Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom Selecting the right legal structure is a strategic decision when starting a business. Two common business structures are partnerships and corporations, each with distinct advantages and drawbacks. This article will examine the distinctions between partnerships and corporations, offering a comprehensive analysis of their legal, financial, and operational implications. Understanding these differences is essential for entrepreneurs and business leaders seeking to optimise their organisational structure for growth and sustainability.

What is a Partnership? Key characteristics & types

A partnership is a business structure in which two or more individuals or entities collaborate to operate a business with shared profits, responsibilities, and liabilities. Unlike corporations, partnerships directly tie ownership to an individual.

Key characteristics of a Partnership

- Shared ownership: Two or more individuals or entities agree to co-own and manage the business.

- Pass-through taxation: Business profits and losses are reported on each partner’s personal tax return, avoiding corporate double taxation.

- Unlimited or limited liability: Depending on the type of partnership, liability can be personal (general partnership) or limited (LP, LLP).

- Flexible management: Unlike corporations with strict governance structures, partnerships allow for informal or contractual management.

- Profit and loss sharing: Partners distribute profits and losses based on their agreed-upon terms, which may not always be equal.

Types of Partnerships

Partnerships can take different legal forms depending on the level of liability protection and management structure. The three primary types are:

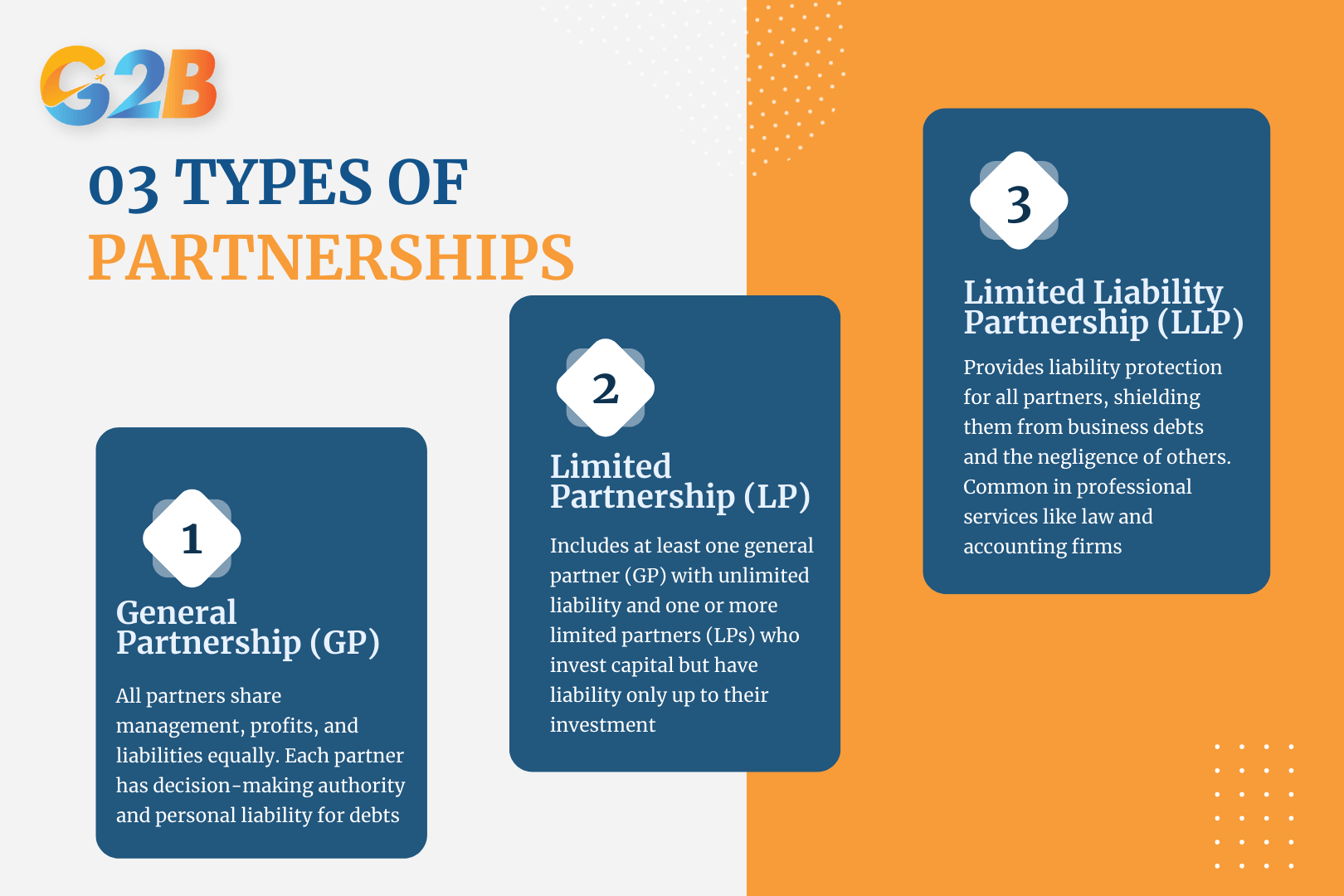

General Partnership (GP)

A general partnership is the simplest form of partnership, where all partners equally share management responsibilities, profits, and liabilities. Each partner has the authority to make business decisions, and all partners are personally liable for business debts and legal obligations.

Limited Partnership (LP)

A limited partnership consists of at least one general partner (GP) and one or more limited partners (LPs). General partners manage the business and assume unlimited liability, while limited partners contribute capital but have limited liability, meaning they are only liable up to the amount they invest.

Limited Liability Partnership (LLP)

A limited liability partnership offers liability protection to all partners, shielding them from personal responsibility for the business's debts or the negligence of other partners. This structure is particularly popular among professional services such as law firms, accounting firms, and consulting firms.

There are three primary types of partnerships

Advantages and disadvantages of Partnerships

| Advantages | Disadvantages |

|---|---|

| Simple and cost-effective to establish compared to corporations. | General partners have unlimited personal liability (except in LLPs). |

| Pass-through taxation avoids corporate double taxation. | Disagreements between partners can disrupt operations. |

| Flexible management structure with no strict corporate governance. | Raising capital can be challenging compared to corporations. |

| More expertise and resources are pooled together than in a sole proprietorship. | Partnerships dissolve when a partner |

What is a Corporation? Key characteristics & types

A corporation is a legally distinct business entity that operates separately from its owners. It is created through a formal process known as incorporation, which grants it rights and responsibilities similar to those of an individual.

Key characteristics of a Corporation

- Limited liability: Shareholders are not personally responsible for the corporation’s debts and liabilities.

- Perpetual existence: The corporation continues to exist beyond the involvement of its original owners.

- Centralized management: A board of directors oversees the company’s activities, and officers handle daily operations.

- Separate taxation: Depending on the type, corporations may be subject to corporate income tax, leading to potential double taxation.

- Regulatory requirements: Corporations must comply with stricter reporting and operational regulations compared to other business structures.

Types of Corporations

Corporations come in various forms, each designed to meet different business needs and tax structures.

C Corporation (C Corp)

C corporations are the most common type of corporation in the United States. They are separate legal entities from their owners and are subject to corporate income tax.

S Corporation (S Corp)

S corporations are similar to C corporations but offer pass-through taxation, meaning profits and losses pass directly to shareholders without being taxed at the corporate level.

Professional Corporation (PC)

A professional corporation is designed for licensed professionals such as doctors, lawyers, and accountants. It provides liability protection for business debts but does not shield professionals from malpractice claims.

Three primary types of Corporations that entrepreneurs should understand

Advantages and disadvantages of Corporations

| Advantages | Disadvantages |

|---|---|

| Limited liability - Protects owners’ personal assets from business debts and lawsuits. | Double taxation - C corporations face corporate income tax and personal income tax on dividends. |

| Perpetual existence - The business can continue even if ownership changes. | Complex formation process - Requires incorporation, legal documentation, and compliance with regulations. |

| Easier capital raising - Corporations can issue stock to attract investors. | Strict regulatory requirements - Subject to financial reporting, annual meetings, and compliance measures. |

| Separate legal entity - Can enter contracts, own property, and sue or be sued. | Formal management structure - Requires a board of directors and officers, reducing flexibility. |

| Attracts institutional investors - Venture capitalists and public investors prefer corporations. | More expensive to maintain - Higher administrative costs and legal fees. |

Corporations provide strong liability protection and long-term stability, making them a preferred choice for businesses planning to scale. However, they come with higher regulatory burdens and potential tax disadvantages. Choosing the right corporate structure depends on factors such as business goals, tax considerations, and ownership preferences.

Partnership vs Corporation: Key differences

Each business structure has distinct legal, financial, and operational implications. Let’s break down the key differences across multiple dimensions, helping you determine which entity best suits your needs.

Explore the key differences between partnership and a corporation

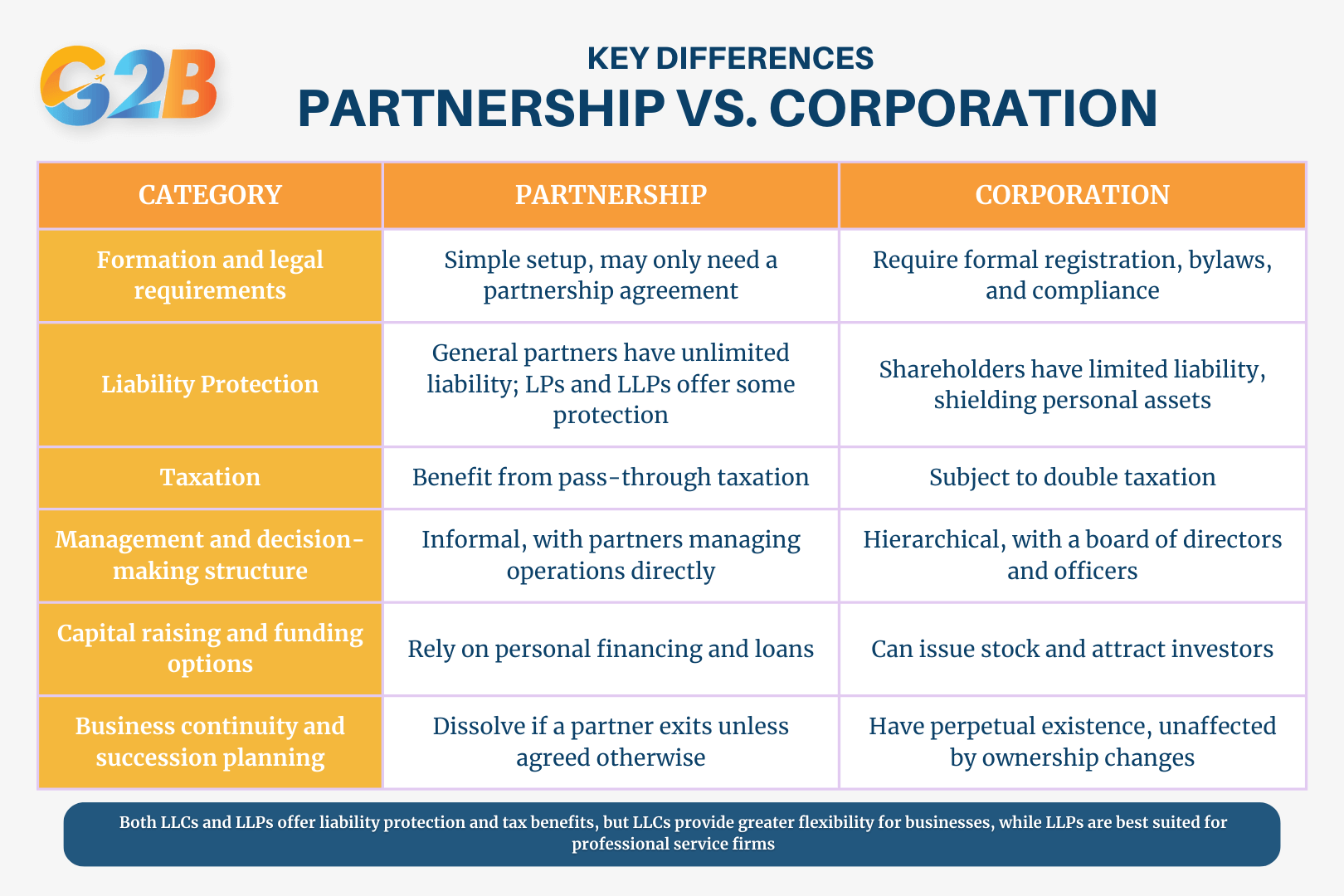

1. Formation and legal requirements

The process of establishing a partnership is generally simpler and less costly than forming a corporation.

- Partnerships: Typically require a partnership agreement, which outlines the roles, responsibilities, and profit-sharing arrangements among partners. General partnerships (GPs) may not even require formal registration in some jurisdictions.

- Corporations: Must file articles of incorporation with the state, adopt bylaws, and establish a board of directors. Compliance requirements are stricter, including annual meetings and detailed record-keeping.

2. Liability protection and risk exposure

Liability protection is one of the most significant differences between partnerships and corporations.

- Partnerships: In a general partnership (GP), partners have unlimited personal liability, meaning their personal assets can be used to cover business debts. Limited partnerships (LPs) and limited liability partnerships (LLPs) offer some liability protection for limited partners.

- Corporations: Shareholders enjoy limited liability, meaning their personal assets are generally protected from business debts and lawsuits. However, directors and officers can be personally liable in cases of fraud or negligence.

- Hybrid Structures: S corporations (S corps) and LLPs offer a blend of liability protection and tax benefits, making them attractive for some businesses.

3. Taxation: Pass-through vs double taxation

Tax treatment is another key factor distinguishing partnerships from corporations.

- Partnerships: Benefit from pass-through taxation, meaning profits and losses are reported on partners’ individual tax returns, avoiding corporate income tax.

- Corporations: C corporations (C corps) are subject to double taxation - the corporation pays corporate taxes, and shareholders pay personal taxes on dividends. S corporations, however, allow for pass-through taxation like partnerships.

- Tax Considerations: While partnerships avoid double taxation, corporations can take advantage of tax deductions, reinvestment opportunities, and lower corporate tax rates in some cases.

4. Management and decision-making structure

The level of formality in management varies significantly between these entities.

- Partnerships: Operate with a more informal structure, where partners typically make decisions collectively. General partners have authority over daily operations, while limited partners in an LP usually have a passive role.

- Corporations: Follow a formal governance structure, requiring a board of directors to oversee corporate affairs and officers (CEO, CFO, etc.) to manage operations. Decision-making is hierarchical and guided by corporate bylaws.

5. Capital raising and funding options

The ability to attract investment is a major advantage of corporations over partnerships.

- Partnerships: Rely primarily on personal financing, private investors, or bank loans. Since ownership is not easily transferable, raising significant capital can be challenging.

- Corporations: Have greater access to funding through equity financing, including issuing stock to investors. Venture capitalists and institutional investors prefer corporations due to their structured governance and limited liability protections.

6. Business continuity and succession planning

The longevity of a business depends heavily on its legal structure.

- Partnerships: Lack perpetual existence - they may dissolve when a partner exits, unless an agreement specifies otherwise.

- Corporations: Have continuous existence regardless of ownership changes. Shareholders can sell their shares, and the company can continue operating indefinitely.

- Transitioning from a partnership to a corporation is possible if a business outgrows the partnership model, offering increased flexibility and funding options.

7. Pros and cons summary

| Factor | Partnership | Corporation |

|---|---|---|

| Formation complexity | Low | High |

| Liability protection | Limited | Strong |

| Taxation | Pass-through | Double taxation (C Corp), Pass-through (S Corp) |

| Management flexibility | High | Structured |

| Capital raising | Limited | Strong |

| Business continuity | Limited | Perpetual |

Both partnerships and corporations offer unique advantages and challenges. Partnerships provide simplicity and tax benefits but come with personal liability and funding limitations. Corporations offer liability protection and growth potential but require more regulatory compliance and may face double taxation. Entrepreneurs should assess their business goals, financial needs, and risk tolerance before making a decision.

Key considerations for startup founders

Choosing the right business structure is one of the most critical decisions startup founders must make. This choice affects taxation, liability, scalability, and the ability to raise capital. While partnerships and corporations each offer unique advantages, the right structure depends on the startup's industry, long-term goals, and financial considerations.

Factors to consider when choosing a business structure

Before selecting between a partnership and a corporation, startup founders must assess key factors that impact business operations and growth potential.

- Liability protection: A corporation provides limited liability protection, meaning shareholders are not personally responsible for business debts. In contrast, general partnerships expose partners to unlimited personal liability, while limited partnerships (LPs) and limited liability partnerships (LLPs) offer partial protections.

- Tax implications: Partnerships use pass-through taxation, meaning profits and losses are reported on individual tax returns. Corporations, particularly C corporations, face double taxation, where both corporate profits and shareholder dividends are taxed. However, S corporations allow pass-through taxation while maintaining corporate liability protections.

- Ownership and control: In partnerships, management is typically direct and flexible, with partners actively involved in decision-making. Corporations require a formal governance structure, including a board of directors and officers, which may suit startups seeking structured decision-making and external investment.

- Administrative complexity and costs: Forming a corporation involves higher costs and regulatory requirements, including annual reports, corporate bylaws, and shareholder meetings. Partnerships, particularly general partnerships, have fewer compliance requirements but may lack the legal protections and credibility that corporations offer.

- Exit strategy and succession planning: Corporations have perpetual existence, meaning ownership can be transferred through share sales or inheritance. Partnerships, unless structured otherwise, dissolve upon the departure of a partner, making long-term business continuity more challenging.

Industry-specific considerations

Certain industries benefit more from one business structure over another due to liability concerns, regulatory requirements, or funding needs.

- Professional services (law firms, accounting firms, medical practices): Many professional firms opt for LLPs or professional corporations (PCs) to limit liability while maintaining operational flexibility.

- Tech startups and high-growth ventures: Corporations, particularly C corporations, are favored due to their ability to attract venture capital and issue stock options.

- Retail and service businesses: Partnerships or LLCs are often chosen for small-scale operations where personal liability is manageable, and formal corporate structures may not be necessary.

- Real estate and investment firms: Limited partnerships (LPs) are commonly used in real estate investments, as they allow general partners to manage the business while limited partners provide capital with reduced liability exposure.

Long-term business goals and scalability

The decision between a partnership and a corporation should align with the startup’s long-term vision, particularly regarding growth, funding, and operational complexity.

- Scalability: Corporations are structured for scalability, making them ideal for businesses planning to expand, enter new markets, or secure venture capital.

- Fundraising potential: Corporations can raise capital through stock issuance, attracting institutional investors. Partnerships rely on capital contributions from partners or debt financing, which may limit growth potential.

- Flexibility vs. stability: Partnerships offer flexibility in management and taxation, but corporations provide stability through a formal governance structure, making them more suitable for businesses with long-term growth aspirations.

For startup founders, choosing between a partnership and a corporation requires a comprehensive evaluation of liability exposure, tax obligations, growth plans, and industry-specific demands. Consulting legal and financial professionals ensures that the selected structure aligns with the startup’s long-term success and operational needs.

Data and statistics: Business entity trends

In the evolving landscape of global business structures, understanding the trends between partnerships and corporations is crucial for entrepreneurs, investors, and policymakers. This section delves into the data and statistics surrounding these entities, highlighting their prevalence, tax implications, and emerging patterns in the startup ecosystem.

Number of Partnerships vs. Corporations registered globally

As of 2023, the global business environment comprises approximately 359 million companies, marking a significant increase from 328 million in 2020. This growth reflects the dynamic nature of business formations worldwide.

In the United States, a notable shift has occurred over the past decades. By 2015, pass-through entities, which include partnerships and S corporations, filed approximately 33.4 million tax returns, accounting for 95% of all business returns. In contrast, traditional C corporations filed about 1.6 million returns in the same year. This data underscores a growing preference for flexible business structures that offer distinct tax advantages.

If you are looking for a partner to support businesses in matters related to taxes, legal issues, or company formation in Delaware, G2B is a unit that can meet these needs with a team of professional staff, accompanying customers.

Tax statistics on pass-through entities vs. Corporate taxation

The choice between operating as a pass-through entity or a traditional corporation significantly impacts tax obligations. Pass-through businesses, such as partnerships and S corporations, are not subject to corporate income tax. Instead, their income "passes through" to the individual owners and is taxed at their personal income tax rates, with a top marginal rate of 37%. However, certain pass-through income is eligible for a 20% deduction, effectively reducing the top rate to 29.6%.

In contrast, C corporations face double taxation. They pay corporate income tax at a rate of 21%, and shareholders are taxed again on dividends received, leading to a combined effective tax rate that can exceed 50%. This double taxation has prompted many businesses to consider pass-through structures to minimize tax liabilities.

Trends in startup business structures

Emerging trends indicate a shift in the preferred business structures among startups and small businesses. In the United Kingdom, for instance, there has been a decline in sole proprietorships and partnerships, with a 4% and 18% decrease, respectively, since 2019. Conversely, the number of registered companies has risen by 4% during the same period. This suggests that more entrepreneurs are opting for corporate structures, potentially due to benefits like limited liability and enhanced credibility.

In the United States, the trend towards pass-through entities continues. By 2017, there were 3.9 million partnerships filing tax returns, a 136% increase from 1996. These partnerships reported $2.2 trillion in net income, representing 38% of all business net income reported on U.S. tax returns that year. This growth reflects the attractiveness of pass-through taxation and the flexibility these structures offer to business owners.

In conclusion, the data reveal a dynamic shift in business entity preferences globally. The rise of pass-through entities and the sustained growth of corporations highlight the diverse considerations entrepreneurs must weigh, including tax implications, liability concerns, and structural flexibility. Staying informed about these trends is essential for making strategic decisions in today's complex business landscape.

Frequently asked questions

Understanding the key differences between a partnership and a corporation is essential for business owners choosing the right structure. Below are some frequently asked questions to clarify how these entities operate.

1. What are the main differences between a partnership and a corporation?

A partnership is a business structure where two or more individuals share ownership, management responsibilities, and profits. It is relatively easy to form and offers pass-through taxation. However, partners are usually personally liable for business debts unless it is a limited partnership (LP) or limited liability partnership (LLP).

A corporation, on the other hand, is a legally distinct entity that provides limited liability protection to its owners (shareholders). Corporations are subject to more regulations and must follow corporate governance structures, including a board of directors. Taxation varies depending on the type - C corporations face double taxation, while S corporations have pass-through taxation benefits.

2. Which structure provides better liability protection?

A corporation provides stronger liability protection than a general partnership. In a corporation, shareholders are not personally responsible for business debts, meaning their personal assets are protected. In contrast, general partners are personally liable for the business’s obligations unless they form an LLP or LP, which offers some liability protection. If liability protection is a primary concern, a corporation (or in some cases, an LLC) is the better option.

3. How do taxation rules differ for partnerships and corporations?

- Partnerships: Profits and losses pass through to individual partners, who report them on their personal tax returns. This avoids corporate taxation but may result in self-employment taxes for partners.

- Corporations: C corporations pay corporate income tax on profits, and shareholders are taxed again on dividends (double taxation). S corporations, however, allow income to pass through to shareholders like a partnership, avoiding double taxation.

The choice between these structures often depends on the tax strategy and long-term financial goals of the business.

4. Can a partnership convert into a corporation later?

Yes, a partnership can transition into a corporation through a legal process known as incorporation. This involves filing articles of incorporation, restructuring ownership into shares, and potentially drafting new operating agreements. Businesses often make this change to attract investors or limit personal liability.

5. Which is better for startups: partnership or corporation?

It depends on the startup’s goals:

- Partnerships are easier and cheaper to set up, making them suitable for small businesses with a limited number of owners.

- Corporations are better suited for startups planning to raise capital from investors, as they can issue stock and provide liability protection.

Many startups begin as partnerships or LLCs and later convert to corporations as they scale.

7. Can a partnership have limited liability like an LLC?

Not exactly. A Limited Liability Partnership (LLP) provides some liability protection but typically does not shield all partners from liability in the way that an LLC or corporation does. A Limited Partnership (LP) offers liability protection to limited partners, but general partners remain personally liable.

8. How do partnerships and corporations raise capital differently?

- Partnerships: Typically rely on personal investments from partners or loans. They cannot issue stock.

- Corporations: Can raise capital through stock issuance, venture capital, or public offerings, making them more attractive to investors.

If external funding is a priority, a corporation is the preferred structure.

9. What happens if a partner or shareholder leaves the business?

- Partnerships: Often dissolve or require a new agreement when a partner exits unless a buyout plan is in place.

- Corporations: Shares can be sold or transferred without dissolving the company, ensuring business continuity.

10. Which structure is easier to manage for a small business?

A partnership is easier to manage with minimal legal formalities. Corporations have more administrative burdens, including board meetings, compliance filings, and tax complexities. For small businesses seeking simplicity, a partnership (or LLC) may be the better choice.

Choosing between a partnership and a corporation is a critical decision that can shape your business’s legal standing, taxation, and growth potential. Both structures offer distinct advantages and challenges, making it essential to assess your long-term goals, risk tolerance, and financial needs before making a choice. If you want to know more about company formation, contact G2B today for expert consultation. We provide professional business support services, guiding entrepreneurs through every stage of business registration with confidence.