Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Guarantor is a legal and financial term referring to an individual or corporate entity that pledges to fulfill the obligations of a borrower if that borrower fails to meet their repayment terms. Acting as a financial safety net, the guarantor provides a secondary layer of security to lenders, significantly reducing the risk associated with lending capital to individuals or businesses with insufficient credit history or collateral.

This article outlines the key concepts of a guarantor and how guarantees function in legal and financial arrangements. We specialize in company formation in Vietnam and not provide financial guarantee services or credit advisory. For guidance on drafting or evaluating guarantee agreements, please consult a qualified legal or financial expert.

What is a guarantor?

A guarantor is a third party in a lending arrangement who agrees to assume secondary liability for a debt or obligation that arises only if the principal debtor defaults. This creates a tripartite legal relationship involving three distinct entities: The Creditor (lender), the Principal (borrower), and the Guarantor. The legal instrument that binds the guarantor is known as the Guarantee Deed or a separate guarantee contract. Unlike the loan agreement which establishes the terms between the borrower and the lender, the Guarantee Deed is a separate legal instrument that specifically sets out the guarantor’s obligations to the creditor.

Responsibilities and obligations of a guarantor

The responsibilities of a guarantor extend far beyond simply covering missed monthly payments. When you sign a guarantee, you are agreeing to a comprehensive set of financial and legal obligations that can persist for years.

Responsibilities and obligations of a guarantor

1. Financial liability scope

The guarantor is liable for the principal debt, accrued interest, default penalties, and legally incurred collection costs such as legal fees and court expenses. If the borrower defaults, the lender is legally entitled to demand payment for the entire outstanding balance, not just the arrears. This often includes:

- Outstanding principal: The core amount of money borrowed that remains unpaid.

- Compound interest: Interest that accumulates on the unpaid debt, often at a higher "default rate."

- Collection costs: Legal fees, court costs, and administrative charges incurred by the lender while attempting to recover the debt.

2. Duration and revocation

A common misconception is that a guarantor can withdraw their support at any time. In reality, a guarantee is usually binding until the loan is fully discharged.

- Fixed-term loans: The liability remains until the final payment is made.

- Revocation notice: Some guarantees allow the guarantor to provide a notice of discontinuance. However, this only affects future obligations after the notice becomes effective and usually freezes liability at the current outstanding amount; it does not erase past obligations. The lender may then demand immediate repayment of that frozen amount from the borrower or the guarantor.

3. Continuing guarantees

In business banking, particularly with overdrafts or lines of credit, guarantees are often structured as "Continuing guarantees." This means the guarantee covers not just a specific loan, but all current and future debts the borrower incurs with that lender. Even if the borrower pays the balance to zero, if they borrow again later under the same facility, the guarantor remains liable unless they have formally and successfully revoked the guarantee in writing.

The scope of "unlimited" vs. "limited" liability

One of the most critical negotiation points in a Guarantee Deed is defining the extent of the liability.

Unlimited liability (All monies guarantee)

An "all monies" guarantee exposes the guarantor to unlimited risk. Under this arrangement, the guarantor is responsible for all debts the borrower owes to the lender, now and in the future. This includes credit cards, overdrafts, and business loans that the guarantor may not even be aware of.

- Risk profile: Extremely high.

- Asset exposure: The lender can pursue all of the guarantor’s personal assets, including their home, savings, and investments, to satisfy the debt.

Because the risk of losing personal wealth is significant, understanding asset protection strategies is crucial before agreeing to unlimited liability. Proper planning can help safeguard essential properties and investments from being seized in the event of a borrower's default.

Limited liability

A limited guarantee caps the guarantor's exposure to a specific amount or a specific transaction.

- Financial caps: The guarantee is limited to a fixed sum (e.g., "Limited to $50,000 plus interest and costs"). Once the guarantor pays this amount, their obligation is discharged, regardless of the remaining debt.

- Time limits: The guarantee is valid only for a specific period (e.g., "Valid for the first 5 years of the mortgage").

- Specific transaction: The guarantee applies strictly to Loan Reference Number X and does not extend to other debts the borrower holds with the bank.

Role of the guarantor when a subsidiary in Vietnam borrows

Navigating corporate finance in Vietnam requires a deep understanding of local regulations. When a foreign parent company acts as a guarantor for its Vietnamese subsidiary, or when a local director guarantees a corporate loan, specific legal frameworks apply.

Civil Code 2015: Article 335

The legal basis for guarantees in Vietnam is codified in Article 335 of the Civil Code 2015. It defines a guarantee as an undertaking by a third party (the guarantor) to the obligee (the creditor) to perform an obligation on behalf of the obligor (the principal) if the obligor fails to perform.

- Scope: The parties can agree that the guarantor is liable only when the obligor is incapable of performing, or liable immediately upon the obligor's failure to perform on time.

- Consent: A guarantee requires the written consent of the guarantor but does not necessarily require the consent of the borrower (though practically, the borrower is involved).

Foreign parent companies and offshore guarantees

For multinational corporations operating in Vietnam, a common scenario involves a foreign parent company providing a Corporate Guarantee for a loan taken by its Vietnamese subsidiary from a local or foreign bank. This is particularly common when the parent entity is structured as an offshore company looking to support its local operations without directly injecting more capital.

- SBV Registration: If the foreign parent company (Guarantor) is called upon to fulfill the guarantee obligation, the payment they make on behalf of the Vietnamese subsidiary is effectively converted into a debt owed by the subsidiary to the parent company. This transaction transforms into a foreign loan.

- Regulatory Compliance: Under regulations by the State Bank of Vietnam (SBV), specifically regarding foreign exchange management, this new "loan" may require registration with the SBV if the repayment term exceeds 12 months. Failure to anticipate this conversion can lead to administrative penalties and difficulties in repatriating funds later.

Corporate authority

When a Vietnamese company acts as a guarantor for another entity, strict adherence to the Law on Enterprises is required. The decision to provide a guarantee must be approved by the Board of Members or the General Meeting of Shareholders, depending on the value of the guarantee relative to the company’s total assets. Unauthorized guarantees signed by a director without proper corporate resolutions can be declared invalid by the courts.

To ensure validity, all corporate guarantees must align with the company's Articles of Association. This constitutional document outlines the internal rules and power limits of the directors, specifying who has the authority to sign guarantees and what approval thresholds are required to prevent legal disputes.

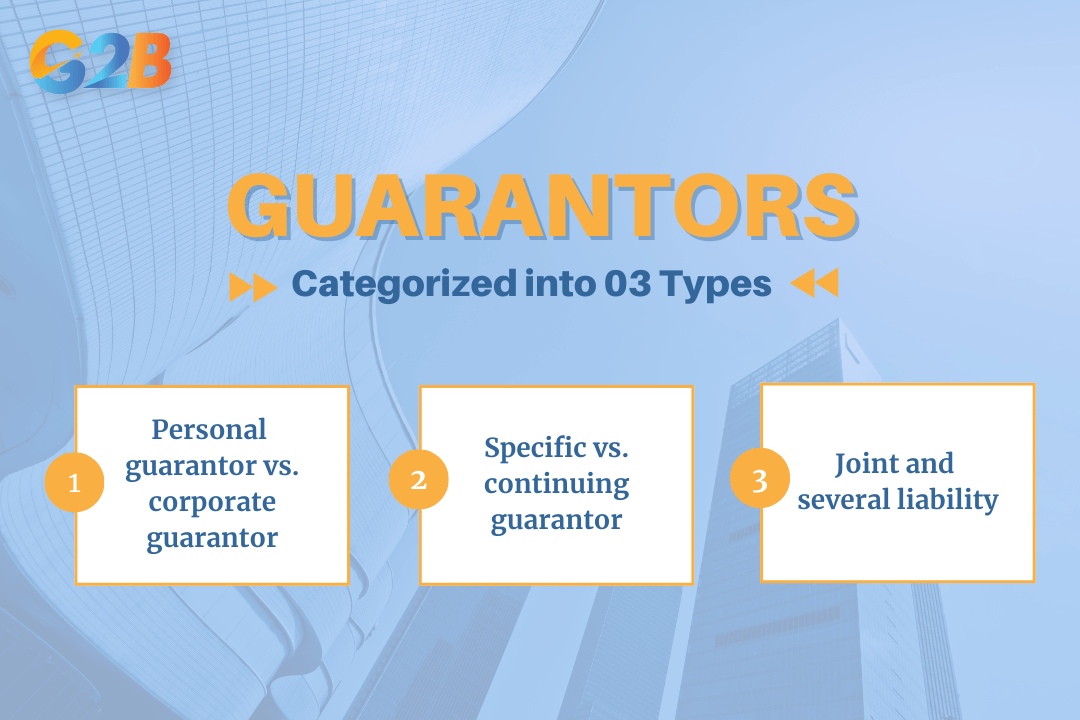

Types of guarantors

The financial world categorizes guarantors based on the entity type and the nature of the liability assumed. Understanding these distinctions helps in selecting the right structure for your needs.

The financial world categorizes guarantors based on the entity type

1. Personal guarantor vs. corporate guarantor

- Personal guarantor: An individual, often a company director or family member, pledges their personal wealth. This puts personal assets like the family home and private savings at risk.

- Corporate guarantor: A company pledges its assets to cover the debt of another company. This is often seen in complex corporate structures where a holding company provides a guarantee for its subsidiaries to secure better lending terms.

It is important to distinguish the role of a "corporate guarantor" from a guarantee company (Company Limited by Guarantee). While a corporate guarantor is a standard business entity acting as a surety, a "Guarantee Company" is a specific legal structure often used for non-profits where members' liability is limited to a nominal amount guaranteed in the memorandum, rather than shares held.

2. Specific vs. continuing guarantor

- Specific performance: The guarantee is tied to a single, isolated obligation (e.g., a performance bond for a construction project).

- Continuing guarantee: As mentioned, this covers a running balance or series of transactions, common in trade finance and revolving credit facilities.

3. Joint and several liability

This is a critical legal concept. If there are multiple guarantors (e.g., three directors of a company), the bank usually insists on "Joint and Several Liability".

- Implication: The bank is not required to sue all guarantors equally. They can choose to pursue the wealthiest guarantor for 100% of the debt. That guarantor must then try to recover the shares from the other co-guarantors privately. You are not just liable for your "share"; you are liable for the whole amount.

Guarantor vs. co-signer: Critical differences

While both guarantors and co-signers agree to take responsibility for a loan, their legal standing and the timing of their liability differ significantly. Confusing these terms can lead to unexpected financial exposure.

1. Liability timing

- Co-signer (Primary liability): A co-signer is treated exactly like the primary borrower. They are responsible for the loan from day one. If the primary borrower misses a payment, the co-signer is immediately delinquent.

- Guarantor (Secondary liability): A guarantor is typically only liable after the lender has formally declared the borrower in default and made a demand for payment.

2. Ownership rights

- Co-signer: usually has ownership rights to the asset being purchased. For example, if you co-sign a car loan, your name frequently appears on the vehicle's title.

- Guarantor: typically has no ownership rights or claim to the asset. They carry the burden of the debt without the benefit of the property.

3. Credit score impact

- Co-signer: The loan appears on the co-signer’s credit report immediately as an active debt. It affects their debt-to-income ratio instantly.

- Guarantor: In many jurisdictions, the potential debt does not appear on the guarantor's credit report as an active liability unless the borrower defaults. However, the inquiry (credit check) will be visible.

Requirements to become a guarantor

Lenders act with caution. Not everyone qualifies to be a guarantor. The bank essentially underwrites the guarantor just as strictly as the borrower. To be accepted, you must meet stringent criteria demonstrating financial solidity.

Requirements to become a guarantor

1. Superior credit score

A guarantor must possess an excellent credit rating. Lenders are looking for a history of timely payments and responsible credit management. A guarantor with a history of defaults or low credit scores provides no additional security to the bank.

2. Income and debt service coverage ratio (DSCR)

The lender will assess the guarantor's Debt Service Coverage Ratio. This metric calculates whether the guarantor has enough cash flow to cover their own living expenses/debts plus the new loan payment if the borrower fails.

- Verification: Proof of income via tax returns, pay slips, or audited financial statements (for corporate guarantors) is mandatory.

3. Asset verification and liquidity

While income is important, collateral is king. Lenders prefer guarantors with tangible assets - real estate, term deposits, or marketable securities - that can be easily liquidated.

- Equity check: If you are guaranteeing a mortgage using your own home as security, you must have sufficient equity (the difference between your home's value and what you owe on it).

4. Legal age and residency

The guarantor must be of legal age (18+ in Vietnam and most jurisdictions) and possess full civil capacity. Residency status is also a factor; banks are often reluctant to accept overseas guarantors due to the legal complexity of enforcing cross-border judgments.

Risks associated with being a guarantor

We emphasize that becoming a guarantor is a high-stakes decision. The risks are multifaceted, affecting your financial health, legal standing, and personal relationships.

1. Impact on personal credit rating

If the borrower misses payments and the lender pursues the guarantee, it acts as a negative mark on the guarantor’s credit history. A default by the borrower can cause a precipitous drop in the guarantor’s credit score, making it difficult for the guarantor to obtain loans, credit cards, or mortgages for themselves in the future.

2. Asset seizure and bankruptcy

In a worst-case scenario, if the guarantor cannot pay the debt they guaranteed, the lender can obtain a court order or enforcement judgment to seize and sell the guarantor’s assets. This can lead to the loss of the family home or forced liquidation of business assets, potentially resulting in personal bankruptcy.

3. The "shadow debt" effect

Even if the borrower is paying on time, the contingent liability sits on the guarantor’s financial profile as "Shadow Debt." When the guarantor applies for their own loan, lenders will treat the guaranteed amount as a potential monthly obligation in debt-to-income calculations. This increases the guarantor’s theoretical debt-to-income ratio, drastically reducing their borrowing capacity.

4. Relationship risks

Money is a leading cause of conflict. If a friend or family member defaults, the guarantor is left with the bill. This creates immense resentment and typically destroys the relationship. In a business context, calling on a director’s guarantee often signals the end of the professional relationship and can lead to acrimonious litigation between partners.

5. Limited control

Once the guarantee is signed, the guarantor often has limited visibility or control over how the borrower manages their finances. The borrower might take on additional risks or mismanage the business, increasing the likelihood of default, while the guarantor remains powerless to intervene until it is too late.

The role of a guarantor is a cornerstone of modern finance, enabling business funding and personal asset acquisition that might otherwise be impossible. However, it is a role defined by asymmetric risk: The guarantor assumes 100% of the liability often with 0% of the benefit. Whether dealing with the nuances of Article 335 of the Civil Code 2015 in Vietnam or navigating complex international joint and several liability clauses, knowledge is your only defense. Before signing a Guarantee Deed, it is imperative to conduct due diligence on the borrower and negotiate terms that limit your exposure. Do not rely on verbal assurances; ensure every limitation is codified in the contract.