Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Two of the most common business structure options are Limited Liability Companies (LLCs) and Sole Proprietorships. While both offer unique advantages, they also come with distinct legal, financial, and operational implications. This guide breaks down the key differences, pros, and cons of each to help you determine between an LLC or a sole proprietorship - which structure best suits your business goals.

Why compare LLC vs. sole proprietorship?

Understanding the differences between a Limited Liability Company (LLC) and a Sole Proprietorship can help business owners make an informed decision that aligns with their goals, risk tolerance, and financial strategies.

Common reasons entrepreneurs choose between LLC and sole proprietorship

Many business owners start as sole proprietors due to the simplicity and low cost of formation. However, as businesses grow, concerns about liability and taxation often lead them to consider an LLC. Below are some key scenarios that influence this decision:

- Freelancers and consultants: A sole proprietorship is an easy entry point for freelancers, such as graphic designers or writers. They may later transition to an LLC when they start hiring employees or working with larger clients who prefer contracts with an incorporated business.

- E-commerce and retail business owners: Dropshipping or online store owners often start as sole proprietors due to minimal upfront costs. However, an LLC becomes attractive when they want liability protection against product liability claims or potential lawsuits.

- Service-based businesses: Personal trainers, photographers, and financial consultants may initially operate as sole proprietors. As their clientele grows, they often switch to an LLC to project a more professional image and separate personal and business finances.

- Side hustlers and small startups: Many individuals testing a business idea begin as sole proprietors. If the business proves successful, transitioning to an LLC can offer credibility, asset protection, and better tax flexibility.

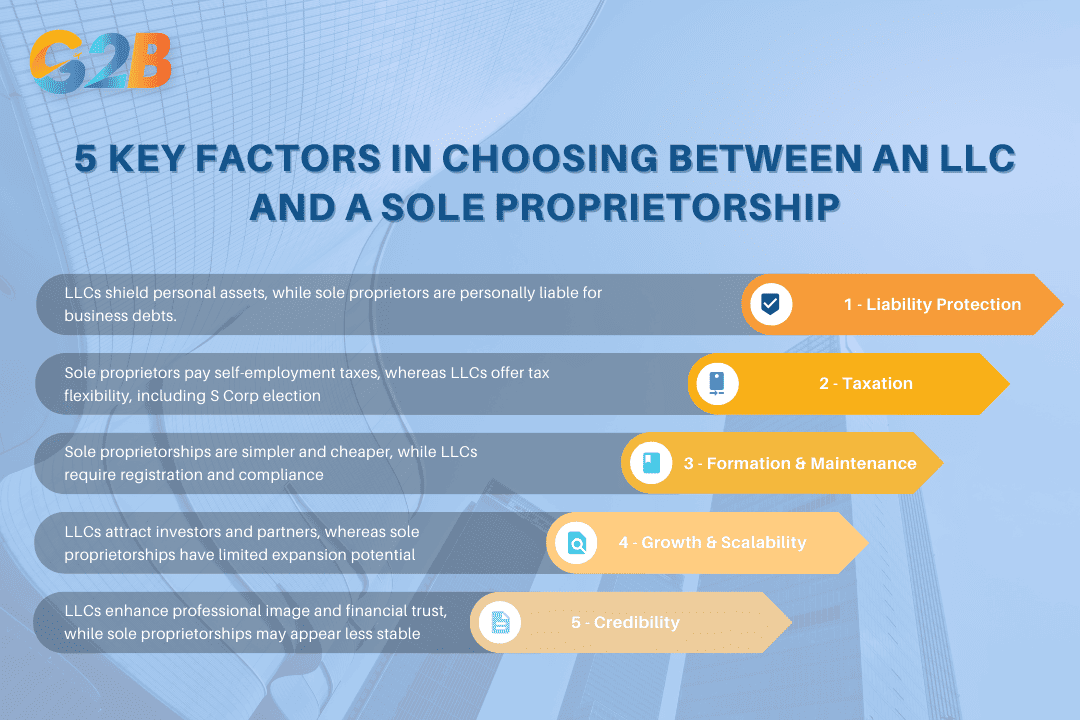

5 key factors that influence the decision

When deciding between an LLC and a sole proprietorship, business owners must evaluate multiple factors, including liability risks, taxation, regulatory requirements, and long-term scalability.

1. Liability protection

- LLC: Provides a legal separation between the business and its owner(s), protecting personal assets (e.g., house, savings) from business debts and lawsuits.

- Sole proprietorship: The owner is personally liable for all business debts and legal claims, meaning creditors can seize personal assets if the business cannot cover its obligations.

2. Taxation considerations

- Sole proprietorship: Business income is reported on the owner’s personal tax return and subject to self-employment taxes (Social Security and Medicare).

- LLC: Has tax flexibility - it can be taxed as a sole proprietorship, partnership, or elect to be taxed as an S Corporation or C Corporation, potentially reducing tax liability.

3. Formation and maintenance

- Sole proprietorship: Simple and cost-effective, with minimal paperwork required to start and operate.

- LLC: Requires formal registration, filing of Articles of Organization, and adherence to state compliance rules (e.g., annual reports, fees).

Whether it's an LLC or Sole Proprietorship, if you are looking for a partner to incorporate in Delaware, you can trust and contact G2B for the best advice throughout the journey from the start to when your company is operating

4. Business growth and scalability

- LLC: More attractive to investors, partners, and lenders due to its structured business framework.

- Sole Proprietorship: Limited scalability since ownership is tied directly to the individual and cannot be transferred.

5. Credibility and professional image

- LLC: Enhances credibility with clients, vendors, and financial institutions.

- Sole proprietorship: Some industries may perceive it as less professional or less stable.

Comparing an LLC and a sole proprietorship isn’t just about legal formalities - it’s about aligning the business structure with long-term goals, risk management, and financial efficiency. Entrepreneurs must assess liability exposure, tax strategy, administrative responsibilities, and growth potential to make the right choice.

For small businesses with minimal risk and no immediate plans for expansion, a sole proprietorship can be a cost-effective solution. However, if asset protection, tax flexibility, and credibility are priorities, an LLC often provides greater security and strategic advantages.

5 Key factors influence the decision between an LLC and a sole proprietorship

Liability protection: Personal risk & business debt

One of the primary considerations for entrepreneurs is liability protection - how much personal risk they are exposed to if their business incurs debt or faces legal claims.

How LLC limit personal liability

An LLC (Limited liability company) is designed to protect its owners - known as members - from personal liability for business debts and legal obligations. This separation between personal and business assets is one of the key reasons many entrepreneurs opt for this structure.

Key aspects of LLC liability protection:

- Limited personal risk: If an LLC is sued or accumulates business debt, creditors can only go after the company’s assets, not the personal assets of its owners.

- Legal entity status: Unlike a sole proprietorship, an LLC is a distinct legal entity separate from its owners, meaning personal liability is limited unless an owner personally guarantees a loan or engages in fraudulent activities.

- Protection in lawsuits: If a customer files a lawsuit against the business, for a defective product, only the LLC’s assets are at risk.

- Piercing the corporate veil: While an LLC offers strong liability protection, courts can override this if business owners fail to maintain proper separation between personal and business finances, commit fraud, or engage in misconduct.

Sole proprietorship and unlimited personal liability

A sole proprietorship, by contrast, offers no legal separation between the business and its owner. This means the owner is personally responsible for all debts, obligations, and legal liabilities. If the business faces financial or legal troubles, creditors can target the owner’s personal assets, including their home, car, and personal savings.

Risks of sole proprietorship liability:

- Unlimited personal liability: The business and owner are legally the same entity, so if the business incurs debt or is sued, the owner is fully responsible.

- Risk to personal assets: Business lawsuits, unpaid debts, or contract disputes can result in personal bankruptcy if the business cannot cover its obligations.

- Difficulties in raising capital: Since a sole proprietorship lacks legal separation, lenders are less likely to offer loans without requiring personal guarantees.

- Higher risk in high-liability industries: Sole proprietors in high-risk industries (e.g., construction, food services, healthcare) are more vulnerable to financial ruin due to lawsuits and operational risks.

Taxation: How you pay taxes in LLCs and sole proprietorships

Both LLCs and sole proprietorships follow pass-through taxation, but LLCs offer more flexibility, allowing owners to choose S Corporation or C Corporation status for potential tax savings.

Understanding the tax implications of LLCs and sole proprietorships

One of the most crucial factors when choosing a business structure is taxation. Both LLCs and sole proprietorships operate under pass-through taxation, but the way taxes are calculated and reported varies significantly. Business owners must understand these differences to optimize their tax liabilities and take advantage of potential deductions.

Pass-through taxation in sole proprietorship vs. LLC

Both sole proprietorships and LLCs (unless taxed as a corporation) follow a pass-through taxation model. This means that the business itself is not taxed at the entity level; instead, profits and losses pass through to the owner's personal tax return. However, the taxation structure differs:

- Sole proprietorship: The business income is reported directly on Schedule C of the owner’s Form 1040. There is no option for tax classification flexibility.

- LLC: By default, a single-member LLC is taxed like a sole proprietorship, but it has the flexibility to elect S Corporation or C Corporation tax treatment for potential tax savings.

Tax deductions & benefits: Which offers more advantages?

Tax deductions can significantly lower taxable income. While both structures allow deductions for business expenses, LLCs generally offer greater flexibility in tax planning.

| Tax deduction | Sole proprietorship | LLC (default taxation) | LLC (S corp election) |

|---|---|---|---|

| Business expenses | Yes | Yes | Yes |

| Health insurance premiums | Yes (Limited) | Yes (More flexibility) | Yes (Deductible for owner-employee) |

| Retirement plan contributions | Yes | Yes | Yes (More contribution flexibility) |

| Home office deduction | Yes | Yes | Yes |

| Pass-through deduction | Yes (If eligible) | Yes (If eligible) | Yes (If eligible) |

| Salary & payroll deductions | No | No | Yes |

Example: A cafe owner operating as an LLC may deduct health insurance premiums and higher retirement contributions compared to a sole proprietor, potentially reducing taxable income.

Choosing the right tax structure for your business

The best choice depends on the business’s income level, financial goals, and willingness to manage additional administrative requirements. Seeking professional tax advice ensures compliance and maximizes tax-saving opportunities.

- If simplicity and ease of tax filing are top priorities, a sole proprietorship is the most straightforward.

- If you seek liability protection with tax flexibility, an LLC offers various tax classification options.

- If reducing self-employment taxes is a primary goal, electing S Corporation status for an LLC can be advantageous.

Business flexibility & scalability

Business owners must consider flexibility and scalability when choosing between a Limited Liability Company (LLC) and a Sole Proprietorship. This section explores how each structure affects a business’s ability to adapt to evolving market conditions.

Can an LLC scale better than a sole proprietorship?

The ability to scale a business depends on legal structure, financial management, and operational flexibility. Below is a comparison of how LLCs and Sole Proprietorships support business growth:

| Criteria | Sole proprietorship | LLC |

|---|---|---|

| Legal structure | Single-owner structure, no legal separation | Legal entity separate from the owner |

| Ability to hire employees | Owner hires under personal tax ID, may face liability risks | Easier to hire employees due to legal separation and liability protection |

| Raising capital | Limited to personal savings, loans, or grants | Can attract investors, obtain business credit |

| Expansion potential | Challenging due to personal liability and tax burden | Easier to expand with structured legal framework |

| Regulatory compliance | Minimal formalities, but may lack credibility | Requires compliance but enhances credibility |

Key takeaways

- A sole proprietorship is ideal for small, low-risk businesses but limits scalability.

- An LLC offers a structured framework, allowing for easier expansion and investment.

- Many entrepreneurs transition from sole proprietorship to LLC as their business grows to enhance credibility, protect personal assets, and secure funding.

- The choice between these structures depends on long-term business goals and risk tolerance.

Understanding the flexibility and scalability of each business structure is crucial for making informed decisions that align with business growth strategies.

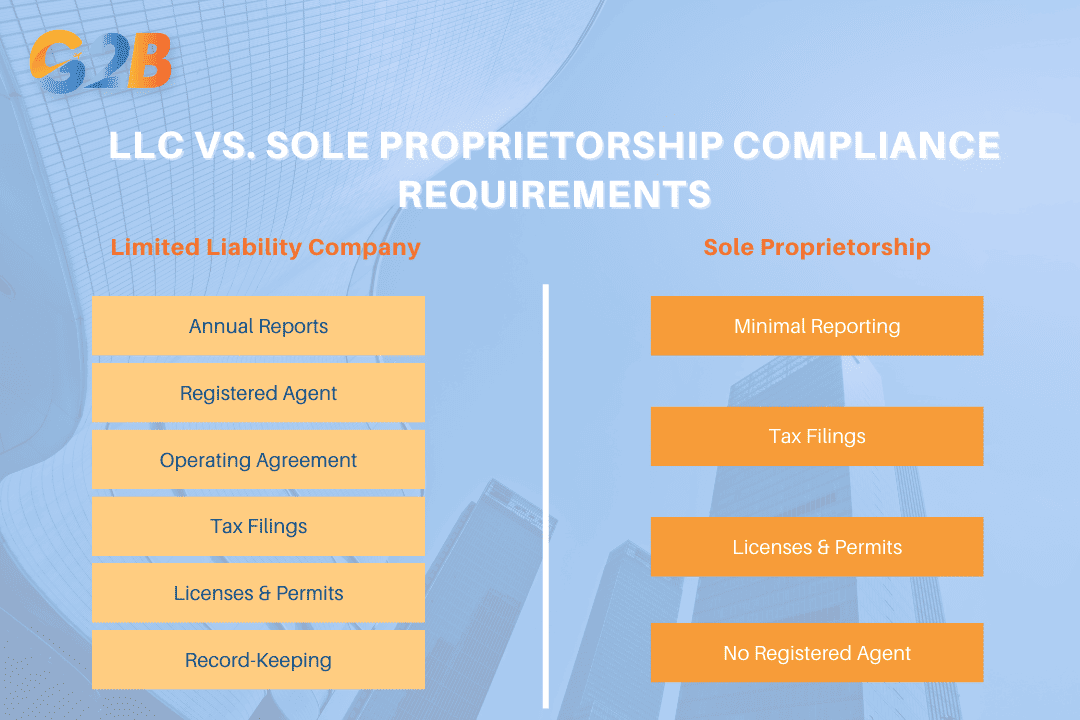

Administrative requirements & ongoing compliance

The ongoing administrative requirements and compliance obligations play a significant role in business operations. Understanding these obligations helps business owners avoid penalties and ensure long-term sustainability.

Annual filing & reporting requirements

The level of administrative upkeep varies significantly between LLCs and Sole Proprietorships. Below is a comparison of their ongoing compliance responsibilities:

LLC compliance requirements:

- Annual reports: Many U.S. states require LLCs to file an annual or biennial report with the Secretary of State. These reports maintain the company’s good standing and often involve a filing fee.

- Registered agent requirement: An LLC must designate a registered agent to receive legal documents on behalf of the business.

- Operating agreement maintenance: While not always legally required, an operating agreement helps LLCs maintain clear governance structures.

- State & federal tax filings: Depending on its tax classification, an LLC may need to file IRS FoForm 1120-S (for S Corporations).

- Business licenses & permits: LLCs operating 1065 (for partnerships) or in regulated industries must maintain up-to-date business licenses.

- Meeting minutes & record-keeping: Although not always mandated by law, maintaining accurate records, including meeting minutes and financial statements, can help protect an LLC’s liability shield.

Sole proprietorship compliance requirements:

- Minimal reporting: Unlike LLCs, sole proprietors do not have to file annual reports with the state.

- No separate tax filings: Business income is reported directly on the owner’s personal tax return (Schedule C, IRS Form 1040).

- Business licenses & permits: Some local or state regulations may require permits, but these are typically fewer than those required for LLCs.

- No registered agent required: Since a sole proprietorship is not a separate legal entity, there is no need to designate a registered agent.

Key takeaway: LLCs have significantly more administrative obligations than sole proprietorships, requiring periodic filings, compliance with state regulations, and record-keeping. In contrast, sole proprietorships offer simplicity but may lack the formal protections of an LLC.

LLC compliance requirements are different from those of a sole proprietorship

Funding & business credibility

Securing funding and establishing business credibility are critical for long-term success. Let’s analyze how each structure affects funding opportunities and credibility below.

Can you raise capital more easily as an LLC?

One of the major advantages of forming an LLC is its ability to attract investors and secure funding more easily than a sole proprietorship. Here’s why:

- Ability to issue ownership shares: Unlike sole proprietors who own their business entirely, LLCs can have multiple members, making it easier to bring in investors in exchange for equity.

- Perceived stability: Investors often view LLCs as more structured and legally sound, reducing concerns about financial risks.

- Venture capital & angel investment: Most venture capital firms and angel investors prefer investing in businesses with legal separation from their owners, which an LLC provides.

- Conversion flexibility: If an LLC later wants to expand its funding options, it can convert to a corporation to issue stocks.

For example, a tech startup seeking seed funding will likely struggle as a sole proprietorship, as most investors prefer structured entities like LLCs or corporations. The lack of legal separation in a sole proprietorship deters investors due to the increased financial risk.

Loan approvals: Sole proprietorship vs. LLC

Both LLCs and sole proprietors can apply for business loans, but banks and financial institutions often favor structured business entities. Here’s how each structure compares:

| Criteria | LLC | Sole proprietorship |

|---|---|---|

| Loan approval rates | Higher, due to legal entity status | Lower, as banks view it as personal debt |

| Collateral requirement | Might be required but can be business assets | Often requires personal assets as collateral |

| creditworthiness | Based on business credit history | Based on personal credit score |

| Loan amounts | Higher loan limits | Typically lower limits |

Sole proprietors often struggle with loan approvals because lenders see them as an extension of the owner's finances. Without a legally distinct entity, banks perceive higher risk and may impose stricter lending requirements.

Business credit scores & credibility impact

Business credibility affects a company’s ability to secure contracts, obtain favorable terms with suppliers, and rent commercial space. Here's how LLCs and sole proprietorships differ:

- Separate business credit for LLCs: LLCs can establish a business credit profile independent of the owner’s personal credit, which enhances financial opportunities.

- Perception by vendors & landlords: Many landlords and suppliers prefer working with LLCs due to their legal structure and stability.

- Longevity & market perception: LLCs are seen as more professional, leading to increased trust from customers and business partners.

Industry-specific considerations: Which structure works best?

Choosing between an LLC and a Sole Proprietorship depends on the industry in which a business operates. Let’s analyze key industries and their optimal business structures.

Best business types for LLC vs. Sole proprietorship

| Business type | LLC | Sole proprietorship |

|---|---|---|

| Freelancers & consultants | Optional (for liability protection) | Preferred (lower cost, simple taxes) |

| E-commerce businesses | Recommended (scalability, liability) | Suitable for small-scale operations |

| Restaurants & cafés | Required in most cases (liability) | Not recommended (high risk exposure) |

| Financial services | Often required (compliance regulations) | Not allowed in many states |

| Healthcare professionals | Recommended (legal protection) | Not advised (personal liability risks) |

| Real estate investment | Common (asset protection) | Risky (personal liability exposure) |

| Bloggers & content creators | Optional (brand protection) | Suitable (minimal risk) |

| Construction & trades | Recommended (high liability) | Not recommended (legal exposure) |

| Tech startups | Preferred (funding potential) | Only viable for solo developers |

Industries where an LLC is essential

Certain industries will benefit greatly from the liability protection and credibility an LLC provides:

1. Financial services & investment firms

- Regulatory requirements: Many states and federal agencies mandate financial service providers to operate under a legal entity such as an LLC, S-Corp, or C-Corp.

- Trust & credibility: Clients prefer to engage with financial firms that demonstrate legal structure and accountability.

2. Healthcare & medical professions

- Professional liability risks: Doctors, therapists, and private practitioners face malpractice risks, making an LLC essential for asset protection.

- Legal compliance: Many states require medical professionals to form a professional LLC (PLLC) instead of operating as a sole proprietorship.

3. Real estate investment & property management

- Asset protection: Real estate investors use LLCs to separate personal assets from rental properties and shield themselves from lawsuits.

- Tax benefits: LLCs offer pass-through taxation while providing liability protection for property owners.

4. Construction & contracting businesses

- High-risk industry: Contractors face legal risks related to worksite accidents, property damage, and contract disputes.

- Client requirements: Many clients require contractors to have an LLC for insurance and liability purposes.

5. Restaurants, catering, and food services

- Public health regulations: The food industry involves strict compliance requirements, and an LLC offers legal protection from foodborne illness claims.

- Supplier & lease agreements: Many suppliers and landlords require restaurant owners to operate as an LLC for liability reasons.

Pros & cons of LLC vs. Sole proprietorship

LLC (Limited liability company) and a Sole proprietorship offer unique benefits, but also come with limitations that impact liability, taxation, credibility, and scalability. Let’s break down the pros and cons of each structure.

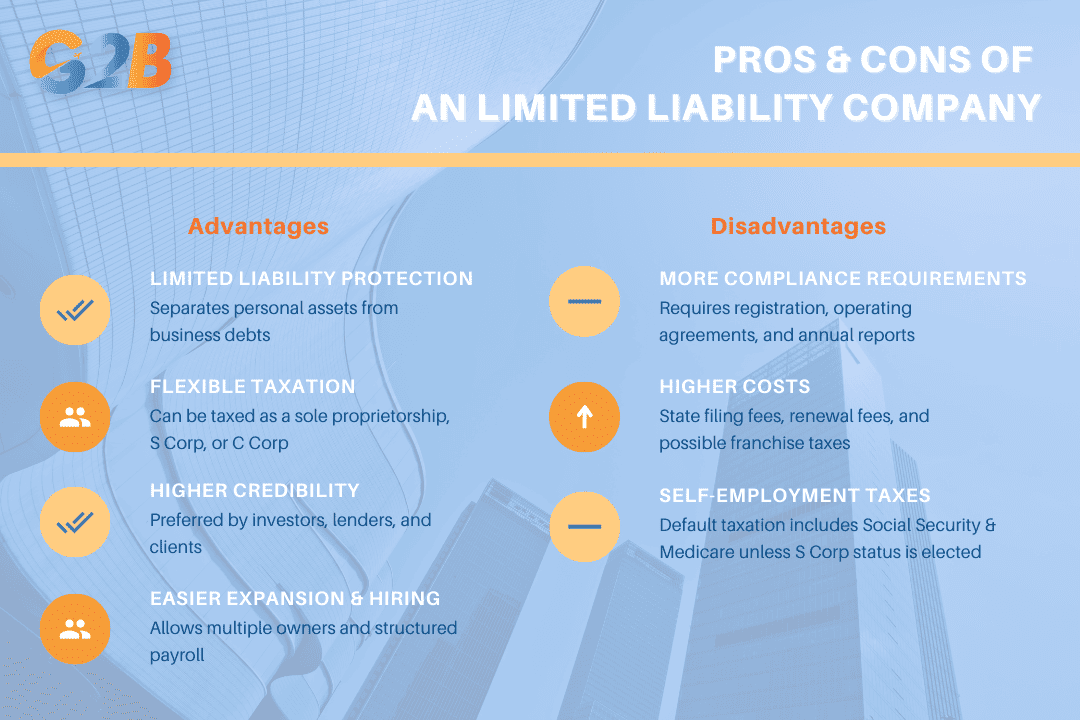

Pros & cons of an LLC

An LLC offers limited liability protection, flexible taxation options, and greater credibility. However, it comes with higher setup costs, compliance requirements, and potential self-employment taxes unless electing S corporation status.

Pros of an LLC

Limited liability protection

- One of the primary reasons entrepreneurs choose an LLC is personal asset protection. Unlike a sole proprietorship, an LLC legally separates the owner's personal assets from business debts and liabilities.

- If the company faces a lawsuit or debt, creditors generally cannot seize personal assets like a home or savings (unless personal guarantees were signed).

Flexible taxation options

- LLCs offer a pass-through taxation structure by default, meaning profits are taxed on the owners’ personal tax returns without a separate business tax.

- LLCs can also elect to be taxed as an S Corporation or C Corporation, which may provide tax advantages depending on income level and structure.

Higher credibility for clients, investors, and lenders

- Operating as an LLC enhances credibility, making it easier to secure business loans, attract investors, and establish trust with customers.

- Some corporate clients and government contracts prefer to work with LLCs over sole proprietors due to perceived stability.

Easier business expansion and hiring

- Unlike a sole proprietorship, an LLC can bring in multiple owners (members) and issue ownership stakes.

- LLCs also facilitate hiring employees, as they allow for more structured payroll and benefits management.

Cons of an LLC

More paperwork and compliance requirements

- LLCs require formal registration, including filing Articles of Organization and maintaining operating agreements.

- Many states require annual reports and state fees, which vary depending on location.

Higher setup and maintenance costs

- Forming an LLC involves state filing fees, which can range from $50 to $500+, depending on the state.

- LLC owners may also need to pay annual franchise taxes or renewal fees.

Possible self-employment taxes (unless electing S-corp taxation)

- By default, LLC owners are subject to self-employment taxes (Social Security & Medicare) on their entire income.

- However, electing S-corp taxation may help reduce self-employment tax liability.

LLCs offer both advantages and disadvantages for business owners

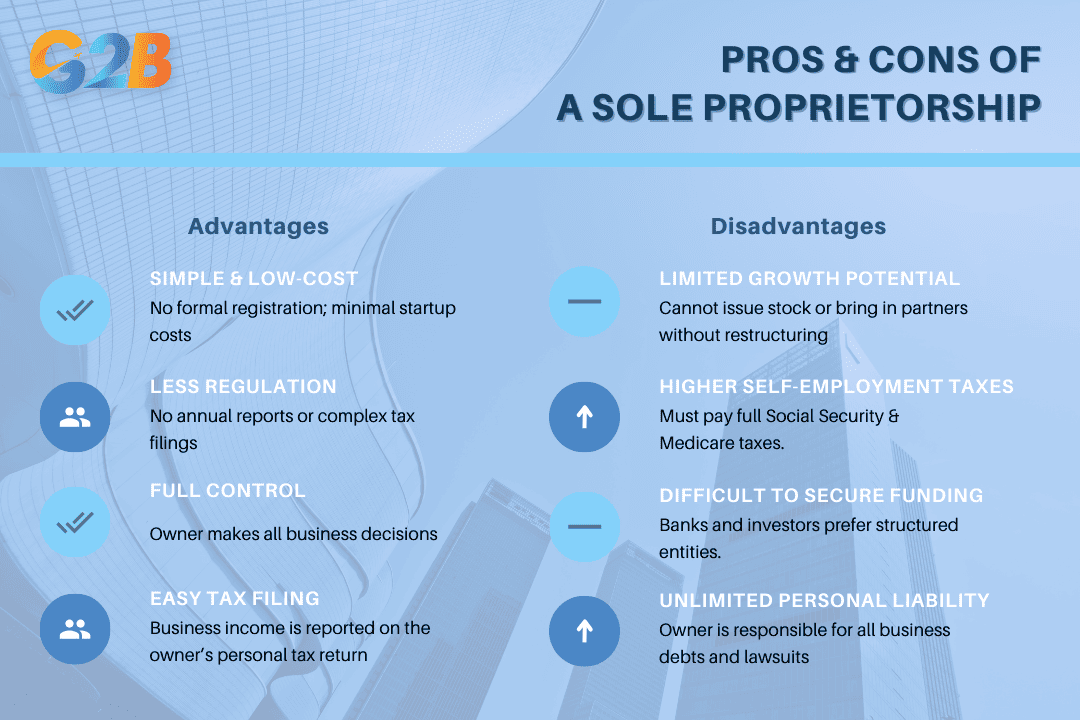

Pros & cons of a sole proprietorship

A sole proprietorship is the simplest and cheapest business structure, offering full control and minimal regulatory requirements. However, it also comes with many disadvantages that entrepreneurs need to consider.

Pros of a sole proprietorship

Simple and inexpensive to start

- No need for formal registration - the business and owner are legally the same entity.

- Sole proprietors only need to register a DBA (Doing Business As) if using a trade name, making it the cheapest and easiest business structure.

Less regulatory burden

- No mandatory annual reports, complex tax filings, or compliance requirements.

- Business income is simply reported on Schedule C of the owner’s personal tax return.

Full control over business decisions

- As the sole owner, there is no need to consult partners or members when making business decisions.

- Profits flow directly to the owner, without needing to split earnings.

Straightforward tax filing

- No separate business tax return is required; all business income is reported on the individual’s Form 1040.

- Fewer bookkeeping and tax complexities compared to LLCs and corporations.

Cons of a sole proprietorship

Unlimited personal liability

- The owner is personally responsible for all business debts, lawsuits, and liabilities.

- If the business is sued or falls into debt, personal assets (house, car, savings) can be used to satisfy business obligations.

Harder to secure funding or loans

- Banks and investors generally prefer structured business entities like LLCs.

- Without a legal distinction between the owner and the business, securing business credit or investment is difficult.

Self-employment tax on all income

- Sole proprietors must pay self-employment tax (15.3%) on their entire net earnings.

- Unlike LLCs, they cannot elect S-corp status to reduce self-employment tax obligations.

More difficult to scale beyond a solo business

- Sole proprietors cannot issue stock or ownership stakes.

- If the owner wants to expand and bring in partners, the business must be restructured into an LLC or corporation.

A sole proprietorship is the simplest business structure, with many pros and cons

Comparison table of LLC vs. Sole proprietorship

| Feature | LLC | Sole proprietorship |

|---|---|---|

| Liability protection | Yes (limited liability) | No (personal liability) |

| Taxation | Flexible (pass-through or corporate tax) | Pass-through only |

| Credibility & trust | Higher (recognized as a separate entity) | Lower (individual business) |

| Ease of formation | Requires registration & fees | Simple, minimal paperwork |

| Ongoing compliance | Moderate (annual reports, fees) | Low (few regulatory requirements) |

| Ability to raise capital | Easier (can take on investors) | Harder (personal credit reliance) |

| Tax savings potential | Possible (S-Corp election) | None (subject to full self-employment tax) |

| Expansion flexibility | Easier (multiple members, hiring) | Harder (limited growth options) |

Key takeaways

- LLCs provide liability protection, tax flexibility, and business credibility, but require more paperwork and higher costs.

- Sole proprietorships are simpler and cheaper to start, but expose owners to personal liability and make expansion more difficult.

- The best choice depends on business goals, risk tolerance, and long-term vision.

- If your business is small, low-risk, and self-funded, a sole proprietorship may suffice. But if you plan to scale, seek investors, or want liability protection, an LLC is the better choice.

How to choose between LLC & sole proprietorship

Choosing between a Limited Liability Company (LLC) and a Sole Proprietorship is a critical decision that can impact your business’s operation. This section below will help entrepreneurs assess your situation and make an informed decision.

Key questions to ask before deciding

Before selecting a business structure, entrepreneurs should evaluate their needs and long-term goals by answering the following questions:

1. How much personal liability risk am I willing to take?

- A sole proprietorship does not provide a legal separation between the business and the owner, meaning personal assets (home, savings, car) could be at risk if the business faces lawsuits or debts.

- An LLC offers limited liability protection, meaning your assets are generally shielded from business debts and legal claims, provided you maintain proper corporate formalities.

2. How do I want my business to be taxed?

- Sole proprietors report business income on their personal tax returns and are responsible for self-employment taxes (15.3%) on all net earnings.

- LLCs have tax flexibility: they can be taxed as a sole proprietorship, partnership, or elect to be treated as an S Corporation or C Corporation to reduce self-employment tax liabilities in some cases.

3. What are my business’s growth and scalability plans?

- If you plan to stay small, with minimal administrative complexity, a Sole Proprietorship is the simplest structure.

- If you foresee expanding, hiring employees, or attracting investors, an LLC provides better credibility and scalability.

4. What are my industry-specific legal requirements?

- Certain industries (e.g., consulting, e-commerce, real estate investing) have higher liability risks and may benefit more from an LLC’s liability protection.

- If your industry has low legal risk and minimal startup costs, a Sole Proprietorship may suffice.

5. How important is business credibility?

- LLCs often appear more professional to clients, vendors, and lenders, making it easier to secure contracts, business credit, and loans.

- Sole Proprietors may find it harder to gain credibility without a formal legal structure.

Final comparison table: LLC vs. sole proprietorship at a glance

To provide a clear, side-by-side comparison, this table outlines the key differences across essential business factors, ensuring a structured and informed approach to decision-making.

LLC vs. Sole proprietorship: Key differences

| Factor | LLC | Sole proprietorship |

|---|---|---|

| Liability protection | Limited liability - owners (members) are not personally responsible for business debts or legal actions. | No liability protection - owner is personally liable for all business debts and legal claims. |

| Tax structure | Pass-through taxation by default but can elect to be taxed as an S Corp or C Corp. | Income is reported directly on the owner’s tax return (Form 1040, Schedule C). |

| Scalability & growth potential | Easier to attract investors, can have multiple owners (members). | Limited to the owner; business growth is solely dependent on personal resources. |

| Administrative complexity | Requires formal registration with the state, annual reports, and compliance with state regulations. | Minimal paperwork - no formal registration required in most states. |

| Startup costs | Typically ranges from $50 to $500 depending on the state. Ongoing fees may apply. | Very low to no cost; only requires a business license in some locations. |

| Tax benefits & deductions | Can deduct operating expenses, health insurance, and potentially avoid self-employment tax if taxed as an S Corp. | Can deduct business expenses, but must pay full self-employment tax (15.3%). |

| Operational flexibility | Can have multiple members or remain a single-member LLC. Allows for flexible management structures. | Owner makes all business decisions without the need for formal meetings or agreements. |

| Business credibility | More credibility with banks, investors, and customers due to formal structure. | Perceived as less stable or professional compared to an LLC. |

| Funding opportunities | Easier to secure business loans, attract investors, and establish business credit. | Relies mostly on personal savings and credit; difficult to secure external funding. |

| Compliance requirements | Must file formation documents, operating agreements, and annual reports in many states. | No formal compliance requirements beyond necessary business licenses and tax filings. |

Key takeaways

- If liability protection is a primary concern, an LLC is the clear choice.

- If simplicity and low costs are priorities, a sole proprietorship may be the better option.

- For those seeking funding and credibility, an LLC provides more advantages.

- Tax flexibility in an LLC allows for potential savings, while a sole proprietorship maintains straightforward tax filing.

The right business structure depends on specific goals and priorities. A Sole Proprietorship offers simplicity and full control, while an LLC provides legal protection, credibility, and potential tax benefits. For a deeper understanding, explore in-depth guides or schedule a free consultation with an expert.