Delaware (USA)

Delaware (USA)  Vietnam

Vietnam  Singapore

Singapore  Hong Kong

Hong Kong  United Kingdom

United Kingdom With over 1.8 million tax-exempt organizations in the U.S. in 2024 and charitable donations surpassing $557.16 billion in 2023, the impact of 501(c)(3) organizations are undeniable. For entrepreneurs launching a nonprofit, considering tax-deductible donations, or ensuring compliance with IRS regulations, understanding how 501(c)(3) status works is crucial. This guide will go beyond surface-level definitions, offering a deep dive into 501(c)(3) organizations.

This article is provided for general informational purposes to help entrepreneurs understand the basics of 501(c)(3) organizations, particularly those focused on charitable, educational, or religious activities. We specialize in company formation, not in providing legal or tax advice for U.S. nonprofit compliance. For specific guidance on compliance, please consult a qualified nonprofit or legal expert.

What is a 501(c)(3) organization? Why is it important?

Nonprofit organizations play a crucial role in addressing societal needs, from education and healthcare to religious and scientific research. Among them, 501(c)(3) organizations hold a distinct status under U.S. tax law.

Definition and legal framework

501(c)(3) organizations are tax-exempt nonprofit entities recognized by the Internal Revenue Service (IRS) under Section 501(c)(3) of Title 26 of the U.S. Code. To qualify, an organization must:

- Be organized and operated exclusively for religious, charitable, scientific, literary, or educational purposes, among others.

- Prohibit earnings distribution to private shareholders or individuals.

- Avoid excessive political or lobbying activities.

- Maintain compliance with IRS reporting and governance standards.

The tax-exempt status applies at the federal level and often extends to state and local taxation, depending on jurisdictional laws. Organizations must file Form 1023 (or Form 1023-EZ for smaller entities) to obtain recognition from the IRS.

Key characteristics of a 501(c)(3) entity

501(c)(3) organizations share specific attributes that distinguish them from other types of nonprofits. These characteristics ensure transparency, accountability, and alignment with public service objectives:

- Public benefit focus: Activities must serve the general public rather than private interests.

- Tax deductibility of donations: Contributions from individuals and corporations are tax-deductible, incentivizing philanthropy.

- Annual reporting requirements: Most organizations must file Form 990 with the IRS, detailing financial information, governance, and operations.

- Restrictions on private benefit: No part of net earnings can benefit private individuals or stakeholders.

- Political activity limitations: Engagement in political campaigns is strictly prohibited under the Johnson Amendment, although limited lobbying is permitted within IRS-defined thresholds.

Why 501(c)(3) status matters for nonprofits

Obtaining 501(c)(3) status provides several strategic advantages:

- Tax exemption: Exemption from federal income tax allows nonprofits to allocate more resources toward their mission.

- Enhanced credibility: Recognition by the IRS signals legitimacy to donors, grantmakers, and partners.

- Increased funding opportunities: Eligibility for government and private grants, as well as corporate sponsorships, expands financial sustainability.

- Public trust and compliance benefits: Adhering to strict governance and reporting requirements fosters transparency and long-term viability.

According to the Tax Foundation, there are over 1.8 million tax-exempt organizations in the U.S., with 501(c)(3) entities making up the majority. In 2023, charitable contributions exceeded $557.16 billion, demonstrating the sector’s significant economic and social impact.

501(c)(3) organizations are foundational to nonprofit work in the U.S., shaping philanthropy, public service, and community development. Their legal framework ensures accountability, while their tax benefits and funding access empower them to fulfill their missions effectively. Understanding these entities is essential for nonprofit leaders, donors, and policymakers

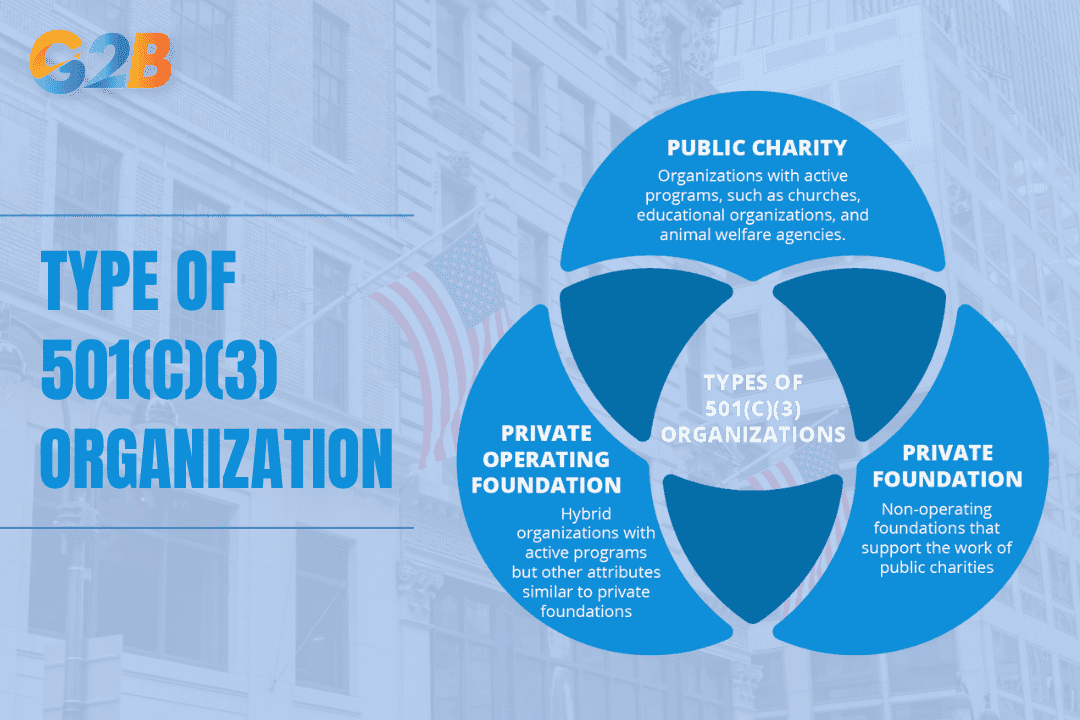

Types of 501(c)(3) organizations

501(c)(3) organizations in the United States are broadly classified into two main categories: public charities and private foundations. Additionally, there exists a subclass known as supporting organizations, which operate to assist other tax-exempt entities.

Public charities vs. Private foundations

The fundamental difference between public charities and private foundations lies in their funding sources and operational structures. The table below highlights key distinctions:

| Feature | Public charities | Private foundations |

|---|---|---|

| Funding source | Broad public support (donations from individuals, corporations, and government) | Primarily funded by a single individual, family, or corporation |

| Tax treatment | More favorable tax deductions for donors | More restrictions on tax deductions |

| Grantmaking | Directly engages in charitable activities | Primarily provides grants to other nonprofits |

| IRS scrutiny | Less stringent regulations | Subject to stricter IRS regulations and excise taxes |

| Annual filing | Must file Form 990 or 990-EZ | Must file Form 990-PF |

| Operational restrictions | Fewer restrictions on operations and investments | Prohibited from self-dealing, excess business holdings, and must distribute a minimum percentage of assets annually |

Public charities

Public charities make up the majority of 501(c)(3) organizations and typically engage directly in charitable activities. Examples include hospitals, schools, churches, and food banks. To qualify as a public charity, an organization must pass the public support test, which ensures that it receives a significant portion of its revenue from public contributions, government grants, or program-related income.

Benefits of public charity status:

- Higher donor tax deduction limits (e.g., individuals can deduct up to 60% of adjusted gross income for cash donations).

- Eligibility for government and private grants due to their public support status.

- Greater public trust and credibility, making fundraising easier.

Private foundations

Unlike public charities, private foundations rely on funding from a limited number of sources, often a single donor, family, or corporation. These organizations primarily distribute grants to public charities rather than directly conducting charitable programs. Notable examples include the Bill & Melinda Gates Foundation and the Ford Foundation.

Key regulatory requirements for private foundations:

- Mandatory annual distribution: Private foundations must distribute at least 5% of their net investment assets annually toward charitable purposes.

- Excise taxes on investment income: Foundations are subject to a 1.39% excise tax on net investment income.

- Self-dealing prohibitions: Transactions between the foundation and its substantial contributors or board members are heavily restricted.

Supporting organizations and their role

Supporting organizations are a hybrid category that provides financial or programmatic assistance to public charities. They operate under one of three classifications. These organizations are granted the same tax benefits as public charities but are subject to additional IRS scrutiny to prevent misuse:

- Type I – Operated, supervised, or controlled by one or more public charities.

- Type II – Operated in connection with one or more public charities.

- Type III – Functionally integrated with a public charity, but not controlled by it.

Examples of 501(c)(3) nonprofits

The following are well-known examples of 501(c)(3) organizations across different categories:

- Public charities:

- The American Red Cross (Disaster relief and humanitarian aid)

- St. Jude Children's Research Hospital (Medical research and patient care)

- Feeding America (Food security programs)

- Private foundations:

- The Gates Foundation (Global health and education grants)

- The Rockefeller Foundation (Scientific research and innovation funding)

- The Walton Family Foundation (Education and environmental grants)

- Supporting organizations:

- Jewish Federation organizations support multiple Jewish charities

- University-affiliated foundations providing scholarships and research grants

Understanding the types of 501(c)(3) organizations is essential for nonprofit leaders, donors, and policymakers. Each classification has distinct funding mechanisms, tax benefits, and regulatory obligations, impacting how an organization operates and sustains its mission.

There are 3 main types of 501(c)(3) organizations

How to obtain 501(c)(3) status?

Obtaining 501(c)(3) status is a crucial step for nonprofit organizations seeking federal tax exemption in the United States. However, the application process is highly regulated by the IRS, requiring strict adherence to legal and operational guidelines.

Eligibility requirements & IRS criteria

Before applying for 501(c)(3) status, an organization must meet specific eligibility criteria defined by the IRS. These include:

1. Organizational structure

- The entity must be structured as a corporation, trust, or unincorporated association (sole proprietorships do not qualify).

- A formal organizing document, such as Articles of Incorporation, must be filed with the state government.

- The organization must have a governing body, such as a board of directors or trustees.

2. Exempt purpose

- The organization must be organized and operated exclusively for exempt purposes, such as:

- Charitable

- Religious

- Educational

- Scientific

- Literary

- Public safety testing

- Amateur sports competition

- Prevention of cruelty to animals or children

3. Restriction on private benefit and political activity

If an organization meets these requirements, it can proceed with the formal application process:

- No part of the organization’s net earnings can benefit private individuals or shareholders.

- Political campaign activity is strictly prohibited.

- Limited lobbying efforts are allowed but cannot constitute a substantial part of the organization’s activities.

Step-by-step application process (Form 1023/1023-EZ)

The nonprofit application process involves incorporating at the state level, drafting bylaws, obtaining an EIN, and filing either Form 1023 or 1023-EZ based on the organization's size.

Step 1: Incorporate the nonprofit and draft bylaws

- Incorporate as a nonprofit corporation at the state level.

- Draft bylaws that define the organization's governance structure and operational guidelines.

- Obtain an Employer Identification Number (EIN) from the IRS.

Step 2: File form 1023 or 1023-EZ

Depending on the organization's size and complexity, it must file either:

- Form 1023 (for larger organizations or those with anticipated annual gross receipts exceeding $50,000)

- Form 1023-EZ (for smaller organizations with annual gross receipts under $50,000 and assets below $250,000)

Form 1023 requirements:

- Detailed narrative of activities

- Three years of projected financial statements

- Fundraising methods

- Compensation details for key personnel

- Conflict of interest policy

Form 1023-EZ requirements:

- Basic information about the organization’s purpose and structure

- Online eligibility worksheet to determine qualification

- Reduced documentation but still subject to IRS scrutiny

Step 3: Pay the IRS user fee

- Form 1023 filing fee: $600

- Form 1023-EZ filing fee: $275

Fees are subject to change, and organizations should verify the latest fee structure on the IRS website.

Step 4: IRS review and determination letter

- The IRS typically reviews 80% of Form 1023-EZ application determinations within 22 days (If your application requires more information or further review, 80% of applications needing further review within 120 days) and 80% of Form 1023 application determinations within 191 days.

- If approved, the organization receives a Determination Letter, officially recognizing its 501(c)(3) status.

- If denied, the IRS provides reasons for rejection and possible avenues for appeal or reapplication.

Common mistakes that lead to application denial

Despite meeting eligibility requirements, many organizations face delays or denials due to avoidable mistakes. Here are the most common errors:

1. Incomplete or inaccurate application

- Missing required documentation, such as financial projections or conflict of interest policies.

- Errors in organization name, EIN, or classification of activities.

2. Failure to prove charitable purpose

- The IRS requires a detailed explanation of how the organization’s activities align with 501(c)(3) exempt purposes.

- Vague or overly broad mission statements can lead to rejection.

3. Engaging in prohibited activities

- Attempting to qualify as a 501(c)(3) while engaging in political campaigning.

- Lacking transparency in financial management and governance policies.

4. Using incorrect form

- Organizations that do not qualify for Form 1023-EZ but attempt to file it will have their applications rejected.

- Some state-level nonprofit statuses do not automatically translate to federal 501(c)(3) eligibility.

5. Poor record-keeping and compliance planning

- Failure to create and maintain proper governance documents.

- Not having a strategy for annual reporting (Form 990) compliance.

Obtaining 501(c)(3) status is a rigorous but rewarding process that grants nonprofits significant tax advantages and access to public and private funding. Organizations must carefully follow IRS guidelines, avoid common application mistakes, and commit to ongoing compliance. A well-prepared application not only secures tax-exempt status but also lays the foundation for sustainable operations and community impact.

Tax benefits & financial advantages for 501(c)(3) organizations

Tax-exempt status under Section 501(c)(3) provides significant financial benefits for nonprofit organizations, enabling them to maximize their resources for charitable, educational, religious, or scientific purposes.

Federal & state tax exemptions explained

The most immediate benefit of 501(c)(3) status is exemption from federal income tax. Once an organization is recognized by the Internal Revenue Service (IRS) as a 501(c)(3), it is not required to pay federal corporate income taxes on revenue generated from its exempt activities. This allows nonprofits to allocate more resources toward their mission-driven programs rather than tax liabilities.

Key tax exemptions include:

- Federal income tax exemption: 501(c)(3) organizations are exempt from paying corporate federal income taxes on revenue generated from their tax-exempt purposes.

- State income tax exemptions: many states automatically grant tax exemptions to 501(c)(3) entities, while others require separate applications.

- Property tax exemptions: Nonprofits often qualify for state and local property tax exemptions, significantly reducing operational costs for facilities such as offices, shelters, and community centers.

- Sales tax exemptions: Some states provide sales tax exemptions on purchases made by 501(c)(3) organizations, reducing expenses on supplies, equipment, and other operational needs.

Consideration: Not all revenue is exempt from taxation. Unrelated Business Income Tax (UBIT) applies to income generated from activities unrelated to the organization’s primary mission. If a nonprofit earns revenue from a business venture outside its charitable scope, it may be subject to UBIT to maintain fair competition with for-profit enterprises.

How do donors benefit from tax-deductible contributions?

A significant financial advantage for 501(c)(3) organizations is the ability to offer tax-deductible donations to their contributors. This incentive encourages philanthropic giving by reducing a donor’s taxable income, making charitable contributions more attractive.

Key benefits for donors:

- Deductibility on federal taxes: Individuals and businesses can deduct donations to qualified 501(c)(3) organizations on their federal tax returns.

- Individuals: Can deduct up to 60% of their adjusted gross income (AGI) for cash donations.

- Corporations: Can deduct up to 10% of taxable income for charitable contributions.

- Stock & asset donations: Donors can contribute appreciated securities, real estate, or other assets without incurring capital gains tax, leading to higher net contributions for the nonprofit.

- Planned giving & estate tax benefits: Bequests and charitable trusts can help donors minimize estate taxes while leaving a lasting legacy to a 501(c)(3) organization.

- Matching gift programs: Many employers offer donation matching programs, effectively doubling the donor’s contribution while providing additional tax benefits.

Compliance note: Organizations must provide proper donor acknowledgment letters for contributions over $250 to ensure tax deductibility. Additionally, donors should retain receipts and documentation to support their claims during tax filings.

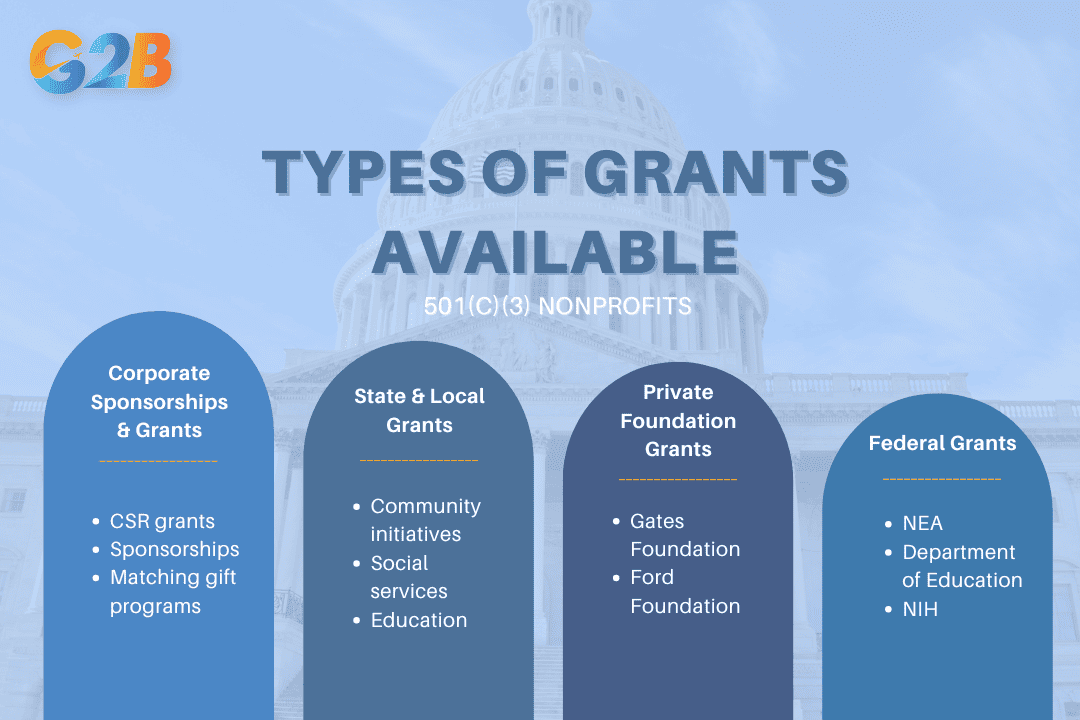

Grants & funding opportunities for 501(c)(3) nonprofits

Achieving 501(c)(3) status opens doors to a variety of grant and funding opportunities that are not available to for-profit entities. Many government agencies, foundations, and corporations exclusively fund tax-exempt organizations.

Types of grants available:

- Federal grants: Agencies like the National Endowment for the Arts (NEA), Department of Education, and National Institutes of Health (NIH) provide funding for nonprofit programs.

- State & local grants: Many state governments allocate funds for community initiatives, social services, and education programs run by nonprofits.

- Private foundation grants: Organizations such as the Bill & Melinda Gates Foundation and the Ford Foundation offer substantial funding for specific causes.

- Corporate sponsorships & grants: Many corporations offer corporate social responsibility (CSR) grants, sponsorships, and matching gift programs to support nonprofit initiatives.

Four types of grants are available in a 501(c)(3) nonprofit

Eligibility & compliance:

- Most grant applications require nonprofits to demonstrate financial transparency, program effectiveness, and alignment with the funder's mission.

- Regular Form 990 filings and annual reports help maintain eligibility for funding.

- Proper financial stewardship and impact reporting increase credibility and future funding opportunities.

501(c)(3) organizations benefit from a wide range of tax exemptions, donor incentives, and grant opportunities that contribute to their financial sustainability. By leveraging these advantages, nonprofits can optimize their funding, reduce operational costs, and enhance their ability to serve their communities. However, maintaining compliance with IRS regulations, financial transparency, and effective fundraising strategies is essential to maximizing these financial benefits and ensuring long-term success.

Compliance & IRS reporting obligations

Maintaining compliance as a 501(c)(3) organization is an ongoing responsibility that extends far beyond the initial tax-exempt approval. To retain their status, nonprofits must adhere to federal regulations, state requirements, and IRS reporting obligations.

Understanding form 990 & filing requirements

501(c)(3) organizations are required to file an annual return with the IRS through Form 990, a critical document that ensures transparency and accountability. The specific version of Form 990 an organization must file depends on annual gross receipts and total assets:

| Form type | Gross receipts | Total assets |

|---|---|---|

| Form 990-N (e-Postcard) | ≤ $50,000 | N/A |

| Form 990-EZ | < $200,000 | < $500,000 |

| Form 990 | ≥ $200,000 | ≥ $500,000 |

Key elements reported in Form 990 include:

- Financial statements: Revenue, expenses, and balance sheets

- Program service accomplishments: Description of mission-aligned activities

- Executive compensation: Salaries of top officers and key personnel

- Governance policies: Conflict of interest policies and board governance

Filing deadlines: Organizations must file Form 990 by the 15th day of the 5th month after their fiscal year ends. Extensions may be requested using Form 8868.

Record-keeping & transparency guidelines

Proper record-keeping is crucial for demonstrating compliance, responding to IRS audits, and maintaining public trust. The IRS requires 501(c)(3) organizations to retain records related to financial transactions, governance, and operational activities. Essential records include:

- Financial records: Bank statements, payroll records, receipts, and expense reports (minimum retention: 3-7 years)

- Governing documents: Articles of incorporation, bylaws, IRS determination letter (permanent retention)

- Meeting minutes: Board and committee meeting records (permanent retention)

- Donation records: Acknowledgment letters for contributions exceeding $250

Additionally, public disclosure requirements mandate that the following documents be accessible upon request:

- IRS Form 990 (for the last three years)

- Tax-exemption determination letter

- Application for tax-exempt status (Form 1023 or 1023-EZ)

Noncompliance with transparency standards may lead to public scrutiny and potential IRS audits.

Consequences of non-compliance & penalties

Failing to meet IRS compliance and reporting obligations can result in serious repercussions:

- Penalties for late or incomplete filings:

- Failure to file Form 990 may result in fines ranging from $20 to $100 per day, depending on the organization's size.

- If an organization fails to file Form 990 for three consecutive years, it will face automatic revocation of its tax-exempt status.

- Loss of tax-exempt status:

- Organizations that engage in prohibited activities, such as substantial lobbying or political campaigning, risk IRS revocation.

- If tax-exempt status is revoked, the organization may be required to pay corporate income tax on revenue and donations received.

- IRS audits & legal action:

- Nonprofits flagged for inconsistent reporting, excessive compensation, or improper use of funds may trigger an IRS examination.

- Serious violations, such as fraud or misuse of donations, can lead to civil penalties or criminal charges.

Staying compliant with IRS reporting obligations is not just a legal requirement but also a best practice for maintaining donor trust and organizational integrity. Regularly filing Form 990, maintaining accurate financial records, and ensuring transparency help 501(c)(3) organizations thrive while avoiding penalties or tax-exempt status revocation. Organizations should invest in compliance training, financial oversight, and professional consultation to navigate complex regulations effectively.

Restrictions & limitations for 501(c)(3) organizations

501(c)(3) organizations benefit from significant tax benefits, but these advantages come with strict limitations imposed by the IRS. Let’s explore the key restrictions that govern 501(c)(3) entities.

Political activity & The Johnson Amendment

One of the most well-known restrictions for 501(c)(3) organizations is the prohibition against political campaign intervention, codified in the Johnson Amendment (1954). This law strictly forbids any direct or indirect participation in political campaigns for or against candidates running for public office. Violating this rule can result in severe penalties, including the loss of tax-exempt status.

Key provisions:

- Endorsements & donations: Organizations cannot endorse, fund, or oppose any political candidate.

- Public statements: Official communications, including speeches, social media posts, and website content, must avoid political endorsements.

- Voter education & advocacy: Educational activities such as nonpartisan voter guides or forums are allowed if they do not favor specific candidates.

Consequences of violations:

- First-time violations may result in warnings or monetary fines.

- Repeated or severe violations can lead to revocation of tax-exempt status.

- Increased IRS scrutiny of financial transactions and public statements.

Lobbying rules & IRS guidelines

While 501(c)(3) organizations can engage in lobbying, their activities must be limited to an insubstantial portion of their overall operations. The IRS uses two tests to determine compliance:

1. The substantial part test

- Organizations cannot devote a substantial part of their time, funds, or resources to lobbying. ("Substantial" is not explicitly defined but typically means 5-20% of total expenditures)

- Factors such as staff time, meeting frequency, and financial records are considered.

2. The expenditure test (501(h) election)

- Organizations can opt into this test by filing Form 5768, which sets clear financial limits based on their total revenue:

| Annual revenue ($) | Lobbying limit ($) |

|---|---|

| Up to 500,000 | 20% of the exempt purpose expenditures |

| > $500,00 but ≤ $1,000,000 | $100,000 plus 15% of the excess of exempt purpose expenditures over $500,000 |

| > $1,000,000 but ≤ $1,500,000 | $175,000 plus 10% of the excess of exempt purpose expenditures over $1,000,000 |

| > $1,500,000 but ≤ $17,000,000 | $225,000 plus 5% of the exempt purpose expenditures over $1,500,000 |

| >$17,000,000 | $1,000,000 |

- Direct lobbying (contacting legislators) and grassroots lobbying (mobilizing the public) are counted towards the limit.

- Exceeding the limit in consecutive years may lead to penalties or revocation of tax-exempt status.

Unrelated business income & how it affects tax-exempt status

501(c)(3) organizations are expected to generate revenue primarily from charitable activities. However, if they earn income from unrelated business activities, they must comply with Unrelated Business Income Tax (UBIT) regulations.

Defining Unrelated Business Income (UBI): An activity is considered unrelated if it meets all three of the following criteria:

- It is a trade or business (involves sales, services, or commercial transactions).

- It is regularly carried on (consistent, frequent, or ongoing operations).

- It is not substantially related to the organization's exempt purpose.

Examples of UBI:

- Operating a bookstore or café that is not directly related to the nonprofit's mission.

- Selling advertising space on a website unrelated to educational programs.

- Running a parking lot that serves the general public rather than program participants.

Managing UBI to avoid IRS penalties:

- File Form 990-T to report unrelated business income.

- Limit UBI to prevent it from becoming a primary revenue source.

- Consider establishing a for-profit subsidiary to handle commercial activities separately.

Compliance with IRS restrictions is critical for 501(c)(3) organizations to maintain their tax-exempt status and credibility. While these entities have some flexibility in lobbying and revenue generation, they must navigate strict political activity bans, lobbying expenditure limits, and unrelated business income rules. By understanding these limitations, nonprofits can operate effectively while staying within legal boundaries.

Special considerations for religious 501(c)(3) organizations

Let’s investigate the key insights on special considerations for religious and church-based 501(c)(3) organizations, including unique IRS exemptions and compliance requirements, and how these organizations maintain their tax-exempt status.

1. Automatic tax-exempt status for churches

Unlike other nonprofit organizations, churches and religious organizations recognized under IRS guidelines receive automatic 501(c)(3) tax-exempt status without the need to file Form 1023. However, some churches still choose to apply for official recognition to provide clarity for donors and avoid potential legal challenges.

Key points:

- Churches are not required to apply for 501(c)(3) recognition but can do so voluntarily.

- Automatic tax exemption applies to churches, integrated auxiliaries, and conventions of churches.

- Filing Form 1023 can help establish legitimacy and allow donors to confidently claim tax deductions.

- Despite automatic exemption, churches must still comply with IRS rules regarding political activities and financial accountability.

2. Limitations on political and lobbying activities

Religious organizations with 501(c)(3) status must adhere to strict limitations on political activities. Engaging in partisan politics can jeopardize tax-exempt status.

Key points:

- Prohibited political activity: Churches cannot endorse or oppose political candidates, donate to campaigns, or distribute partisan materials.

- Permitted advocacy: Churches can speak on moral or social issues but must avoid direct political endorsements.

- Lobbying restrictions: Limited lobbying is allowed if it remains an "insubstantial" part of activities (typically less than 5% of total expenditures).

- Violations & consequences: Noncompliance can lead to revocation of tax-exempt status and IRS penalties.

Governance & best practices for 501(c)(3) organizations

Let’s find out essential governance principles and best practices to ensure your 501(c)(3) organization operates effectively and remains compliant.

1. Board governance & responsibilities

A well-structured board of directors is essential for the effective governance of a 501(c)(3) organization. Board members must understand their fiduciary duties, which include:

- Duty of care - Making informed decisions that best serve the organization.

- Duty of loyalty - Avoiding conflicts of interest and acting in the nonprofit’s best interest.

- Duty of obedience - Ensuring compliance with all legal and regulatory requirements.

Best practices:

- Maintain a diverse and engaged board with relevant expertise.

- Conduct regular board meetings with documented minutes.

- Establish clear policies on conflicts of interest and ethics.

2. Compliance with IRS regulations

501(c)(3) organizations must adhere to IRS rules to maintain their tax-exempt status. Key compliance areas include:

- Filing Form 990 annually to disclose financial information.

- Avoiding private inurement, where profits benefit private individuals.

- Ensuring activities align with the organization’s exempt purpose.

Best practices:

- Develop an internal compliance checklist.

- Engage legal or tax professionals to review filings.

- Maintain transparent financial records.

3. Financial management & transparency

Strong financial oversight ensures accountability and trust with donors and stakeholders. Organizations should:

- Implement internal controls to prevent fraud.

- Adopt generally accepted accounting principles (GAAP).

- Conduct regular financial audits or reviews.

Best practices:

- Develop an annual budget and monitor financial performance.

- Ensure donations and grants are properly allocated.

- Publish annual reports for donor transparency.

4. Fundraising ethics & donor relations

Fundraising must be conducted ethically, ensuring compliance with federal and state regulations. Organizations should:

- Follow honest and transparent solicitation practices.

- Provide proper documentation for tax-deductible contributions.

- Avoid excessive compensation or misleading claims in fundraising appeals.

Best practices:

- Adopt the Donor Bill of Rights.

- Implement a clear gift acceptance policy.

- Maintain strong donor stewardship to build long-term relationships.

5. Program effectiveness & impact measurement

Nonprofits should regularly assess their programs to ensure effectiveness and alignment with their mission.

- Establish measurable goals and key performance indicators (KPIs).

- Conduct periodic impact assessments.

- Use data and feedback to improve services.

Best practices:

- Engage stakeholders in program evaluation.

- Publish impact reports showcasing measurable outcomes

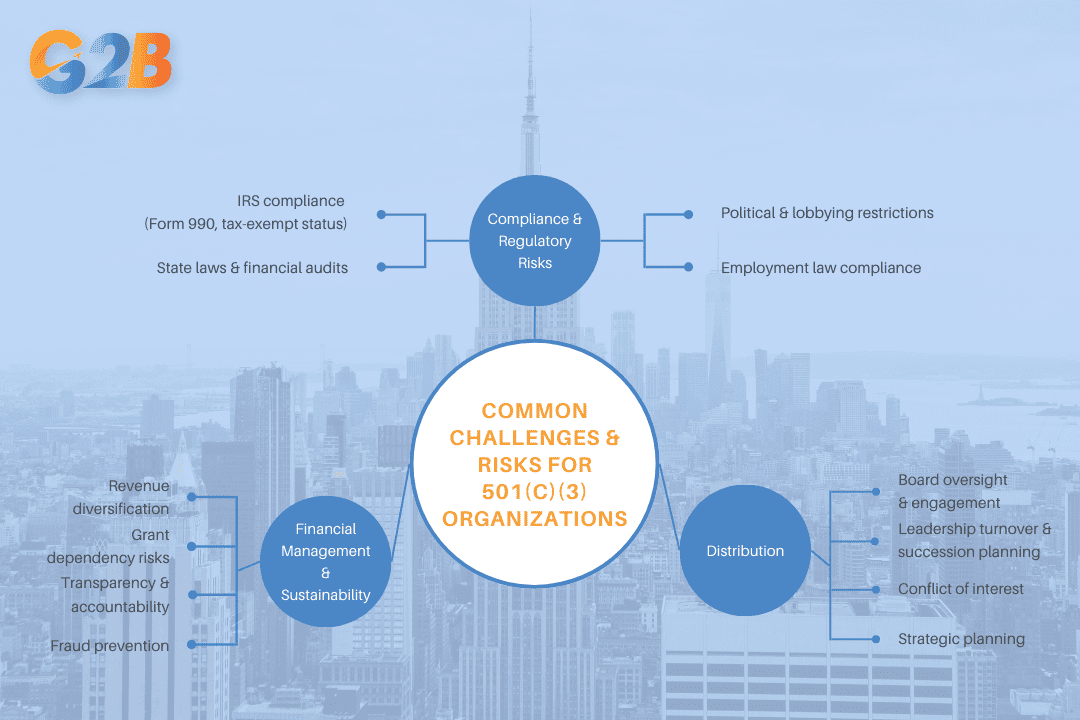

Common challenges & risks for 501(c)(3) organizations

Let’s uncover the common challenges and risks that 501(c)(3) organizations face, from regulatory compliance to financial sustainability, and learn proactive strategies to navigate these obstacles and protect your nonprofit’s mission and impact.

1. Compliance & regulatory risks

501(c)(3) organizations operate under strict federal and state regulations. Failing to comply with these requirements can lead to penalties, loss of tax-exempt status, or even legal action.

- IRS compliance: Organizations must file annual Form 990 to maintain their tax-exempt status. Failure to do so for three consecutive years results in automatic revocation.

- State laws & regulations: Many states require nonprofits to register and renew their status annually. Some also mandate financial audits for organizations exceeding a specific revenue threshold.

- Political & lobbying restrictions: 501(c)(3) organizations cannot engage in political campaigns and have strict limitations on lobbying activities. Violations can lead to penalties or loss of tax-exempt status.

- Employment laws: Compliance with labor laws, anti-discrimination policies, and worker classification regulations is crucial to avoid legal disputes.

2. Financial management & sustainability

Nonprofits often face financial challenges due to reliance on donations, grants, and fundraising efforts, which can be unpredictable.

- Revenue diversification: Relying on a single funding source can be risky. Organizations should develop diverse revenue streams, including membership fees, endowments, and corporate sponsorships.

- Grant dependency risks: Many nonprofits depend heavily on grants, which may not be renewed. Organizations should plan for financial sustainability beyond grant cycles.

- Transparency & accountability: Maintaining accurate financial records and demonstrating responsible fund usage is vital to retain donor trust and comply with financial regulations.

- Fraud & mismanagement: Weak financial controls can lead to fraud or mismanagement of funds. Implementing internal audits, segregation of duties, and oversight committees can mitigate these risks.

3. Governance & leadership challenges

Effective governance and leadership are critical for long-term success, but many nonprofits struggle with board engagement, leadership transitions, and strategic planning.

- Board oversight: A disengaged or underqualified board can negatively impact decision-making and oversight. Regular training and clear responsibilities help maintain a strong board.

- Leadership turnover: High executive turnover can disrupt operations and fundraising. Succession planning and leadership development are essential for continuity.

- Conflict of interest: Board members and executives must avoid conflicts of interest that could compromise the organization’s integrity.

- Strategic planning: Many nonprofits operate without a clear long-term strategy. Developing and regularly updating a strategic plan helps align the organization’s mission with actionable goals.

By addressing these challenges proactively, 501(c)(3) organizations can strengthen their compliance, financial health, and governance to ensure long-term impact and sustainability.

501(c)(3) organizations will grow stronger when addressing these challenges proactively

FAQs - Answering common questions about 501(c)(3) organizations

Nonprofit organizations operating under 501(c)(3) status must adhere to specific legal, financial, and operational guidelines. However, common misconceptions often arise. Let’s investigate three most frequently asked questions below.

Can a 501(c)(3) organization pay its employees?

Yes, 501(c)(3) organizations can pay their employees, but compensation must be reasonable and aligned with fair market standards to maintain compliance with IRS regulations.

Key Considerations:

- Reasonable compensation standard

- The IRS defines "reasonable compensation" as the amount that would ordinarily be paid for similar services by a comparable organization under similar circumstances.

- Excessive salaries can trigger Intermediate Sanctions (IRC 4958), resulting in penalties for both the organization and its leadership.

- Prohibited private benefit

- A 501(c)(3) organization cannot distribute its net earnings to individuals or private shareholders ("private inurement doctrine").

- Employees and executives can receive fair salaries but cannot profit from the nonprofit’s revenue beyond their justified compensation.

- Board member compensation

- While board members typically serve on a volunteer basis, some nonprofits compensate them for specialized expertise or time-intensive responsibilities.

- Any compensation must be disclosed in IRS Form 990 to ensure transparency.

Comparison: nonprofit vs. for-profit compensation

| Factor | 501(c)(3) Organizations | For-profit businesses |

|---|---|---|

| Salary cap | Must be "reasonable" | No legal restriction |

| Profit sharing | Prohibited | Allowed |

| Board compensation | Limited, often unpaid | Common and incentivized |

Bottom Line: 501(c)(3) organizations can compensate employees, but salaries must align with industry standards and IRS regulations to avoid penalties.

What happens if a 501(c)(3) loses its tax-exempt status?

Losing 501(c)(3) tax-exempt status has serious legal and financial consequences, affecting both the organization and its donors.

Reasons for losing tax-exempt status:

- Failure to file IRS Form 990

- Organizations must file Form 990, 990-EZ, or 990-N annually.

- Three consecutive years of non-filing automatically triggers revocation.

- Engaging in prohibited activities

- Political campaigning: Supporting or opposing political candidates violates the Johnson Amendment.

- Excessive lobbying: While some lobbying is allowed, exceeding the permitted threshold can lead to penalties or loss of status.

- Private benefit & misuse of funds

- Any misallocation of funds for personal gain or private shareholders is strictly prohibited.

Consequences of losing tax-exempt status:

| Impact area | Consequence |

|---|---|

| Tax liability | Organization must start paying corporate income tax. |

| Donor deductibility | Donations are no longer tax-deductible for contributors. |

| State-level effects | May lose sales tax exemptions or state nonprofit status. |

| Reinstatement process | Requires IRS reapplication via Form 1023 or 1023-EZ, with penalties and fees. |

Bottom line: Losing 501(c)(3) status leads to financial burdens and loss of donor incentives. Nonprofits must follow IRS compliance rules to avoid revocation.

Can a 501(c)(3) organization be converted to a for-profit business?

Yes, but the process involves strict legal procedures to ensure assets remain dedicated to charitable purposes.

Steps to convert a 501(c)(3) to a for-profit business:

- Dissolve the nonprofit entity

- A 501(c)(3) cannot simply "rebrand" as a for-profit; instead, it must legally dissolve according to state nonprofit laws.

- All remaining assets must be transferred to another 501(c)(3) nonprofit (per IRS "asset lock" rules).

- Establish a new for-profit entity

- File incorporation documents for the new for-profit business.

- Obtain a new Employer Identification Number (EIN).

- Register for taxable status with the IRS.

- Address legal & financial obligations

- Pay any outstanding tax liabilities.

- Notify stakeholders (donors, partners, employees) of the transition.

Alternative option: forming a hybrid model

- Instead of converting, some nonprofits form a "sister" for-profit entity, known as a social enterprise (e.g., L3C, Benefit Corporation).

- This allows the organization to pursue revenue-generating activities while maintaining a nonprofit mission.

Bottom line: A direct conversion is not allowed; a nonprofit must dissolve and reestablish as a for-profit business while ensuring assets remain dedicated to charitable purposes.

Understanding 501(c)(3) organizations’ structure, benefits, and compliance requirements is essential for nonprofit success. By applying these insights, you can ensure tax-exempt compliance, unlock funding opportunities, and build credibility within the nonprofit sector.

Need expert guidance on company formation in Delaware? Contact G2B today to receive comprehensive consulting based on your specific situation! G2B provides professional business support services, guiding you through every stage of business registration with reliability and dedication. Let us be your trusted partner on this expansion journey into new countries!