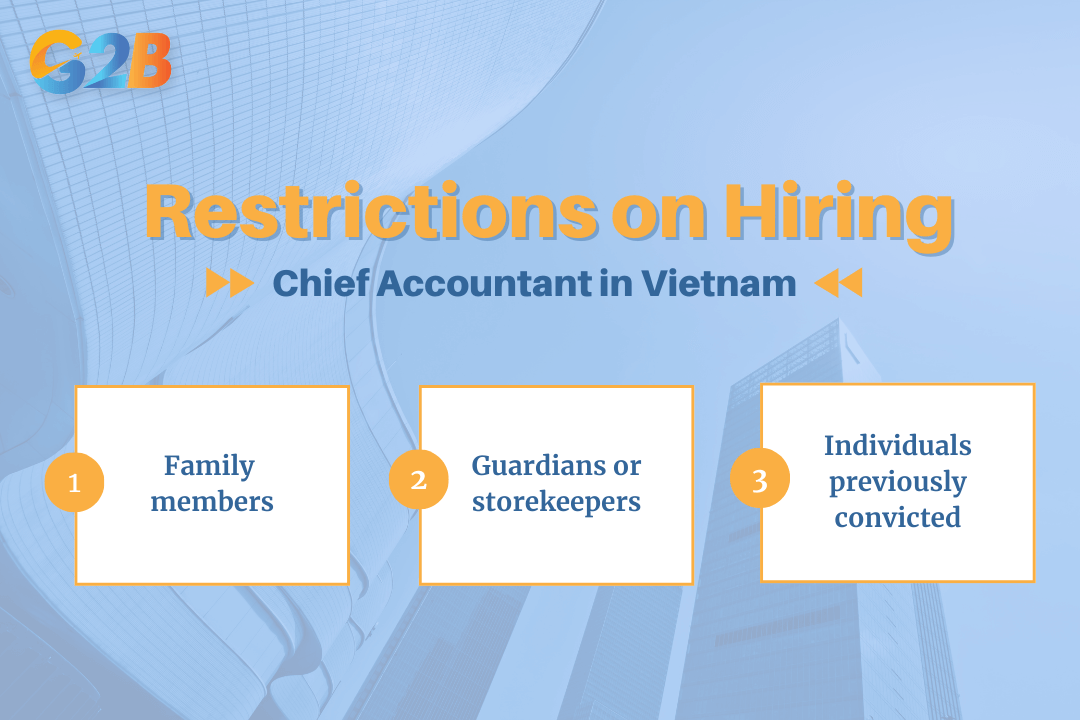

Restrictions on hiring

The law explicitly prohibits certain individuals from holding this position to prevent conflicts of interest and ensure integrity. You cannot appoint:

- Family members (parents, spouses, children, siblings) of the Legal Representative, General Director, or owner of the company.

- Guardians or storekeepers responsible for warehousing or treasury assets (to prevent theft and cover-ups).

- Individuals previously convicted of economic crimes or accounting violations who have not had their criminal records cleared.

03 Restrictions on hiring a chief accountant in Vietnam

Choosing between in-house and outsourced services

For Foreign Direct Investment (FDI) companies and SMEs, the decision to hire in-house or outsource is pivotal for cost management and compliance.

Benefits of hiring in-house

An in-house Chief Accountant is suitable for large-scale enterprises, manufacturing plants, or companies with high transaction volumes.

- Pros: Immediate availability, deep understanding of daily operations, and tighter control over internal cash flow.

- Cons: High salary costs, compulsory insurance/benefits, and the difficulty of verifying if the individual truly understands the ever-changing tax laws.

Benefits of outsourced nominee chief accountants

For the majority of market entrants, representative offices, and SMEs, outsourcing is the superior strategy.

| Feature | In-house chief accountant | Outsourced |

|---|---|---|

| Cost | High ($1,500 - $3,000/month) | Low (Fixed monthly retainer) |

| Staffing Stability | Risk of turnover/resignation | Guaranteed continuity |

| Expertise | Limited to one person's knowledge | Access to a team of experts |

| Liability | Company bears full employment risk | Service provider bears professional liability |

Outsourcing allows investors to satisfy the "Article 53" legal requirement immediately while ensuring that tax reports are reviewed by experts who are updated daily on circulars from the General Department of Taxation.

Outsourcing this role is often part of a broader financial structure optimization for foreign-invested enterprises

Salary benchmarks and cost expectations for 2026

As we approach 2026, the demand for bilingual, high-level accountants in Vietnam is driving salaries upward. Inflation and the gradual shift toward IFRS are also impacting compensation.

Full-time salary ranges

If you choose to hire internally, you must budget for the following gross monthly salaries (excluding bonuses and 23.5% mandatory social insurance contributions):

- Junior Chief Accountant (SMEs): 25,000,000 VND – 40,000,000 VND ($1,000 – $1,600).

- Experienced Chief Accountant (Large Local Corp): 45,000,000 VND – 70,000,000 VND ($1,800 – $2,800).

- CFO / Chief Accountant (MNCs/FDI): 80,000,000 VND – 120,000,000 VND+ ($3,200 – $5,000+).

Note: Salaries in Ho Chi Minh City are typically 10-15% higher than in Hanoi due to the higher cost of living and competition for talent.

Outsourcing fees

In contrast, outsourcing fees remain highly cost-effective. A "Chief Accountant Service" (which includes the Named Chief Accountant and review of books) typically ranges from $200 to $600 USD per month, depending on the volume of invoices and complexity of the business model. This represents a savings of over 80% compared to a full-time hire.

Penalties for non-compliance

The Vietnamese government is strict regarding accounting oversight. Ignoring these regulations results in immediate financial and operational consequences.

Administrative fines

Under Decree 41/2018/ND-CP, the government outlines specific penalties for accounting violations.

- Fines ranging from 10,000,000 VND to 20,000,000 VND are applied for failing to appoint a Chief Accountant or appointing one who does not meet legal standards.

- Fines ranging from 5,000,000 VND to 10,000,000 VND are applied for failing to notify the tax authority of the Chief Accountant’s appointment or change in personnel.

Operational risks

The administrative fine is often the least of the investor's worries. The operational risks are far more damaging:

- Tax finalization rejection: The Tax Department may reject your annual CIT finalization if the signatory is not a legally registered Chief Accountant.

- Frozen bank accounts: Banks are legally required to verify the Chief Accountant’s status. Discrepancies can lead to the freezing of corporate accounts, halting all outgoing payments.

- VAT refund denial: Companies claiming VAT refunds must have compliant accounting books signed by a certified Chief Accountant. Without this, refunds are denied.

To avoid these risks, investors should strictly follow the company setup process and requirements in Vietnam, which include early tax registration and accountant appointment

Transition from VAS to IFRS

Vietnam is currently in a transitional phase that will reshape the accounting landscape significantly by 2026.

Roadmap to 2026 and beyond

The Ministry of Finance has approved a roadmap to apply International Financial Reporting Standards (IFRS) in Vietnam.

- Phase 1 (2022-2025): Voluntary application for consolidated financial statements by specific FDI companies and large listed corporations.

- Phase 2 (Post-2025): Wider mandatory application is expected.

Impact on the chief accountant role

This transition means the modern Chief Accountant in Vietnam must evolve from a simple "compliance bookkeeper" into a strategic financial analyst. They will need to manage dual reporting systems (VAS for tax authorities and IFRS for foreign parent companies).

Frequently asked questions about chief accountants

Here are the most common questions from foreign investors about chief accountants when running a business in Vietnam.

Is a chief accountant mandatory for a representative office?

No, an RO is one of several types of company in Vietnam that have simplified accounting requirements as they do not generate profit.

Can a foreigner serve as a chief accountant in Vietnam?

Yes, but it is difficult. A foreigner can hold the title, but they must possess the Vietnamese Chief Accountant Certificate and typically need to be fluent in Vietnamese to handle the statutory paperwork and interface with tax officials. In practice, most foreign companies hire a Vietnamese Chief Accountant or use a nominee service to satisfy the legal requirement, while a Foreign Finance Manager handles internal strategy. Furthermore, a foreign accountant will still need a valid work permit to be legally employed in this position in Vietnam.

Can the general director also hold the chief accountant position?

Absolutely not. The Law on Accounting explicitly forbids the Legal Representative (General Director) from concurrently holding the Chief Accountant position. This is to ensure a separation of duties and prevent unchecked financial misconduct.

Do I need a chief accountant immediately upon licensing?

You have a 12-month grace period to appoint a formal Chief Accountant. During this time, you can appoint a "Person in Charge of Accounting." However, for tax registration purposes, it is highly recommended to settle this role within the first 30 days to ensure smooth banking and tax setup.

The Chief Accountant in Vietnam is a linchpin of corporate compliance. They are the shield that protects your business from tax penalties and the bridge that connects your financial performance to the state authorities. Whether you are a startup utilizing the 12-month grace period or an established FDI enterprise navigating the shift to IFRS, compliance with Article 53 of the Law on Accounting is non-negotiable.