Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom When starting a business, selecting the appropriate legal structure is crucial to ensuring long-term success and compliance. Two of the most widely chosen structures are the Limited Liability Company (LLC) and the corporation. Understanding these key differences, along with the advantages and drawbacks of LLCs vs. Corporations, is essential for making an informed decision that aligns with your business goals.

5 key factors to consider when comparing LLCs and Corporations

Deciding between a Limited Liability Company (LLC) and a corporation requires a thorough evaluation of various business factors. Below are the key considerations that can help business owners make an informed decision.

5 Key factors to consider when comparing LLCs and Corporations

1. Liability protection

Both LLCs and corporations offer limited liability protection, but the extent and nature of that protection differ:

- LLC: Members are shielded from personal liability for business debts and legal actions. However, this protection can be compromised if courts determine that the LLC is not properly maintained.

- Corporations: Shareholders are also protected from personal liability, but corporations have a more formalized structure, making it harder for courts to hold owners personally responsible for business debts.

Key takeaway: While both structures protect personal assets, corporations may provide stronger protection due to stricter corporate governance rules.

2. Taxation and financial flexibility

Tax treatment is one of the most significant differences between LLCs and corporations.

- LLC taxation:

- By default, LLCs benefit from pass-through taxation, meaning business income is reported on the owners’ personal tax returns.

- LLCs can elect to be taxed as an S corporation or a C corporation, offering flexibility based on the owner’s financial strategy.

- Owners may be subject to self-employment tax (covering Social Security and Medicare), which can be higher than corporate tax rates.

- Corporation taxation:

- C corporations face double taxation - corporate profits are taxed at the business level, and dividends are taxed again when distributed to shareholders.

- S corporations avoid double taxation by passing income directly to shareholders, but they have restrictions on ownership

Key takeaway: LLCs offer more tax flexibility, while corporations require careful tax planning to avoid double taxation.

3. Ownership structure and investor appeal

Ownership structure plays a crucial role in deciding between an LLC and a corporation.

- LLC ownership:

- LLCs can have one or multiple owners (members) with flexible profit-sharing arrangements.

- Ownership transfer can be complicated as it often requires approval from all members.

- LLCs cannot issue stock, limiting their ability to attract investors.

- Corporation ownership:

- Corporations have a formal ownership structure with shareholders, directors, and officers.

- Stock issuance allows corporations to attract investors and raise capital more easily.

- Ownership transfer is straightforward, making corporations ideal for businesses planning to scale.

Key takeaway: If attracting investors or issuing stock is a priority, a corporation is the better choice.

4. Regulatory and compliance requirements

LLCs and corporations differ significantly in their legal and administrative burdens.

- LLC compliance:

- Generally requires less paperwork and fewer ongoing compliance requirements.

- Most states mandate an Operating Agreement, which outlines member roles and responsibilities.

- Annual reports and fees may be required depending on the state.

- Corporation compliance:

- Must adhere to strict corporate formalities, including maintaining bylaws, holding annual shareholder meetings, and keeping detailed corporate records.

- More compliance oversight from government agencies, particularly for publicly traded companies.

Key takeaway: LLCs offer simplicity, while corporations require greater formalities but may be better suited for long-term scalability.

5. Scalability and long-term growth

For businesses with long-term growth potential, scalability is a major factor.

- LLCs:

- Best suited for small-to-medium-sized businesses that prioritize operational flexibility.

- Challenging to raise capital due to restrictions on ownership structure.

- Corporations:

- Ideal for companies planning to expand significantly or go public.

- Easier to raise funds through stock sales and venture capital investments.

Key takeaway: Corporations provide a more structured path for growth, while LLCs work well for businesses that want flexibility.

LLC vs. Corporation: A quick comparison table

Choosing between an LLC and a corporation is an important decision that impacts liability, taxation, governance, and scalability. Below is a comprehensive comparison table highlighting the key differences:

| Factor | LLC | Corporation (C corp & S corp) |

|---|---|---|

| Ownership structure | Owned by members (individuals, partnerships, or entities) | Owned by shareholders (can be individuals or entities) |

| Liability protection | Limited liability for members | Limited liability for shareholders |

| Tax treatment | Pass-through taxation by default; can elect corporate tax | C corp: Double taxation; S Corp: Pass-through taxation |

| Management & governance | Flexible; members or managers can run the company | Formal structure with a board of directors and officers |

| Compliance & reporting | Less formal, minimal reporting requirements | Stricter compliance, annual reports, shareholder meetings |

| Funding & investment | Limited ability to raise capital, no stock issuance | Can issue stock, easier to attract investors |

| Scalability & exit | Harder to scale, dissolution upon major ownership change | Easier to scale, perpetual existence |

Ownership & management differences of LLC and Corporations

These two business entities operate under distinct legal, financial, and operational models, which directly influence decision-making, flexibility, and corporate governance.

Ownership structure

Ownership in an LLC and a corporation differs significantly in terms of equity distribution, transferability, and control mechanisms.

LLC: Members vs. managers

- LLC ownership: LLCs are owned by members, who may be individuals, corporations, or other LLCs. Unlike corporations, ownership is not represented by shares but by membership interests.

- Flexibility: Members can structure ownership as they see fit, including defining different classes of ownership in an Operating Agreement.

- Transfer restrictions: LLC ownership interests are generally more restrictive when transferring. Most states require unanimous or majority approval from existing members to sell or transfer ownership.

- Management options:

- Member-managed LLC: All members participate in the decision-making process, similar to a partnership.

- Manager-managed LLC: Members appoint managers (who can be members or external parties) to handle daily operations.

Corporation: Shareholders, board of directors & officers

- Corporation ownership: Corporations issue shares of stock, which represent ownership and voting rights.

- Transferability: Stock is freely transferable unless restricted by agreements. This makes corporations a preferred entity for investors and public trading.

- Shareholder role: Shareholders own the corporation but do not manage daily operations. They vote on major decisions and elect a board of directors.

- Board of directors: The board sets policies, oversees management, and ensures the corporation operates in the best interests of shareholders.

- Corporate officers: A structured hierarchy exists, with officers such as the CEO, CFO, and Secretary handling operational management.

Management flexibility

The management structure of LLCs and corporations differs significantly in terms of hierarchy, corporate formalities, and flexibility in governance.

LLC: Member-managed vs. manager-managed

- Less formality: LLCs require fewer formalities, with no obligations to hold annual meetings or maintain strict record-keeping.

- Customized management: LLCs can be structured in any way members agree upon, allowing for customized decision-making processes.

- Pass-through taxation: LLCs can elect to be taxed as a sole proprietorship, partnership, or even an S corporation, offering flexibility in financial planning.

- Decision authority: If member-managed, all members share decision-making responsibilities unless otherwise specified in the Operating Agreement.

Corporation: Rigid structure with corporate formalities

- Strict governance: Corporations must follow a more rigid management hierarchy, ensuring compliance with state and federal regulations.

- Mandatory meetings: Corporations are required to hold annual meetings for shareholders and directors and maintain detailed records of corporate decisions.

- Legal and tax implications: The structured management ensures clear delineation of duties and responsibilities, but it also results in double taxation (for C Corps) unless an S corporation election is made.

- Professionalism and credibility: A structured management system gives corporations a perception of stability, making them attractive to investors and lending institutions.

Decision-making & control

Decision-making power in an LLC and a corporation is determined by ownership structure and management roles.

- LLC decision-making:

- In a member-managed LLC, all members have a say in major business decisions unless specified otherwise in the Operating Agreement.

- In a manager-managed LLC, designated managers handle daily operations, reducing member involvement in routine decision-making.

- LLCs offer flexible voting rights that can be tailored to the needs of the members.

- Corporation decision-making:

- The Board of Directors makes high-level decisions and establishes corporate policies.

- Shareholders vote on significant matters such as mergers, acquisitions, and electing the board.

- Day-to-day operations are handled by corporate officers under the oversight of the board.

Liability protection: Understanding personal liability exposure

Liability protection is one of the most critical factors when choosing a company type. Business owners must understand how these structures shield personal assets from business debts and legal claims.

Limited liability for owners

While LLCs and corporations generally offer robust protection for personal assets, this protection can be compromised if business formalities are not properly followed. To maintain liability protection, owners must ensure a clear separation between personal and business activities, along with adherence to legal and financial requirements.

How LLCs and Corporations protect personal assets

Both LLCs and corporations are considered separate legal entities from their owners, meaning business debts and lawsuits typically do not impact personal assets such as homes, vehicles, or personal savings. Here’s how each structure provides protection:

- LLC (Limited Liability Company): Owners, known as members, are not personally liable for business debts or legal claims. Creditors can only pursue business assets, not personal ones.

- Corporation (C corporation & S corporation): Shareholders are similarly shielded from business liabilities. Their financial exposure is limited to their investment in the company.

Scenarios where liability protection can be lost (Piercing the corporate veil)

Piercing the corporate veil occurs when a court determines that business owners have failed to maintain a clear separation between personal and business finances. In such cases, personal assets may be used to satisfy business debts. Common reasons include:

- Failure to maintain corporate formalities: Not keeping accurate financial records, missing corporate meetings, or failing to file required documents.

- Commingling personal and business funds: Using a business bank account for personal expenses or vice versa.

- Fraud or misrepresentation: Engaging in deceptive business practices, such as obtaining loans without the intention to repay.

- Undercapitalization: If a company is deliberately underfunded and unable to cover foreseeable liabilities, courts may hold owners personally responsible.

Personal vs. business debt responsibility

While limited liability generally protects owners, there are exceptions where personal responsibility arises:

| Factor | LLC | Corporation |

|---|---|---|

| Personally guaranteed loans | Members may be required to sign personal guarantees for business loans, making them personally liable. | Shareholders or directors who personally guarantee debts can be held responsible. |

| Payroll taxes | Members can be held liable for unpaid payroll taxes if they fail to remit them properly. | Corporate officers responsible for payroll tax compliance can be personally liable for unpaid taxes. |

| Malpractice or personal negligence | LLC members offering professional services (e.g., doctors, lawyers) can be personally sued for malpractice. | Directors, officers, or employees who personally commit wrongdoing can be held liable, even if acting on behalf of the company. |

| Fraudulent business practices | Courts can hold LLC members personally liable if they commit fraud or misrepresent financial conditions. | Fraudulent activities by corporate executives or directors can expose them to personal liability. |

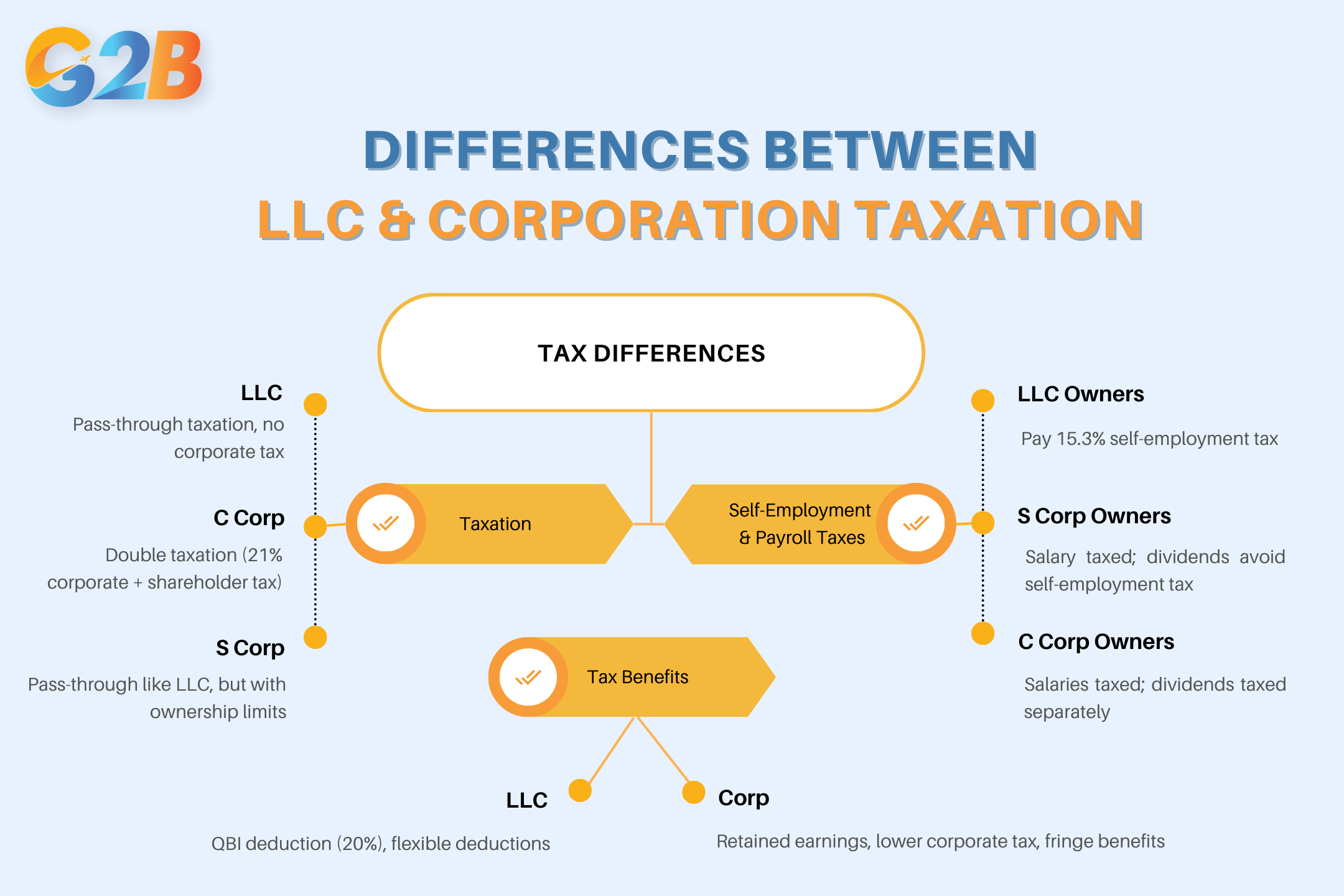

Tax differences: LLC vs. Corporation taxation explained

LLCs and corporations have distinct tax structures that can affect a business’s bottom line. Understanding these differences helps entrepreneurs make informed decisions to optimize tax efficiency and compliance.

LLCs and corporations have distinct tax structures

Pass-through taxation vs. Corporate taxation

One of the most critical differences between an LLC and a corporation is how they are taxed at the entity level.

- LLCs: Default taxation for an LLC follows the pass-through taxation model. This means that business profits and losses pass through to the owners (members), who report them on their personal income tax returns. The LLC itself does not pay federal income taxes.

- Corporations: C corporations (C Corps) face double taxation. The company pays corporate income tax on its profits at the federal level (21% as of 2024), and when those profits are distributed as dividends to shareholders, they are taxed again on individual tax returns.

- S corporations (S Corps): While legally corporations, S Corps avoid double taxation by electing pass-through taxation like an LLC. However, they have stricter eligibility requirements, such as a cap of 100 shareholders and restrictions on ownership types.

Self-employment taxes & payroll tax considerations

Self-employment taxes and payroll taxes also differ between LLCs and corporations, impacting how business owners compensate themselves.

- LLC members: Owners of an LLC (if taxed as a sole proprietorship or partnership) are considered self-employed and must pay self-employment tax (15.3% as of 2024), covering Social Security and Medicare. This tax applies to their entire share of the company’s net earnings.

- Corporation owners: Shareholders of a corporation (especially in an S Corp) who work in the business can classify themselves as employees and receive a salary. Payroll taxes (FICA) are deducted from wages, but dividends paid to shareholders are not subject to self-employment tax.

Tax considerations for owner compensation:

- LLC owners: Pay self-employment tax on their entire earnings.

- S corp shareholders: Can receive a “reasonable salary” subject to payroll tax and take additional income as dividends, which are not subject to self-employment tax.

- C corp shareholders: Typically receive salaries subject to payroll tax, and dividends are taxed separately.

Tax benefits & deductions

Each structure offers unique tax benefits and deductions that impact overall tax liability.

LLC tax benefits:

- Pass-through losses: LLC members can deduct business losses on personal tax returns (subject to passive activity loss rules).

- Qualified Business Income Deduction (QBI): Allows eligible LLCs to deduct up to 20% of their business income under Section 199A.

- Flexible expense deductions: LLCs can deduct operating expenses, home office expenses, and business-related travel without strict corporate governance rules.

Corporation tax benefits:

- Retained earnings: C Corps can retain earnings within the company, deferring tax liability compared to LLCs where all profits are taxed annually.

- Lower corporate tax rate: At 21%, the corporate tax rate can be lower than the highest personal tax rate (37%) for LLC owners with high incomes.

- Fringe benefits: C Corps can deduct employee benefits such as health insurance and retirement plans without the same limitations imposed on LLCs.

LLCs provide tax flexibility, allowing owners to avoid double taxation and take advantage of pass-through deductions. However, self-employment taxes can be costly. Corporations, particularly C Corps, benefit from lower corporate tax rates and more options for retaining earnings and offering fringe benefits. The right choice depends on business goals, profit distribution strategies, and tax planning needs. Consulting with a tax professional ensures optimal structuring for long-term financial benefits.

Investigating compliance & legal requirements

While LLCs generally have fewer formalities, corporations are subject to stricter legal obligations. Below is a breakdown of the key compliance aspects that differentiate LLCs from corporations.

Filing & reporting obligations

Every business entity must adhere to specific filing and reporting requirements mandated by state and federal laws. However, LLCs and corporations have distinct obligations:

- LLCs:

- Required to file Articles of Organization with the state upon formation.

- Must maintain an Operating Agreement (though not always legally required, it is highly recommended for internal governance).

- Depending on the state, LLCs may be required to file an Annual Report and pay state fees.

- Typically do not have to hold formal annual meetings or keep extensive records of company decisions.

- Corporations:

- Must file Articles of Incorporation with the state and pay incorporation fees.

- Required to draft and adopt Corporate Bylaws governing internal management.

- Legally obligated to hold annual shareholder and board of directors meetings, with meeting minutes documented.

- Must file Annual Reports and in some cases, franchise tax reports, depending on the state.

- Required to issue stock certificates and keep a record of shareholders.

The complexity of these requirements means that while LLCs enjoy more flexibility, corporations must adhere to a structured governance model.

Ongoing administrative burden

The ongoing legal and administrative responsibilities of maintaining an LLC or a corporation significantly impact business operations. Here’s how they compare:

- LLCs:

- Fewer formalities make it easier for small business owners to manage compliance.

- No legal requirement to hold annual meetings or record meeting minutes.

- Members have flexibility in decision-making without needing a board of directors.

- In some states, LLCs may need to renew their business registration periodically.

- Corporations:

- Subject to double taxation if structured as a C corporation (unless electing S corporation status).

- Must maintain meticulous records, including corporate resolutions, stockholder meetings, and financial statements.

- Required to follow strict internal structures, such as having a board of directors and defined officer roles.

- Failure to comply with corporate formalities can result in piercing the corporate veil, potentially exposing shareholders to personal liability.

Fundraising & investment options

Securing funding is a critical factor for business growth, and the choice between an LLC and a corporation significantly impacts access to capital. While both structures offer distinct advantages, they also come with limitations.

Raising capital: A comparative analysis of LLCs and Corporations

Corporations generally have an easier time raising capital due to their ability to issue stock and attract institutional investors. In contrast, LLCs face more limitations in capital raising, relying mainly on private funding and lacking the ability to access public markets.

LLCs: Limited access to venture capital & public investment

- Private funding reliance: LLCs primarily raise capital through personal savings, business revenue, bank loans, or private investors (such as angel investors or private equity firms). Unlike corporations, LLCs cannot issue stock, limiting their ability to attract large-scale investment.

- Membership restrictions: Some investors may be hesitant to invest in an LLC due to the complexities associated with membership interests. Additionally, certain venture capital firms prefer investing in corporations due to regulatory and tax considerations.

- Fewer reporting requirements: While LLCs face fewer regulatory burdens than corporations, this lack of transparency can sometimes deter institutional investors who prioritize governance and financial disclosures.

Corporations: Easier capital raising through equity financing

- Stock issuance: The most significant advantage of corporations in fundraising is the ability to issue stock. Corporations can raise capital by selling shares to investors, which makes them an attractive option for venture capital firms and public markets.

- IPO potential: Unlike LLCs, corporations can go public through an Initial Public Offering (IPO), providing a pathway to raise significant capital from public investors. This is a crucial factor for businesses with long-term growth aspirations.

- More attractive to investors: Due to the standardized structure of corporations and the ability to issue stock options, they are often the preferred entity for institutional investors, including hedge funds, pension funds, and private equity firms.

Stock & equity ownership

| Feature | LLC | Corporation |

|---|---|---|

| Equity Structure | Membership interests | Shares of stock |

| Transferability | Limited, may require approval of other members | Freely transferable |

| Preferred by Investors? | Less preferred due to lack of stock options | More preferred for venture capital |

- LLCs & membership interests: Unlike corporations, which issue shares of stock, LLCs distribute ownership through membership interests. This structure can be flexible, allowing customized profit-sharing arrangements, but it also complicates fundraising efforts as ownership transfers may require the approval of all members.

- Corporations & stock issuance: Corporations can issue multiple classes of stock, such as common and preferred shares. This makes it easier to structure investment deals and incentivize investors.

Attracting investors & scaling the business

- Scalability: Corporations are designed for scalability, allowing for easy expansion through the sale of additional shares. This makes them the preferred entity for high-growth startups seeking venture capital.

- Clear exit strategies: Many investors favor corporations due to clear exit strategies, such as acquisition or IPO, which provide a return on investment.

- Stock-based compensation: Corporations can offer stock options and equity-based compensation, making it easier to attract and retain top talent.

Scalability, growth, & exit strategies

The ability to scale a business, facilitate growth, and implement an exit strategy is vital when choosing between an LLC and a corporation. While both structures offer distinct advantages, their suitability depends on long-term goals and regulatory considerations.

Business growth potential

While LLCs offer flexibility, corporations provide growth potential and long-term stability.

1. Structural flexibility & growth constraints

- LLCs provide operational flexibility, allowing members to define management structures and profit distributions in an operating agreement. However, this flexibility can limit scalability since many investors prefer the standardized structure of corporations.

- Corporations, particularly C corporations, follow a well-established governance framework, making them more attractive for institutional investors and venture capitalists.

2. Raising capital for expansion

- LLC: Generally relies on internal funding, member contributions, and bank loans. Equity financing is challenging because LLC ownership is not structured in shares, making it less appealing to venture capitalists or public investors.

- Corporation: C corporations, in particular, are ideal for companies seeking to scale rapidly through venture capital or an eventual initial public offering (IPO).

3. Operational continuity & longevity

- LLCs often have limited lifespans based on their operating agreements. Some states require dissolution if a member exits unless provisions are in place.

- Corporations have perpetual existence, making them a preferred choice for businesses that aim for long-term scalability beyond the original owners.

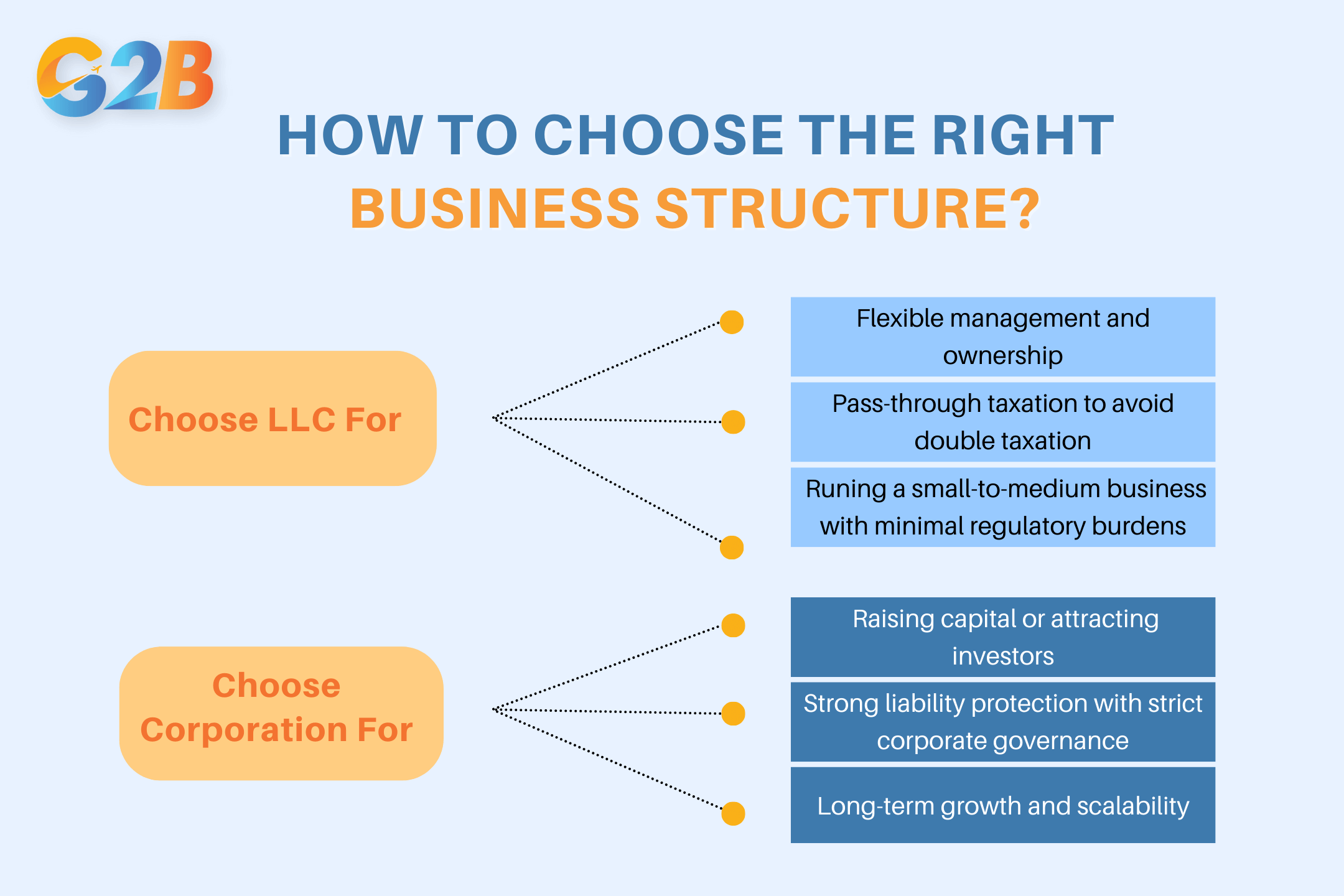

When choosing an LLC or a Corporation

Each entity type offers distinct advantages and drawbacks, making it essential to align your choice with your long-term business strategy.

Best for small businesses & solo entrepreneurs

For small businesses, freelancers, and solo entrepreneurs, an LLC is often the preferred choice due to its simplicity, flexibility, and tax benefits.

- Ease of formation & management: LLCs require fewer formalities compared to corporations. Unlike corporations, which must establish a board of directors, hold annual meetings, and maintain formal minutes, LLCs allow owners (members) to operate with minimal bureaucracy.

- Pass-through taxation: LLCs do not pay federal corporate taxes. Instead, profits and losses pass through to individual members' tax returns, avoiding double taxation. This structure is particularly advantageous for small businesses with moderate earnings.

- Lower administrative costs: LLCs typically have lower setup and ongoing compliance costs. Many states only require an Articles of Organization filing and a minimal annual report, making it cost-effective for small business owners.

- Personal asset protection: An LLC provides limited liability protection, shielding personal assets from business debts and lawsuits. This feature is crucial for sole proprietors transitioning to a formal business entity.

- Flexible profit distribution: Unlike corporations, which distribute profits based on share ownership, LLCs can allocate profits in a customized manner agreed upon in the operating agreement.

Best for startups & investors

For high-growth startups and businesses seeking outside investment, a corporation - especially a C corporation - is the preferred structure due to its scalability and investor-friendly framework.

- Easier access to venture capital & funding: Investors, especially venture capitalists (VCs), prefer corporations because they can issue stock, which allows for clear ownership structures and easy transferability of shares.

- Potential for IPO (Initial Public Offering): If the long-term goal is to go public, a C corporation is the best choice. The ability to issue multiple classes of stock makes it attractive to institutional investors.

- Better for retaining earnings: Unlike LLCs, which typically pass all profits to members, corporations can retain earnings to reinvest in growth and expansion without immediate tax consequences.

- Clear corporate governance: A corporation’s structured hierarchy - comprising shareholders, directors, and officers - ensures clear roles and responsibilities, making it easier to scale and manage a growing business.

- Stock incentives for employees: corporations can offer stock options and equity compensation, which is a valuable tool for attracting top talent, particularly in tech startups.

Final considerations

- Tax complexity: If you prefer straightforward taxes, an LLC is the better option due to its pass-through taxation. Corporations, especially C Corps, face double taxation (corporate and personal tax levels).

- Growth & exit strategy: If your goal is to build a scalable business that might be acquired or go public, a corporation is more suitable.

- Liability & risk management: If your business involves substantial liability risks (e.g., medical, finance, or manufacturing industries), forming a corporation may provide stronger liability protection.

- Administrative burden: If you want a simpler business structure with fewer compliance requirements, an LLC is the ideal choice.

How to choose the right structure?

Selecting the right structure depends on various factors, including business goals, industry, and long-term strategy. Below are key considerations to help entrepreneurs make an informed choice.

Key considerations to help entrepreneurs choose the right structure between LLC and Corporation

Key takeaways from the comparison

- Liability protection: Both LLCs and corporations provide limited liability protection, but corporations offer stronger shielding against legal claims due to their rigid corporate formalities.

- Tax implications: LLCs offer pass-through taxation by default, whereas corporations are taxed at the corporate level (C corporation) unless they elect S corporation status.

- Ownership & management: LLCs provide flexible ownership structures, while corporations have a strict hierarchical management system with shareholders, directors, and officers.

- Fundraising & investment: Corporations are more attractive to investors due to their ability to issue stock, whereas LLCs may face challenges in raising capital.

- Regulatory & compliance burden: Corporations require more paperwork, annual meetings, and formalities compared to LLCs, making them more suitable for larger operations.

Consulting legal & tax professionals

While these considerations provide a foundational understanding, consulting with a business attorney or tax professional is essential for making the best choice. Each state has different regulations for LLCs and corporations, and tax implications vary based on individual financial situations. A professional can:

- Assess your specific business needs and risks.

- Provide insights into state-specific regulations and compliance requirements.

- Advise on tax strategies to optimize financial outcomes.

- Help structure operating agreements or bylaws to align with your business goals.

Selecting the right business structure is a strategic decision that influences your company's future. An LLC may be ideal for those prioritizing operational flexibility and tax advantages, while a corporation is better suited for businesses focused on scaling, fundraising, and long-term growth. By carefully evaluating your business objectives and seeking expert advice, you can choose the structure that best aligns with your vision and success.

FAQs – Frequently asked questions about LLCs & Corporations

This section provides detailed answers to frequently asked questions regarding LLCs and corporations, offering valuable insights into the key differences and considerations for each entity type.

1. What are the main differences between an LLC and a Corporation?

LLCs and corporations differ in several key areas, including ownership, taxation, liability protection, and operational structure.

- Ownership & structure: An LLC has a flexible structure and can have one or multiple owners (called "members"), while a corporation is owned by shareholders and governed by a board of directors.

- Taxation: LLCs offer pass-through taxation, meaning profits and losses pass directly to members' tax returns. Corporations are taxed separately at the corporate level, with potential double taxation unless they elect S-Corp status.

- Compliance requirements: corporations require more formalities, such as annual meetings, bylaws, and shareholder reports. LLCs have fewer ongoing compliance requirements.

- Fundraising & growth: corporations are better suited for venture capital funding, while LLCs provide more flexibility for small business owners.

2. Which is better for tax purposes: LLC or Corporation?

The best tax structure depends on the business's revenue, reinvestment strategy, and owner preferences.

- LLC taxation: LLCs are taxed as pass-through entities by default, meaning business income is reported on the owner's personal tax return. However, an LLC can elect to be taxed as an S-Corp or C-Corp for potential tax advantages.

- Corporation taxation: C-corporations face double taxation (corporate tax + shareholder dividends). S-corporations avoid this but have restrictions on ownership and profit distribution.

- Which is better? If owners want to reinvest profits into growth, a corporation may be better. If they prefer direct income without corporate tax burdens, an LLC might be more beneficial.

3. Can an LLC convert into a Corporation later?

Yes, an LLC can convert into a corporation, but the process varies by state. Conversion methods include:

- Statutory conversion: A simple and direct method available in some states.

- Statutory merger: Involves forming a new corporation and merging the LLC into it.

- Non-statutory conversion: Requires dissolving the LLC and transferring assets to a new corporation.

Conversion may be necessary for businesses seeking venture capital or going public.

4. Which structure is better for raising venture capital?

Corporations, specifically C-Corps, are the preferred choice for investors due to:

- Stock issuance: Corporations can issue multiple classes of stock.

- Preferred shares: Investors often require preferred shares, which LLCs cannot issue.

- Scalability: A corporation's structured governance appeals to institutional investors.

While LLCs can receive investment, the complexity of ownership structures and tax implications make them less attractive to VCs.

5. What are the compliance requirements for an LLC vs. A Corporation?

Corporations have stricter compliance requirements than LLCs.

- Corporation compliance: Must hold annual meetings, file annual reports, maintain bylaws, and issue stock records.

- LLC compliance: Fewer requirements, but still must file an annual report (in some states) and maintain an operating agreement.

6. How does liability protection compare between LLCs and Corporations?

Both LLCs and corporations provide limited liability protection, meaning owners' personal assets are shielded from business debts.

- LLCs: Members are protected unless they personally guarantee a loan or commit fraud.

- Corporations: Shareholders have strong liability protection, but directors and officers may face personal liability in cases of misconduct.

7. Can a single person form a Corporation or an LLC?

Yes, both structures allow for single-member entities:

- Single-member LLCs (SMLLCs): Treated as a disregarded entity for tax purposes unless an election is made.

- Single-owner corporations: Require corporate formalities like bylaws and minutes but can be structured as an S-Corp to avoid double taxation.

10. How to decide whether an LLC or Corporation is right?

Consider these factors:

- Business goals: If seeking investors or planning an IPO, a corporation is better.

- Tax strategy: LLCs offer flexibility, while corporations suit reinvestment-heavy businesses.

- Liability & compliance: LLCs provide easier management, while corporations require more structure.

If flexibility and pass-through taxation are priorities, an LLC may be the optimal choice, while a corporation offers greater advantages for capital raising and scalability. By understanding these distinctions, entrepreneurs can select the structure that best supports their long-term goals. For personalized guidance, consider consulting with a business attorney or tax advisor.

Want to dive deeper? Explore our further guide on business structures. Reach out to G2B today for a comprehensive consultation based on your specific situation! G2B provides professional business support services, guiding you through every stage of business registration with reliability and dedication!